| Items | Amount |

| Original Loan | RM150,000 |

| Interest per annum | 3.25% |

| Loan tenure | 35 years |

| Remaining loan tenure | 30 years |

| Current loan balance | RM137,499 |

This article looks at the interest element for the latest moratorium announced by BNM. It disputes the message that banks will not charge any compound interest (interest on interest), as is being communicated to Malaysian consumers.

✉️ Subscribe to us on Telegram for the latest property insights and updates.

Bank Negara Malaysia (BNM) has stated that individual and microenterprise borrowers, as well as SMEs affected by the COVID-19 pandemic, may start applying for the six-month PEMULIH moratorium from 7 July 2021 onwards. Under this scheme, banks will waive the compound interest (interest on interest) and penalty charges incurred during the loan moratorium period.

According to Investopedia, Compounding is the process whereby interest is credited to an existing principal amount as well as to interest already paid. Compounding can thus be construed as interest on interest.

What you need to know about compound interest

What exactly is interest on interest? My layman’s understanding seemed to be different from the examples provided by the Malaysian banks. To illustrate my point, I simulated the monthly repayment based on examples provided by 2 commercial banks.

One bank extended the loan tenure with the loan moratorium scheme. The other one did not extend the loan tenure but instead increased the final month’s payment amount.

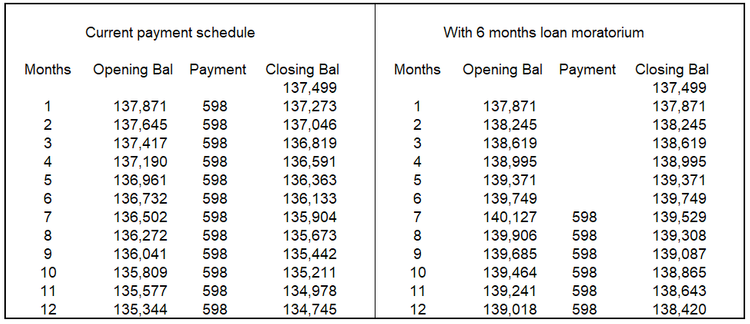

Chart 1 illustrates the difference in the simulated payment scheme for one of the banks. The column on the left shows the schedule based on the current loan term while the one on the right shows the schedule assuming the 6-months loan moratorium. You can see that there is no payment for the first 6 months.

For each column, the chart shows the amount due at the start of the month (Opening Balance). This is equal to the amount at the end of the previous month (Closing Balance) plus the interest charged for the month. For details refer to the Methodology section.

What does the chart illustrate? If you look at the Closing Balance for the example with a 6-month moratorium you will find the following:

- At the start of month 1, the borrower owned the bank RM 137,871. This was because there was one month interest of RM 372 based on the starting loan balance of RM 137,499.

- Then at the start of month 2, the monthly interest was computed to be RM 373 based on the Closing Balance for month 1 (RM 137,871).

- At the start of month 3, the monthly interest was computed to be RM 374 based on the Closing Balance for month 2 (RM 138,245).

As you can see, for the subsequent months the monthly interest was computed based on the previous month’s Closing Balance. But the previous month’s Closing balance included the accumulated interest.

This meant that the current month’s interest is based not only on the outstanding balance at the start of the moratorium but also includes the accumulated interest. If this is not interest on interest, I am not sure what is interest on interest or as it’s commonly known, compounded interest.

My layman’s understanding was that if there was no interest on interest, the bank would have used the same interest for month 1 for the 6 for the loan moratorium period. The simulated result for the other bank showed the same interest computation.

Doesn’t this show that the banks are charging interest on interest? I am of course not disputing the banks’ right to compute the interest as they see fit. But I would like to think that the description should suit the layman’s understanding. As it is there is interest on interest in a disguised form.

SEE WHAT OTHERS ARE READING:

💰 Moratorium Malaysia is ending soon: What to do if I cannot afford my loan repayments?

🤔 What are the disadvantages of the latest moratorium?

Loan moratorium calculation examples

When conducting my analyses, I looked at the financing schemes by two banks – Maybank and CIMB.

Maybank had the following loan profile.

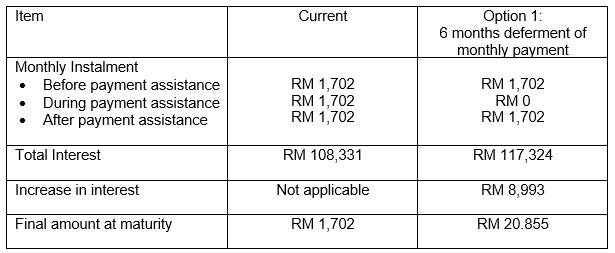

The bank illustrated the differences between the existing repayment schedule and one with a 6 months moratorium as follows. This assumed that there is no change to the interest rate during the loan tenure.

As you can see there is about RM 6,004 additional interest under the moratorium. This is equal to an additional RM 1,000 per month interest during the 6 month period.

Calculation if there is actually NO interest on interest

Shouldn’t the interest be RM 137,499 X 3.5 % X ½ year = RM 2,406 for the 6 month period if there was no interest on interest? This would be equal to just an additional RM 401 per month.

CIMB had the following loan profile.

| Items | Amount |

| Interest per annum | 3.25% |

| Loan maturity date | 1 July 2041 |

| Remaining principle | RM300,000 |

The bank illustrated the differences between the current and moratorium schemes as shown below. Note that in this case, the loan tenure remained the same. The difference was in the amount payable in the final month. The example assumed that the interest rate during the loan tenure remained the same.

</

</In this case, there was an additional RM 8,993 interest payable under the loan moratorium plan. This is equal to RM 1,499 per month.

Calculation if there is actually NO interest on interest

I would argue that if there was no interest on interest, the interest would be RM 300,000 X 3.5 % X 1/2 year = RM 5,250. This is equal to RM 875 per month.

Methodology used for interest calculation

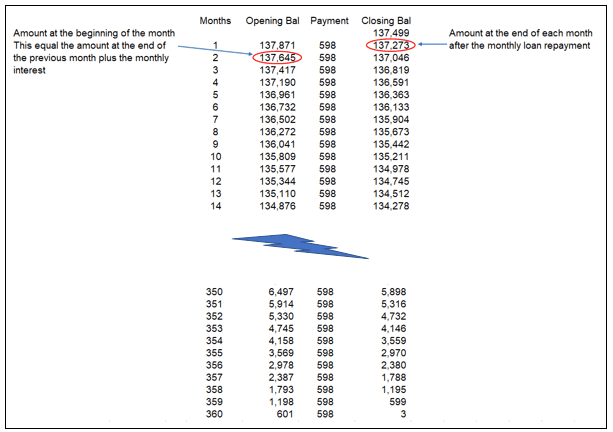

To ensure that I understood the banks’ computation, I created an Excel spreadsheet model as shown in Chart 2. This is a simple payment model with the following formulae.

- Opening Balance for month = Closing Balance of previous month plus monthly interest.

- Closing Balance for month = Opening Balance – Payment.

- The monthly interest is based on the Closing Balance of the previous month. The monthly interest = 3.25 %/12 months.

To obtain the exact figures as those for the Maybank example for the current payment schedule, the actual monthly repayment sum had to be RM 598.405. The results are close enough to validate the model.

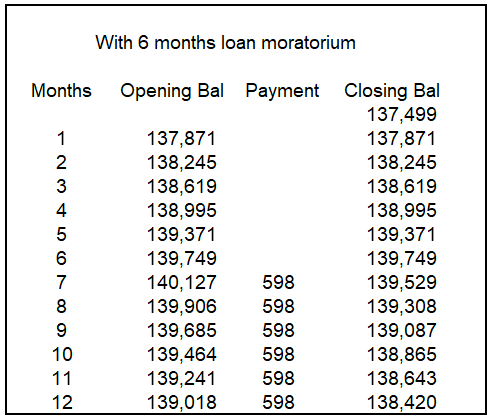

I next used the same model to compute the case where there is a 6-month moratorium on the loan as illustrated in Chart 3.

Basically, I just assumed that there was no loan repayment for 6 months. The rest of the formulae remained the same. Not surprisingly, if the monthly repayment was RM 598.461, I could match the bank’s total payment of RM 241,431, total interest of RM 83,931, and the extended tenure of 31.3 months. I would conclude that the model explains how the computation for the loan moratorium was done.

CHECK OUT: EIS PERKESO: How to claim job loss benefits & 4 other SOCSO claims

Conclusion

I carried out the simulation for both banks. Even though they have different payment schemes for the loan moratorium, the way the interest was computed for each month was the same. How was the monthly interest for the moratorium period computed? If you look at the Closing Balance in Chart 3 you will find the following:

- At the start of Month 1, the borrower owed the bank RM 137,871. This was because there was one month interest of RM 372 based on the starting loan balance of RM 137,499.

- Then at the start of Month 2, the monthly interest was computed as RM 373 based on Month 1’s Closing Balance of RM 137,871.

- At the start of Month 3, the monthly interest was computed to be RM 374 based on Month 2’s Closing Balance of RM 138,245.

As you can see, for the subsequent months the monthly interest was computed based on the previous month’s Closing Balance. You should not be surprised by this as I did not change the interest formula when I moved from Chart 2’s loan repayment scenario to Chart 3. I merely deleted the payments for the first 6 months.

This meant that the interest formula for the loan moratorium case was based on the same formula without the loan moratorium. In other words, it was based on compounded interest. As mentioned earlier, if this is not interest on interest, I am not sure what it actually is.

My layman’s understanding was that if there was no interest on interest, the bank would have used the same interest for month 1 for the 6 months period. So are the banks charging interest on interest?

Do keep in mind that I am not challenging the banks’ right to compute the interest as they see fit. Nor am I suggesting that this is the actual formulae used by the banks to work out the payment plan. But I think the analysis shows that there is some debate on what is actually meant when the government said that there is no compounding of interest. As iterated, this is my layman’s understanding of compound interest. If you have other views, please feel free to email me at [email protected].

This article was originally published as Pemulih loan moratorium – is there really no interest on interest? by i4value.asia and is written by Dato Eu Hong Chew.

TOP ARTICLES JUST FOR YOU:

Find out if home loan refinancing is for you?.

Find out if home loan refinancing is for you?.

Applying for a loan? Compare banks’ effective lending rates in Malaysia.

Applying for a loan? Compare banks’ effective lending rates in Malaysia.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.