| SECTOR | REMARK | ACTIVITY |

| Retail | Dropship, agent, stockist | Taking orders, packaging, receiving payments, delivery |

| Transportation & logistics | Delivery service, car rental, online ticketing | Services, payments, insurance, delivery |

| Financial services | Banks, payment gateways, cryptocurrencies, credit cards, debit cards, loyalty cards, membership cards | Confirmation of financial status, statement generation |

| Manufacturing & Agriculture | 3D printing | Taking orders, packaging, receiving payments, delivery |

| Education | E-books, online tuition, online tutorials | Taking orders, packaging, receiving payments, delivery |

| Health & wellness | Health and wellness products | Taking orders, packaging, receiving payments, delivery |

| Media & Broadcasting | YouTube, photography (as photographer and sale of images) | Content design, uploading, receiving payments |

| Sharing economy | Sharing of cars, houses, rooms, motorbikes | Services & payments |

| Subscription | Comic & newspaper online subscription, video streaming, audio streaming | Services & payments |

| Perkhidmatan | Software, facilitating, wedding planning | Services & payments |

| Advertising | Blogging, instafamous, insta reviews | Content design, uploading, receiving payments |

| Crowdsourcing | Example: kickstarter.com | Content design, uploading, receiving payments |

| Sale of digital products | Data, e-books, applications | Content design, uploading, receiving payments |

| Cryptocurrencies | Trading in cryptocurrencies | Trader, seller, miner |

Many people assume influencers and those who do not have steady incomes such as digital entrepreneurs and Youtubers are exempt from paying income taxes. This is not true. This article lays down how to calculate your income tax and the available exemptions if you count yourself among said worker category.

This article was translated from Adakah influencers dan peniaga ekonomi digital perlu bayar cukai pendapatan kepada LHDN? by Ridzwan A.Rahim.

It is that time of the year again – time to declare last year’s income and pay your income tax to the Inland Revenue Board (IRB). Whether your source of income is business, freelance work or permanent employment, you are required to declare your income.

According to the IRB, regardless of the nature of your work, as long as you make RM34,000 annually (about RM2,888.33 monthly) after Employee Provident Fund (EPF) deduction, you need to file your income tax.

What is the digital economy?

According to the LHDN website, the digital economy is an economy based on the use of digital technologies. Any business transaction conducted through the use of digital technology including information provision, promotion and advertising, marketing, and supplying of goods and services is considered digital technology. Even when the payment and delivery of the transaction are conducted offline, on the whole, it is still considered a digital economy.

If you are an influencer who gets paid to promote products on your social networks such as Instagram, Facebook and Tik Tok, you are required to declare your income and pay tax!

Examples of digital economy business activities

Source: IRB

Rules governing tax for the digital economy are similar to those governing incomes from conventional businesses under the Income Tax Act 1967.

If you or your company fall under any of the categories above, there are several obligations that you need to fulfil:

- Register with the IRB and get an income tax number

- Report revenues and losses from your business activities and digital economy activities

- Complete and submit Form e-B (tax form) through e-Filing

- Pay your tax (ByrHASiL)

How about tax exemption or tax relief?

Interestingly, some of your business expenses can be claimed for tax exemption.

| ALLOWED | NOT ALLOWED |

| Expenditure generating business revenue. Example:

| Domestic and personal expenditure. Example:

Purchase of personal assets. Example:

Purchase of personal assets.

|

SEE WHAT OTHERS ARE READING:

Housing loan checklist for freelancers: Non-standard documents you need to know

Housing loan checklist for freelancers: Non-standard documents you need to know

List of income tax relief for LHDN e-Filing 2022 (YA 2021)

List of income tax relief for LHDN e-Filing 2022 (YA 2021)

Other incentives that can be claimed by digital economy business operators

Aside from the exemptions and reliefs listed above, you may also enjoy deductions on capital allowance and the following incentives by the government:

1. Capital allowance

Digital economy business operators can also claim capital expenditure for the purchase of assets and a number of incentives that have been approved by the government. Deductions on capital expenditure incurred on business assets can be claimed after abatement of adjusted income. Special deduction on the cost of website development at 20% for five years. (PU (A) 101 Rules 2003).

Conditions for claiming capital allowance

- Business-related activities only

- Purchase of business assets only

- Assets used for business

| Type of allowance | Type of asset | Rate |

| Initial allowance | All types of asset | 20% |

| Annual allowance | Motor vehicles, heavy machinery | 20% |

| Plants and machines | 14% | |

| Office equipment, furniture and fittings | 10% | |

| Computers | 20% | |

| All types of asset | 20% |

2. Pioneer Status under the Promotion of Investment Act 1986.

Companies that have attained the MSC Malaysia Status Company from the Multimedia Development Corporation Sdn Bhd (MDEC) are eligible to apply for Pioneer Status under the Promotion of Investment Act 1986.

To do so, companies need to be involved in the following MSC Malaysia Status approved activities:

- Extension of research, development and provision of services related to research, development and commercialising of Web-based services or solutions related to search, directory and advertising

- Provision of professional support, technical, training and maintenance services related to Web-based solutions or services

3. Investment Tax Allowance (ITA) under the Promotion of Investment Act 1986

Companies that have acquired MSC Malaysia Status are eligible to apply for an Investment Tax Allowance (ITA) for their capital expenditure (CAPEX). If your company provides digital services to overseas clients from within Malaysia and you are not sure if you are liable to pay tax, CLICK HERE.

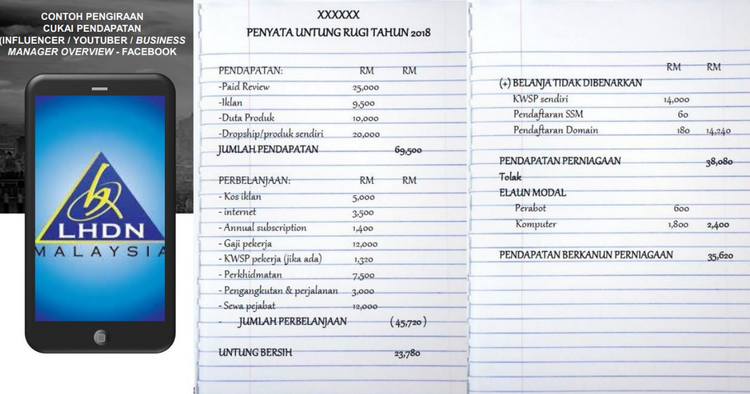

How to calculate income tax for influencers and digital businesses

For the purpose of calculating income tax, influencers first need to acquire their businesses’ total statutory income. Here’s a sample calculation as a guide:

1. Income

- Paid review = RM20,000

- Advertisement = RM9,000

- Brand ambassador = RM10,000

- Dropship/own product = RM15,000

TOTAL INCOME = RM54,000

2. Expenditure

- Advertising cost = RM6,000

- Internet = RM1,500

- Yearly subscription = RM1,200

- Employee wage = RM12,000

- Employee EPF (if applicable) = RM1,320

- Service = RM5,500

- Transportation and journey = RM4,000

- Office rental = RM8,500

TOTAL EXPENDITURE = RM40,020

*NET PROFIT = Total income + total expenditure = RM13,980

3. Expenses that are not allowed

- Own EPF = RM10,000

- Companies Commission of Malaysia (SSM) registration = RM60

- Domain registration = RM180

TOTAL = RM10,240

*BUSINESS INCOME = Net profit + expenses that are not allowed = RM24,220

4. Capital allowance

- Furniture = RM600

- Computer = RM1,800

TOTAL = RM2,400

*BUSINESS STATUTORY INCOME = Business income – capital allowance = RM21,820

A sample income tax computation by the IRB:

Documents required to claim business expenditure

If you want to make claims on your expenditure, the following is a list of documents and records that you need to keep for seven years as proof for the IRB:

- Statement from payment gateways such as Paypal, ipay88 and MOL

- Domestic and personal expenditure

- Bank statements

- Income statements from advertising firms such as Nuffnang and Google Adsense

- Sales invoice and purchase record

- Confirmation of sale and purchase through e-mail

- Agreement document

- Original receipts of each exemption and expenditure claimed

Regardless of whether you work in digital or not, you have a responsibility to pay taxes if required.

Failure to keep tax records

The following can happen if you fail to keep records of your tax:

- The risk of having your expenditure claims and tax exemptions denied

- You can be charged and fined no less than RM300 and no more than RM10,000 or jailed no less than 12 months, or both

- Under Section 82A, ACP 1967

Here’s hoping that all of us would be more aware of our responsibilities as taxpayers, even as suppliers of digital services, and not get a surprise visit from the IRB!

TOP ARTICLES JUST FOR YOU!

Income tax offences, fines, and penalties in Malaysia

Income tax offences, fines, and penalties in Malaysia

The pros and cons of refinancing your home

The pros and cons of refinancing your home

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.