Find out how you can reduce your taxable income and maximise the available tax rebates in 2020.

Taxpayers will have until the end of June 2020 to file their Income Tax Returns with the Inland Revenue Board of Malaysia (LHDN), either manually or by e-Filing. If you haven’t done so, then you are in luck as you can follow our top tips on how to boost your tax refund for 2020!

1. Claim for lifestyle-related purchases

During the 2017 Budget, the government introduced a tax relief category for lifestyle expenses worth up to RM2,500 per taxpayer. If you have not made the most out of the lifestyle income tax relief before, now is the time to do it, before it goes defunct.

The full list of the eligible purchases under the lifestyle income tax relief is as below:

- Books, magazines, and printed newspaper (except banned reading materials)

- Personal computer, smartphone, or tablet

- Sports equipment purchases (except motorised two-wheel bicycles)

- Monthly internet subscriptions bills

- Gym membership fees

Just remember that you can only claim up to RM2,500 and you need to also keep all of your receipts as proof.

2. Claim for your medical-check up

When was the last time you got your cholesterol and blood sugar levels checked? The government allows up to RM500 income tax relief for complete medical check-ups annually, so if you haven’t had one done this year, make use of that benefit and make an appointment with your doctor today.

If you are diagnosed with a serious disease, you can claim up to RM6,000 income tax relief for your medical expenses. Bear in mind that you are only allowed to claim for the listed serious diseases by LHDN, so check first before you make a claim for your medical expenses.

READ: Must you declare your rental income to LHDN & what are the tax incentives available for landlords?

3. Claim for your EPF and life insurance premiums

We know, we know. Life is tough enough without having to pay for adult “stuff” left and right, too. But if the generous Malaysian government is providing an income tax rebate for both Employee Provident Fund (EPF) deductions of and life insurance premiums of up to RM4,000 and RM3,000, respectively – be a smart Malaysian and make sure to claim it to the maximum!

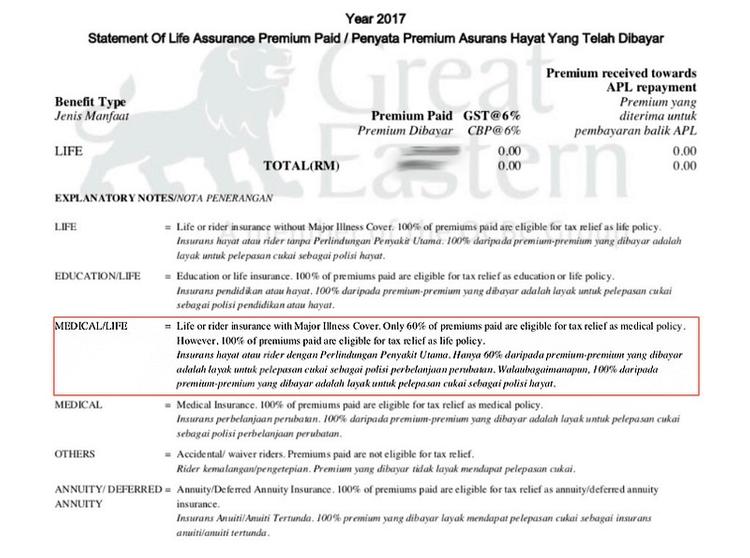

If you don’t have a medical or life insurance policy, it’s not too late to get one. Also, here’s a secret income tax tip that not everyone knows – if you have a life insurance policy with an attached Major/Critical Illness rider, you can claim 60% of the total annual premium paid under the medical insurance tax relief category (limited to RM3,000).

Here’s how this can work out to your advantage. For example, let’s say your:

EPF deductions or contributions = RM4,000

Life insurance annual premium = RM800

Medical insurance annual premium = RM2,600

So you have maxed out your income tax relief with your EPF deductions/contributions. But does that mean you can’t claim for the premiums you’ve paid for your life insurance policy? The answer is yes you actually can, but on one condition. You need to check if your life insurance policy has a Major/Critical Illness rider (make sure you do this, or you could be fined up to RM10,000 or imprisoned for negligence).

You can call your insurance provider directly if your agent is uncontactable, but you might be able to find this information on your annual statement. Here’s a sample on how it might look like:

Once you are sure that your life insurance policy qualifies for the 60% income tax relief, calculate it according to your annual statement. For example, from the above scenario, we can take 60% of the total life insurance premium (60% x RM800 = RM480) and include it with the medical insurance or education insurance tax relief claim (RM2,600 + RM480 = RM3,080).

Of course, you can only make a claim for RM3,000, but hey, at least you can now claim the maximum amount for both income tax relief categories!

CHECK OUT: BNM reduces OPR to 2% due to Covid-19 – How will it affect your home loan?

4. Claim for medical and education insurance

Sure, you have employee medical benefits, but what will you do if you get laid off or can no longer work due to whatever reason? How will you pay for your medical bills if you get sick or injured then?

If it’s the premium costs you are worried about, you can stop worrying now. Are you aware that you are entitled to up to RM3,000 income tax rebate for both medical and education (for your children) insurance premiums? Not only will you have your personal medical insurance coverage, but also get to reduce a lot of taxable income!

5. Claim for parental living and medical expenses

This relief is provided that you support your parents financially – you can claim income tax relief of up to RM3,000 (limited to RM1,500 for each parent) for living expenses or up to RM5,000 for their medical expenses. Start digging up all the medical bills and receipts that you have paid for and save on income tax today.

On a closing note, don’t wait until the very last minute, start drafting your YA 2019 income tax now. Check out our guide on how you can file Income Tax in Malaysia using LHDN e-filing.

*This article was repurposed from “THIS Is How to Claim as Much as Possible for Your Tax Refund!“, first published on Loanstreet.com.my.