| House Price (RM) | Loan (90%) | Tenure (Years) | Average Monthly Instalment (RM)

[Market Interest Rates: 4.3%-5.18%] | Minimum Average Household NET Income (RM)

[DSR = 70%] |

| 300,000 | 270,000 | 30 | 1,336 – 1,479 | 3,368 |

| 400,000 | 360,000 | 30 | 1,781 – 1,972 | 4,038 |

| 500,000 | 450,000 | 30 | 2,227 – 2,465 | 4,709 |

| 600,000 | 540,000 | 30 | 2,627 – 2,959 | 5,347 |

| 700,000 | 630,000 | 30 | 3,118 – 3,452 | 6,050 |

Don’t fear, we’ve got you covered – Check out our guide to determine which price ranges and residential neighbourhoods within Klang Valley best suit your salary.

Read the 2019 version of this article: How much should the average Malaysian household income be to afford a home in KV?

Buying a home is probably the largest financial milestone for most adult Malaysians. It seems like the most natural thing to do after one gets a stable paying job. Although there have been reports highlighting the slowing down of residential property price growth in the few recent years due to a poor economy and housing market glut, many millennials have a gloomy outlook on their chances of getting on the property ladder.

Even if you think you are financially ready to be a homeowner, do you know what kind of residential property and which price point you should be looking at? Determining your personal housing affordability isn’t always easy, as you will have to find the right balance between wants/needs and financial capability. Do you have the earning power to purchase a brand new condominium near the city centre? Or could you only afford a sub-sale apartment somewhere in Shah Alam?

Most importantly, how much cash do you need to buy a typical starter house within Klang Valley, which ranges between RM400,000 to RM600,00? Will your salary be able to finance the down payment and monthly repayments? Before you start surveying for your dream abode, let’s take a look at your finances and gauge how much you can realistically pay.

RELATED: First-time homebuyers: How to secure a home loan?

How much should you be earning?

When it comes to home purchasing, the general rule of thumb is that your Debt-to service (DSR) ratio should not exceed 70%. The DSR percentage shows how much of your income is being used to pay off debt and if you can afford to take up the housing loan you have in mind. This formula is used by banks to assess a borrower’s ability to repay his/her monthly instalments, where

DSR = Debt/Net Income X 100

Debt refers to all existing financial obligations, such as credit card repayments, personal loans and student loans whereas net income refers to your income after deductibles, such as income tax and EPF.

Most banks including Maybank and Public bank have a DSR cap of 65-70%, so it is crucial that you calculate your repayment ability for your target home before making the next move. The last thing you want to be doing is to utilise your entire salary for housing expenses.

For instance, let’s assume you earn RM5,000 each month. Hence, in order to fulfil the minimum 70% DSR rule, your total debt cannot exceed RM3,500.

DSR= RM3,500/RM5,000 X 100 = 70%

Let’s say you have the following financial obligations:

- Car loan: RM600

- Credit card repayments: RM250

- PTPTN Loan: RM100.

Current total debt amounts to RM950.

Therefore, when taking up a home loan, your monthly instalment figure must not be more than RM2,550. (RM3,500-RM950)

To help you figure out which property price range you should be targeting, we have created a table that details the estimated home loan repayments for a few price ranges that are considered affordable to most first-time Malaysian home buyers, i.e: RM300,000 to RM700,000, using the 70% DSR rule and the above current debt amount of RM950.

When calculating the minimum net income required for each price range, we ensured that the sum of current debt (RM950) and the average monthly instalment figure (mean of lowest and highest interest rate) does not exceed 70% of the net income stated in the last column:

* The calculations assume a 10% downpayment and a 30-year loan tenure whereas the interest figures are based on market rates of current loan products available in the market. These loan products range between 4.3% to 5.15% – calculations were tabulated using Ringgit Plus’s online calculator.

Do take note that there are other expenses to consider when purchasing a house – monthly instalments may take up the bulk of it, but you will also have to factor in stamp duty, legal fees, bank processing fees and insurance costs. It is imperative that you include all these complementary expenses into your budget before making a purchasing decision.

How to fund your down payment?

Looking for your dream home is tough, but forking out the initial 10% down payment is an even bigger headache, especially if you’ve just joined the workforce and don’t have significant savings. Nevertheless, there are plenty of alternatives out there which will support your homeownership dream. Here are some of the solutions that you can opt for :

1. A low-interest rate personal loan

This might not be an ideal option but it can be very helpful in times of financial need. Applicants who have a clean credit record will be able to negotiate with the banks for a lower interest rate. If you are applying for a loan from a bank in which you have an existing account, the approval process can be a whole lot faster. Make sure to shop around for the best product – look out for one which offers the most suitable tenure period, interest rates and monthly instalment amounts. This way, you will be able to finish paying your personal loan repayments before you even begin paying your mortgage loan in two or three years time.

2. EPF Account 2 Withdrawal

Another alternative would be to withdraw from your Employee Provident Funds (EPF) Account 2. This option is possible for aspiring home buyers:

- Who are buying a residential house

- Whose financing option has been approved by the bank

- Whose SPA has been signed but not more than three years

- Who has never made a withdrawal before for a house purchase

Where can you afford?

Now that you roughly know which price ranges you should be looking at, the next thing you would want to determine is which neighbourhood or area should you be scouting out your property for. Ask any urbanite for their dream residential location, and most will quote a city centre address – you are surrounded by plenty of conveniences including public transportation links, popular restaurants, malls and entertainment outlets. The only roadblock is, of course the hefty price tag.

Nevertheless, there are plenty of residential products throughout various suburbs located on the city fringes. The upgrades in roads networks and rail transportation infrastructure in the past year or two have also contributed to more homes being supplied in the market.

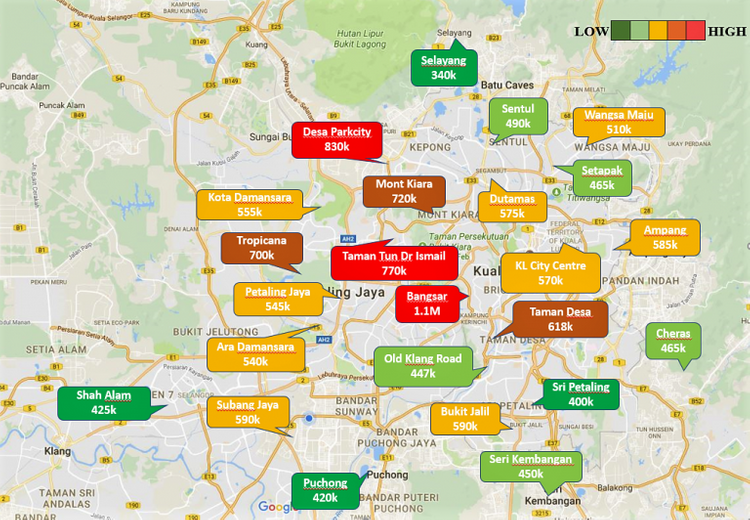

In order to provide readers with an affordability benchmark for various areas, we have compiled latest data from iPropertyiQ.com – the image below is a heat map of various residential boroughs within Klang Valley and their respective median prices per sq ft for condominiums.

The median figures displayed are recorded from April 2016 – March 2017 review period.

So you have calculated your DSR to determine the corresponding property price you should be able to afford – should the result be RM500,000 then, you should narrow down your home search to areas such as Puchong (RM420,000), Seri Kembangan (RM450,000), Shah Alam (RM425,000) and Cheras (RM465,000).

Here’s a bonus, there’s a great deal worth checking out in Cheras – Harta Intan Group recently launched Sapphire 9, a low-density condominium located within walking distance from the Taman Suntex MRT station (Line 1).

A major plus point – the Hulu Langat interchange which opens into the Cheras-Kajang Expressway is just a stone throw away from the development. FYI, there are only 150 units available, so make sure to check it out before its too late. More details here.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.