This article was updated on 16th July 2020.

Is your homeownership dream cut short by insufficient funds and steep home loan instalments? Despair no more as you are allowed to withdraw money from your EPF Account 2. Let us show you how!

Purchasing your first home requires a huge financial commitment and is no easy feat for most Malaysians, especially if you work in the city. An ‘affordable’ mid-range family home costs roughly RM500,000 and calls for a 10% downpayment of RM50,000! Even after this first hurdle is passed, you still have to worry about servicing your subsequent monthly loan repayments. Is it any wonder that most urban millennials are still living with their parents?

We have an interesting tidbit for those who are in a financial bind – it is possible for both current and aspiring homeowners to dip into their Employees Provident Fund (EPF) savings, in particular their EPF Account 2 to help finance their home purchase and instalments.

Here we lay out the step-by-step EPF withdrawal process for the purpose of:

A) Purchasing your first or second home

B) Settling your monthly instalments for an existing home loan OR paying down an existing home loan to save on interest costs

Register for i-Akaun on the EPF website

To get the ball rolling, you have to register for the i-Akaun facility on the EFP website. The fastest way to do this is through any nearby EPF Kiosk or counter. Alternatively, you may contact the EPF Contact Management Centre at 03-89226000. Once registered, you will need to activate your account by logging into your i-Akaun as shown below:

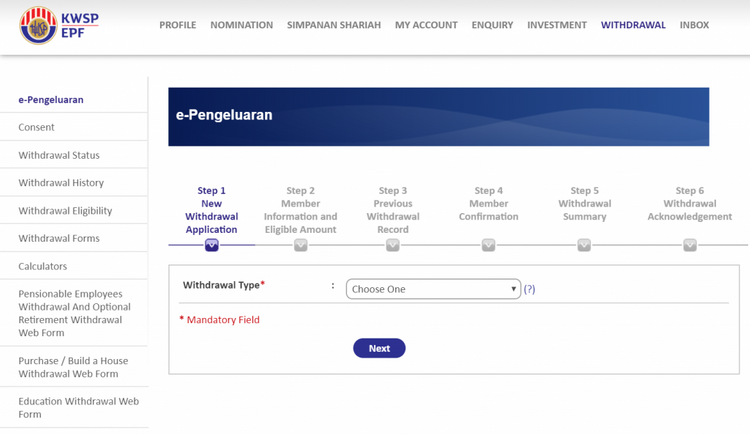

EPF has made it very convenient for home purchasers to apply for withdrawals online rather than doing it manually through the counter. Once you’re in, you will be taken to a page where you can select the different withdrawal types from the drop-down list below.

For first time applicants though, you will still need to present yourself at the counter. Subsequent applications can then be made via the site.

How to withdraw EPF Account 2 money to purchase (or build) a house

To utilise your EPF Account 2 money to pay the 10% down payment for a house, you will have to first fork out the 10% down payment yourself, payable to the developer for primary properties or to the property owner if purchasing a sub-sale house. Only then will you be able to secure a home loan from a bank/financial institution such as Maybank, CIMB or AmBank and sign the Sales & Purchase Agreement (SPA). As soon as your SPA is signed, apply immediately to EPF to redeem the down payment paid.

One can apply to withdraw the difference between the house price stated in the SPA and the housing loan amount (which is typically 90% as most first time home buyers have to submit a 10% down payment) on top of an additional 10% on the price of the house. For instance,

- SPA Price: RM500,000;

- Loan Amount (90%): RM450,000

Amount you can withdraw: (RM500,000 – RM450,000) + (10% of RM500,000) = RM100,000

Of course, withdrawals are limited to the savings amount in your Account 2.

REQUIRED DOCUMENTS:

- EPF Withdrawal Application Form 9C (AHL) (D5)

- Your Malaysian Identity Card (first time only). Thumbprint verification will be captured for subsequent applications.

- Bank loan documents (Letter of Loan approval or Loan Facility Agreement) certified by your borrowing bank. Inform the bank officer your intention to withdraw from your Account 2 and the rest will be done for you. You can either collect the documents yourself at the branch or have it mailed to you (usually within 2 weeks). Hence, make sure to collate your documents a few weeks before.

- Bank account information. Members are encouraged to bring their bank passbook OR a copy of their bank statement.

- Sales & Purchase Agreement (SPA)

CRITERIA

1) Age below 55 at the time of application.

2) Have at least RM500 in Account 2.

3) The property in question has to be for residential purpose only i.e bungalow/terrace/semi-detached/apartment/condominium/studio apartment/serviced apartment/townhouse/SOHO or a shop lot with a residential unit.

4) Can either be a Malaysian or non-Malaysian as long you are an active member and have been making EPF contributions.

5) Your home purchase can be either financed by a home loan granted by banks or via an outright cash purchase.

6) Withdrawal is only valid for one property (house) at any one time. Should you wish to apply for a second home, this is only possible once you have disposed of your first property. You must submit the proof of transfer of ownership.

7) The application must be made within 3 YEARS of signing the SPA. If it has been over 3 years since your house purchase, don’t worry. You still have the option to apply for a withdrawal on a monthly basis to reduce your housing loan (discussed below).

Did you know: EPF withdrawals made for home loan purposes are not subject to tax!

What if you are unable to come up with the 10% downpayment for the house purchase?

You would want to explore 100% financing schemes offered by a few banks. One such bank is MBSB, subject to certain conditions. However, applicants under this category can only withdraw up to 10% of the property price. So say your home costs RM500,000, you will be eligible to withdraw RM50,000 only. Alternatively, you will have to borrow or pool money from your parents, relatives or close friends in order to secure a 90% home loan. You can then pay them back with the monies withdrawn from your Account 2. It is wise to accumulate the sufficient amount of savings first before making your move; you wouldn’t want to be indebted to your loved ones for a long time.

How long does it take to withdraw EPF Account 2 for house loan?

EPF is very efficient in processing applications. The whole process of withdrawing from your EPF Account 2 to buy a house takes less than 3 weeks from the day of application to the point of the money being deposited into your account. Once your application is approved, you will receive an SMS requiring you to be present at any EPF counter for thumbprint verification. Speaking from personal experience, it only took 3-4 days for the money to be received!

READ: Applying for a home loan? Here’s what you need to know

How to withdraw EPF Account 2 money to help pay instalments or to reduce housing loan

Let’s say you were not aware that you are able to withdraw from your EPF Account 2 to pay down your house instalment, and you purchased a house over 3 years ago. You can still opt to withdraw money from your EPF Account 2 to assist with paying your monthly instalments or to pay down the capital of your home loan to save on interest costs.

CRITERIA

1) Same as above for Criteria 1-5

2) The house in question must be your first residential property/house.

3) You must be an owner of the property and have an outstanding home loan with a bank.

The next step will be to obtain the latest loan balance statement from your bank and submit it to EPF. Your bank will take about 2 weeks to process this.

You may apply to withdraw all your savings in your Account 2 but this will be paid to on a monthly basis, not exceeding the amount of your monthly instalment. For example, say your monthly repayment is RM1,000 and you have a total of RM10,000 in your Account 2. RM1,000 will be credited into your personal account or directly to your borrowing bank each month over 10 months.

NOTE: Those who apply for withdrawals before the 3-year mark of their home purchase, can request for the EPF money to be paid in a lump sum to help pay down their home loan balance.

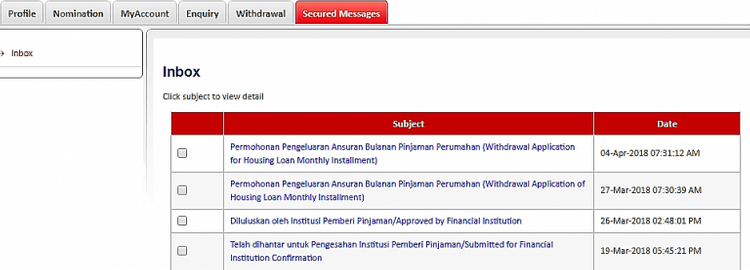

Again the whole process is pretty fast and takes less than 3 weeks to complete. An example of the timeline is as below.

An application was made on 19th March and it was submitted for the bank’s verification on home loan details. The bank in question approves said details within a week on 26th March. The following day (27th March), EPF proceeded to process the application and it was finalized on 4th April. You will be given a period of 2 weeks to present yourself at the EPF counter for thumbprint verification. Once that is done, the money will be disbursed to you within 3-4 days.

Do go through the detailed explanation available on the EPF website to gain a better understanding. Better yet, walk into any EPF office and speak directly to the officer on duty regarding your withdrawing options.

Also, make sure to find out what is your maximum home loan eligibility using the debt-to-service ratio (DSR) method. You can do this easily via the iProperty’s Home Loan Eligibility Tool also known as LoanCare in just three easy steps.

We wish you the best of luck!

_________________

Each month, the EPF amount contributed by your employer and yourself will be separated into Account 1 and 2, respectively according to the 70:30 ratio. Account 1 is the principal account and can only be fully withdrawn upon death, retirement or leaving the country for good, i.e giving up your Malaysian citizenship. Account 2 a.k.a the Withdrawal Account is the one which you can utilize for housing loan purposes and others including educational, investment and health purposes.

*Article was written in collaboration with Allen Phua. The personal experience sharing is courtesy of Allen Phua.