| Base rate of 3.0% | Assumed Inflation Rate | |||

|---|---|---|---|---|

| 4.0% | 4.5% | 5.0% | ||

| Value in 2000 (RM) | 800,000 | 800,000 | 800,000 | 800,000 |

| Value in 2019 after adjusting for inflation (RM) | 1,402,805 | 1,685,479 | 1,846,288 | 2,021,560 |

| Selling Price in 2019 (RM) | 2,400,000 | 2,400,000 | 2,400,000 | 2,400,000 |

| Actual gain after adjusting for Inflation (RM) | 997,195 | 714,521 | 553,712 | 378,440 |

| RPGT payable (RM) | 80,000 | 80,000 | 80,000 | 80,000 |

| Actual RPGT rate (%) | 8.0% | 11.2% | 14.4% | 21.1% |

The Real Property Gains Tax (RPGT) rates on disposal of real property assets have been increased for properties held for more than five years – is the rakyat being taxed unfairly? Let’s explore.

The National House Buyers Association (HBA) acknowledges the challenges faced by our Finance Minister, Lim Guan Eng, in tabling the maiden Budget 2019 from the Pakatan Harapan (PH) Government on Friday, 2nd November, 2018.

This is in view of the slowdown in global and regional economies and also the steep drop of the Ringgit, after taking over the Federal Government following the resounding victory in GE14. It is overall a commendable budget– save for the ill-advised issue that relates to Real Property Gains Tax (RPGT).

We speak for all when we say that it was a shocking moment when the announcement of the perpetual imposition of RPGT on disposal of property (with gains), was announced. It is best described by tax experts as a ‘knockout punch’.

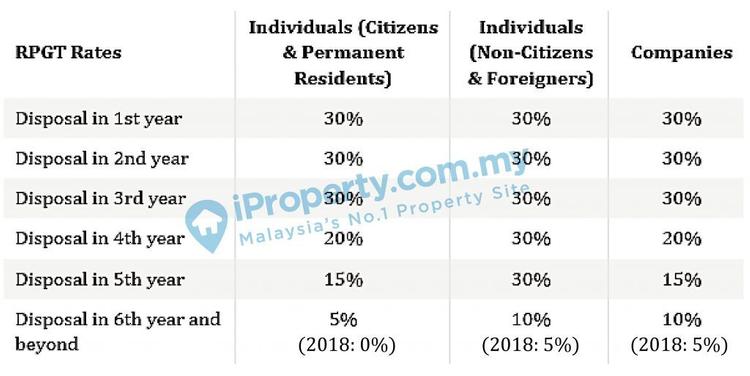

HBA is dismayed that genuine owners are now to be taxed for having ‘diligently preserved’ their properties beyond the grace period of 5 years. The new ruling simply means that the Government has proposed to impose a 5% RPGT for gains on disposal of properties held for more than 5 years by Malaysian citizens and permanent residents.

For non-citizens/permanent residents and companies, the RPGT rate will be increased from 5% to 10%. As for the calculation of property gain tax for units purchased before 2000, the Government will use the market price on 1st January, 2000 as the initial point of valuation.

READ: What is Real Property Gains Tax (RPGT) in Malaysia & How to calculate it?

This reflects badly on the PH Government as the previous RPGT regime was more equitable and fair where no RPGT was payable beyond the 5th year.

Properties are always seen as more than just a ‘roof over your head’, but also as a long term financial investment to hedge against inflation and to provide financial security in our golden years. By charging an RPGT rate for people who have held properties for 6 years or more, the PH Government is effectively imposing a ‘tax on inflation’ and this seems to punish genuine long term investors.

Who is affected?

This change affects many Malaysians from all walks of life. Never before in the history of Malaysia has the Government imposed RPGT for disposal made after 5 years of acquisition on Malaysian property owners.

In Budget 2010, the then Finance Minister proposed the imposition of such tax but this proposal was timeously reversed upon appeals from NGOs, the public and many genuine house buyers. Why does the PH Government deem it necessary to tax this group of long term individual property owners? Are there no other avenue for funds to be raised?

Do they not realise that property ownership is a means of savings?

Many individuals buy properties to provide a home for their family. Others view real properties as a better place to put their savings without the risk of fluctuations of the equity markets or unit trusts, and an option as opposed to just placing their money in a bank.

These groups normally have to borrow from financial institutions to finance their purchases and they hold on to their properties for the long term, some even for decades. They dispose of or buy property either to upgrade, downsize or as and when the need arises – to fund their children’s education, to meet medical expenses, to meet their retirement expenses or other reasons. Property ownership is a means of savings and a way to supplement their income by letting out the properties (for which taxes are paid).

MORE: Home Ownership Campaign (HOC) 2019 extended by another 6 months! Here’s what homebuyers should know

As the time gap between the purchase and sale is great, it would be expected that on paper, it would appear that a substantial gain has been made. However, now that property owners would have to pay a substantial amount of tax, this results in a reduction in the amount of funds available for the disposer’s use. Funds that could ultimately be used to provide a better and secure future for themselves and their family.

What is the justification for taxing genuine property owners and not those who make gains by placing their savings in other forms of investment? When it comes to gains from investments, we need to question the fact that other forms of gains are not being taxed, for example – Interest earned from savings in banks, equity markets, commodity markets, unit trust and other forms of trading, as well as investments in antiques, precious metals or stones.

Why are speculators and foreign property owners not affected?

Strangely, a third group of property owners are not affected at all by the current budget. This group comprises those who enter the property market with the sole intention of making a quick buck by buying and selling quickly. The speculators and flippers. The Government has deemed it necessary to let them ‘off the hook’ and not change the rate of tax imposed. Why is the RPGT rate imposed on short term property owners not revised upwards as well?

Not forgetting the foreigners who come in with their cache of funds to snap up properties, driving up prices until they are beyond the reach of the average rakyat and selling them off when the price goes up.

Recently, it has been reported that a Hong Kong actor has bought several properties in Malaysia and is just waiting to sell when the price increases. Why has the Government deemed it unnecessary to increase the rate of tax paid by the foreign property owner(s)?

The long term individual Malaysian property owners warrant an explanation from the Government for this unjust treatment. Are they being viewed as stool pigeons by the Government, knowing that there is no way for them to exit the property market immediately upon the announcement of the budget?

MORE: A beginner’s guide for strata property owners in Malaysia

Tax Exemption: Sale of Properties below RM200,000

The Government has announced that out of their concern for the rakyat, gains made from the sale of properties below RM200,000 is exempted from tax.

Honestly, how many of the rakyat will be able to enjoy this exemption? Even a small 700 sq ft leasehold walk-up flat is selling for more than RM250,000 in Kuala Lumpur. DBKL’s low cost 2-room flats measuring around 650 sq ft are now selling for above RM200,000 for non-bumiputra units and close to RM200,000 for bumiputra units and the prices are steadily creeping upwards for such flats.

As time goes by, will there even be any property in the towns selling for less than RM200,000? So this exemption is meaningless to the majority of property owners. Furthermore, the Government had not considered that by granting this allowance, there is a possibility that it may be encouraging the speculators to buy cheap properties to avoid having to pay RPGT, and thereby causing an artificial increase in the prices of such properties which were originally cheap and meant for the lower income group.

Let us consider the impact of inflation and RPGT under the following scenario:

Scenario 1: Albert inherited his late father’s property in Bangsar in 1989, some 30 years ago then valued at RM300,000. The property’s value in 2019 is RM2,400,000 and the value as of 1st January, 2000 (Government’s proposed initial point of valuation) is RM800,000. Assuming no other deductible cost, the gain on disposal is RM1,600,000 and the 5% RPGT payable on the RM1,600,000 gain is RM80,000.

Scenario 2: Ahmad purchased a double-storey link house in Kajang in 2004 for RM240,000 and wishes to dispose of this property to upgrade to a bigger house. The market value of the property in 2019 is RM520,000 and assuming that there is no other deductible costs, the gain on disposal is RM280,000 and the RPGT payable at 5% is RM14,000.

At first glance, it may appear that both properties have enjoyed a whopping increase in market value and the RPGT of only 5% seems reasonable. However, this is a deceptive and simplistic view as the market value increases during these periods also include normal capital appreciation and inflation.

Property has always been touted as the best hedge against inflation in the long run and the increase in property prices are also expected to be higher than just putting the money in the bank. Save for times of prolonged economic downturn, property prices are always expected to increase or else, all property investors and financiers will be sitting on equity losses.

Sensitivity of Inflation

As we do not have the published Official Malaysia inflation rate from 2000 to 2018, we will use a prudent base rate of 3.0% per year. However, as consumers, we all know that there is a difference between the so-called official inflation rate and the real rate of inflation due to declining purchasing power of the Malaysian Ringgit. Using the base rate of 3.0% up to 5.0% per annum, we have done a sensitivity analysis of the inflation rate based on Scenario 1 above.

Sensitivity of Inflation on Property price in Bangsar under Scenario 1

Just people will agree that the real rate of inflation is higher than just 3.0% per annum. If we were to consider that the real rate of inflation at say 4.5% per year, the same property that was valued at only RM800,000 in 2000, would have been valued at RM1,846,288 in 2019 and disposing of that property at RM2,400,000 will only produce a nett effective gain of RM553,712.

The RPGT of RM80,000 on the actual nett gain of RM553,712 represents a whopping 14.4% RPGT and not 5%.

Just based on an inflation rate of only 3.0% per year from 2000 until 2019, a property that was valued at RM800,000 in 2000 would be valued at a minimum of RM1,402,805 in 2019. If this property was subsequently sold at RM2,400,000, the actual gain, less inflation, is only RM997,195 and not RM1,600,000 and the RPGT of RM80,000 is actually effectively taxed at a rate of 8%.

Using the same example for Scenario 2 where the RPGT payable for the link house in Kajang was RM14,000 – a real rate of inflation at 4.5% per year will mean represents a whopping 25.2% tax on the RM55,532 actual gain (after adjusting for 4,5% inflation) and not 5%.

There was no tax payable then, but why made retrospective now? The Government may have reasoned this hike as an effort to help increase the country’s coffers and not to mitigate property speculation – however, it is a solution that’s opening itself up to other problems.

Read on the second part of this article where we will detail the 4 Reasons why the RPGT is punishing genuine homeowners & what could be done instead.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.