The inflation rate in Malaysia climbed to a one-year high of 3.4% in June 2022. Many may think that a house buyer should buy a property immediately as the effects of a high inflation environment have yet to be fully felt. We take a look at why you should not rush into buying a house.

Earlier this year, Bank Negara Malaysia projected that the country’s headline inflation will average between 2.2-3.2% in 2022. Also, there is anecdotal evidence that if we ignore price-controlled items, the inflation rate would be higher:

- The price of petrol RON 97 at the end of May 2022 was 19% higher compared to the end of April 2022.

- The ceiling price for standard chicken has risen 5.6% from RM8.90 per kg to RM9.40 per kg.

Malaysia may be entering a high inflation phase and the general view is that house prices will go up. However, it does not directly affect pricing. The authorities’ actions to limit inflation are however another issue we must deal with.

Interest rates have gone up, based on the recent OPR increase to 2.25%. Steps may be also taken to cool the economy that in the worst-case scenario leads to an economic contraction. Higher interest rates typically mean higher housing loans. An economic depression may affect household income, which in turn, may affect the buyer’s ability to secure a housing loan.

These are of course only general views. Based on historical evidence, there is no need for Malaysians to rush into buying a house during periods of high inflation. Read on to find out how I came to such a conclusion.

There is a correlation between house prices and inflation rates. In the Malaysian context, the Housing Price Index (HPI), which measures house prices, will rise more quickly over time than the Consumer Price Index (CPI). Many have thus projected that house prices will spike during periods of high inflation. On top of this, the authorities might try to control inflation further by increasing the OPR another time later this year.

READ: Malaysia’s house price: Will there be a market boom in 2022?

How is inflation measured in Malaysia?

Inflation is defined as the decline of purchasing power of a given currency over time. The general level of prices for products and services increases as a result. The most common method to quantify inflation is to use the Consumer Price Index (CPI), a price index that is based on a fixed basket of goods and services that represents the spending of an average consumer.

Aside from the CPI, there are other ways to measure the increase in the prices of goods and services. Examples of other inflation indicators are:

- Producer Price Index (PPI) – Tracks change in the prices paid to the producers of goods and services. PPI is also a measure of wholesale inflation, while the CPI measure the prices paid by consumers.

- Gross Domestic Product Price Deflator Index (GDP Deflator) – Measure changes in prices for all the goods and services produced in an economy. The GDP Deflator is a more comprehensive inflation measure compared to the CPI.

As they have a different basis of measurement, you should not expect the CPI, PPI or GDP Deflator to give the same results. For example, from the end of December 2021 to the end of March 2022 for Malaysia:

- CPI increased by 0.9%

- PPI increased by 5.8 %

- GDP Deflator increased by 3.6%

Because of the many price-controlled items in the CPI, you should not be surprised that the CPI has the lowest rates. In the context of this article, I will use the CPI as the reference point. If the CPI indicates high inflation, you can be sure that the PPI and GDP Deflator will have higher rates.

What is considered high inflation?

The US and most European countries have a target 2% inflation rate. However, news reports show that both US and UK are currently facing high inflation:

- The US reported an 8.3% annual inflation rate in April 2022.

- The UK Office for National Statistics reported an annual change in the CPI of 7.8% for April 2022.

It can be said that these countries are experiencing severe inflation as their actual inflation rate is four times the desired rate.

Whereas in the case of Malaysia, BNM does not have a target inflation rate although its goal is price stability. 8% will be considered a high inflation rate for Malaysia because the median annual inflation rate over the past 30 years was 2.3%, which is close to the western countries’ desired inflation rate.

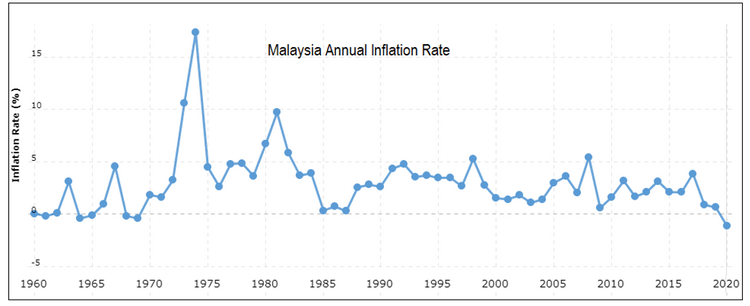

Chart 1 shows the annual inflation rates for Malaysia for the past 60 years. You can see that there were 2 years when the annual inflation rate exceeded 8%. They were:

- 3% in 1974 following the OPEC Oil Crisis.

- 7% in 1981 when the Malaysian economy was affected by the fall in commodity prices. This was the result of the oil price hike and the interest rate increases in the US.

When did Malaysia experience high inflation?

After 1981, there were no periods with more than 8% annual inflation rates – however, there were 2 peaks rates after 1981:

- 3% in 1998 following the Asian Economic Crisis.

- 4% in 2008 following the US Subprime Financial Crisis.

Does this imply that there haven’t been any instances of high inflation over the past 30 years? From a CPI standpoint, yes. However, this is because goods and services in Malaysia are subsidized and subject to price controls. We might have experienced high inflation in 1998 and 2008 if you accept that the PPI and the GDP Deflator would be higher than the CPI.

The fascinating aspect of Malaysia is that the high inflation periods only lasted a year and the subsequent years saw a significant drop in inflation. Since I am no economist, I won’t discuss the economic justifications for this. In my opinion, this would be a sign that Malaysia has a successful track record of quickly getting rising inflation under control.

How did the HPI change during periods of high inflation?

We know that in the Malaysian context, house prices as reflected by the Housing Price Index (HPI) tend to go up faster than the inflation rate. From an expenditure perspective, it meant that it is more cost-effective to buy a house today as compared to a few years ago.

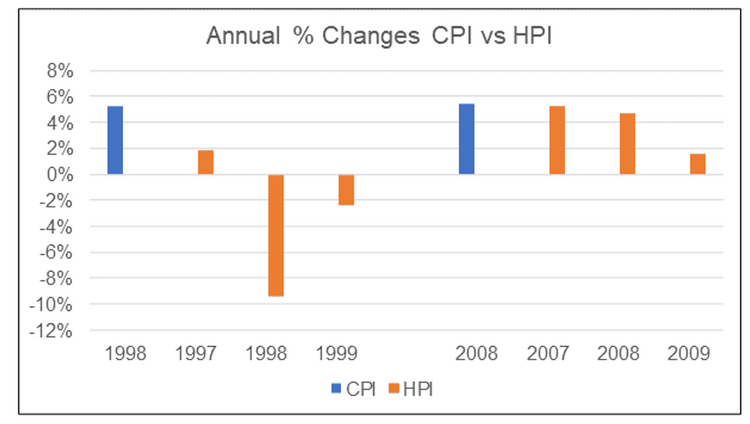

But these analyses looked at the changes in the HPI over the long term. In this article, we are looking at periods where the annual inflation rate is considered high. In the Malaysian context, over the past 30 years, there were 2 years where the inflation rate was greater than 5% – 1998 and 2008. How did the HPI change during such periods?

Chart 2 compared the annual inflation rate with the annual changes in the HPI. I looked at 3 periods – the year before, the reference high inflation year, and the year after.

- In 1998, the HPI decreased during the high inflation year and continued to decline the year after.

- In 2008, while there was no decline in the HPI. In fact, the HPI increased (at a slower rate than the CPI) in 2008 and the year after.

The conclusion from this limited dataset is that the % annual changes in the HPI are lower than the inflation rates (CPI). This applies to both the high inflation year (reference year) and the following year. As such, there is no urgency to buy a house during high inflation periods. House prices are not expected to increase at a higher rate than the high inflation rate.

This outcome should not come as a surprise to you. This is because input costs alone do not influence the price of a home. Property values are influenced by a few things, such as demographics, interest rates, the state of the economy, and government policies.

Impact of high inflation on lending rates

High inflation influences more than simply the cost of products and services. The central bank may raise bank lending rates as one method of controlling inflation during periods of high inflation that will then affect the housing loan rates. This will then lead to house buyers having higher borrowing costs, on top of paying more due to a higher house price.

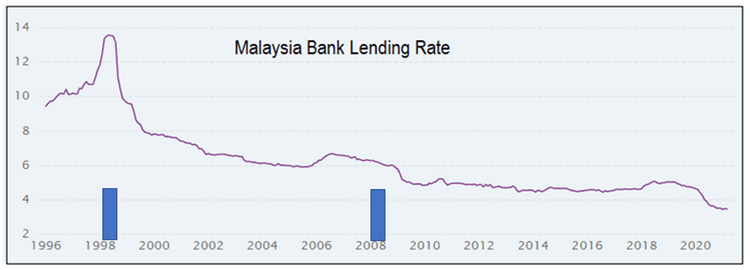

Note: The blue bar represents the inflation rate for the year. The purple line represents the average bank lending rate

Chart 3 compares the Malaysia Bank Lending Rate with the inflation rates for 1998 and 2008.

- You can see how bank lending rates significantly increased in 1998. But in 2008, we do not see such a rise.

- You can observe that there are decreases in bank lending rates the year following the year of high inflation for both 1998 and 2008.

The above is of course a simplistic analysis. The lending rates set by the bank are dependent on not only the central bank measures but also other economic factors. Looking at inflation rates alone is not enough.

In Malaysia, a 5% CPI rate does not always imply a higher bank lending rate. Even if there is a higher interest rate, it is short-term in comparison to the long housing loan term of more than 20 years.

Furthermore, the impact on the individual house buyers would depend on their mortgage plan. The impact of a fixed interest rate plan is different from a variable interest rate plan. This would also depend on whether the buyer is borrowing for the purchase of their first home or second property.

The conclusion is that there may be short-term pain during periods of high inflation from a long-term mortgage perspective.

TOP ARTICLES JUST FOR YOU

Standardised Base Rate (SBR): Differences with BR and how will it affect loans in 2022?

Standardised Base Rate (SBR): Differences with BR and how will it affect loans in 2022?

2022 Top condos for sale in KL

2022 Top condos for sale in KL

Debt Service Ratio (DSR): How to calculate and how does it affect home loan approval?

Debt Service Ratio (DSR): How to calculate and how does it affect home loan approval?

Impact of high inflation on household income

According to the Malaysia Rating Corp – In the 25 years between 1995 and 2019, Malaysia’s median household income expanded by about 6.2% per annum on a compound annual growth rate (CAGR) basis. This is slightly lower than the country’s nominal GDP growth of 7.7% per annum during the same period.

During the same period also, the CPI increased at a CAGR of 2.4 %. This means that over the past 25 years, household income increased at a faster rate compared to inflation. This augurs well for the Malaysian house buyer from the perspective of the house price as well as getting a mortgage. However, the short-term impact is not so clear-cut.

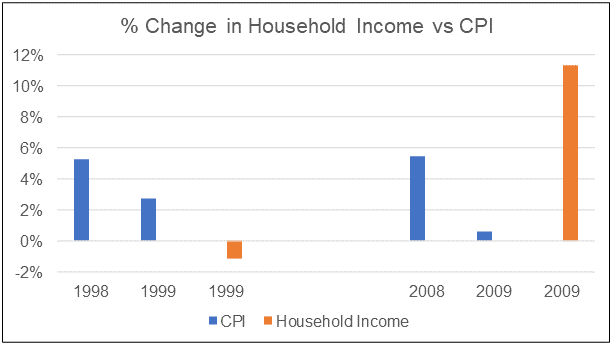

Note: The changes in the household income are for 2 years. Eg: 1999 compared to 1998.

Chart 4 compares the annual inflation rate for 1998 and 2008 with the percentage change in the median household income.

- In 1999, there was a contraction in the median household income compared to that in 1998. This was because the Malaysian GDP contracted by 7.4% in 1998, although it grew by 6.1 % in 1999.

- In 2009, the median household income increased compared to that in 2008. It grew at a higher rate than inflation. This was despite the GDP contracting by 1.5 % in 2009.

Given the household income contraction in 1999, house buyers would have problems securing a bank loan in 1999 compared to 2009. The analysis showed that when looking at the impact of high inflation on household income, you must look beyond price increases. Other economic factors are more important compared to inflation.

Conclusion

There is a correlation between house prices and inflation rates. It can’t be denied that over the long term, house prices in Malaysia as represented by the HPI will increase at a faster rate than the CPI. Many have thus predicted the same pattern in a high inflation environment.

On top of this, other impacts may result from the authorities’ efforts to control inflation. Thus, many foresee or predict the following in a high inflation situation:

- A higher increase in house prices. If the inflation rate is 5%, we would expect that house prices would increase by more than 5%.

- Housing loan costs would go up resulting in a higher monthly repayment sum than for a “normal inflation” period.

- Household income may not keep pace with high inflation. Alternatively, there may a decline in household income if there is slower economic growth or a recession.

The question we need to ask ourselves is, are the above a realistic scenario? Based on the evidence over the past 30 years, it can be concluded that:

- the HPI (housing prices) did not increase at a faster rate than the CPI (inflation rate) for both the high inflation year and the subsequent year.

- It is uncertain whether the bank lending rate would continue to increase

- Other economic factors (instead of inflation) may have a bigger impact on household income.

From an overall perspective, I would suggest that there is no need to rush to buy a house in anticipation of a high inflation period. This is because house prices are unlikely to shoot up, there is a risk of higher mortgage rates that may affect your ability to get home financing and there may be a short-term risk to your earnings.

More importantly, history shows that high inflation is only temporary. Given the borrowing and income challenges, it may be better to wait. After all, while house prices will continue to go up in the long run, so will income. Between 1995 and 2019,

Malaysia’s median household income expanded by about 6.2% CAGR while the HPI increased by 4.6% CAGR.

If you enjoyed this article, read this next: Rising bankruptcies: Are you financially ready to buy a property?

This article was originally published as Should you rush to buy a house anticipating high inflation? byi4value.asia and is written by Dato Eu Hong Chew.