| Housing Affordability Rating | Median Multiple |

| Affordable | 3.0 and below |

| Moderately unaffordable | 3.1 to 4.0 |

| Seriously unaffordable | 4.1 to 5.0 |

| Severely unaffordable | 5.1 to 8.9 |

| Impossibly unaffordable | 9.0 and above |

The median multiple “affordable standard” of 3.0 is derived from the historical trends in six nations – Australia, New Zealand, United Kingdom, Ireland, Canada, and the United States – which may not be a representative yardstick in other geographies.

Housing affordability refers to a household’s ability to pay for housing and housing-related costs without financial hardship. A simple measure of housing affordability is the ratio of house prices to income, which takes the basic form of the national average house price divided by the average annual income of buyers. The lower the ratio of house prices to income, the more affordable housing is.

The house price-to-income ratio is widely used to compare housing affordability across countries and over time within a country. Recognizing that averages can be affected by outliers and are likely to be skewed upward due to the inclusion of the highest prices and incomes, medians are used as better measures of central tendency to reflect the economic impacts on middle-income and lower-income households.

The median price-to-income ratio is also termed the “median multiple.” According to Demographia International, median-priced houses should be affordable to middle-income households in a well-functioning market, in which a housing market is considered affordable only if it can be financed by less than three times a household’s median annual income. On the other hand, a ratio of more than three indicates an unaffordable housing market and can be further categorized into moderately, seriously, severely, and impossibly unaffordable (Table 1).

Table 1: Demographia’s housing affordability ratings

Despite the median multiple is a useful broad measure for comparing housing affordability and is recommended by the World Bank and United Nations to evaluate urban housing markets, the accuracy of which the median multiple indicates an affordable housing market may vary between countries. This is because the median multiple “affordable standard” of 3.0 is derived from the historical trends in six nations – Australia, New Zealand, United Kingdom, Ireland, Canada, and the United States – which may not be a representative yardstick in other geographies.

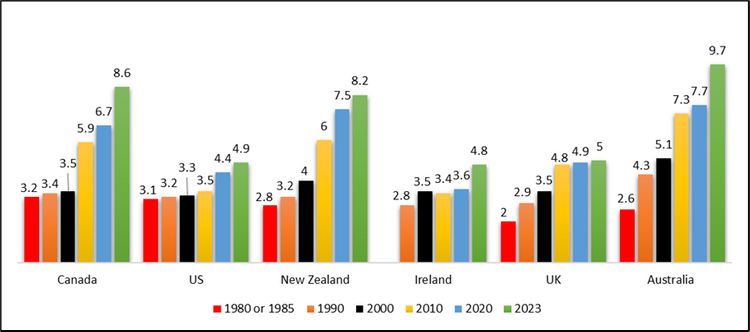

As shown in Figure 1, the median multiple in these six nations generally ranged between 2.0 and 3.0 until the 1980s or 1990s. However, a sharp increase in the ratio has been observed since the 2000s. In 2023, the Australian housing market was considered “impossibly unaffordable” with a ratio of 9.7, while housing markets in Canada and New Zealand are considered “severely unaffordable” with a ratio of 8.6 and 8.2, respectively. The remaining markets in the UK, the US, and Ireland were considered “seriously unaffordable,” with the respective ratios of 5.0, 4.9, and 4.8. As such, the ratio of 3.0 is set as a yardstick of “affordable” and was deemed predominated in most geographies.

Source: Demographia International; FRED; Trading Economics; GlobalData; KPI; DQYDJ; CCSD; statista

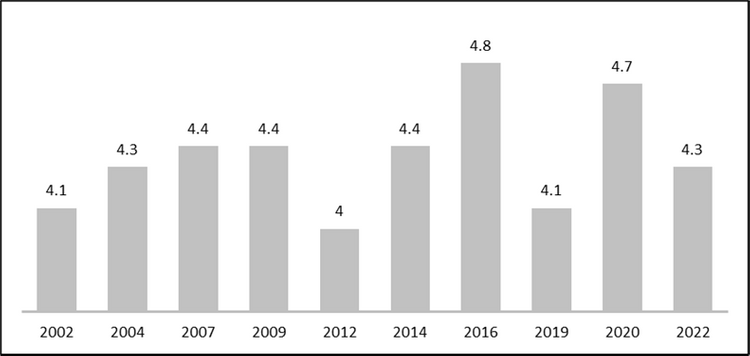

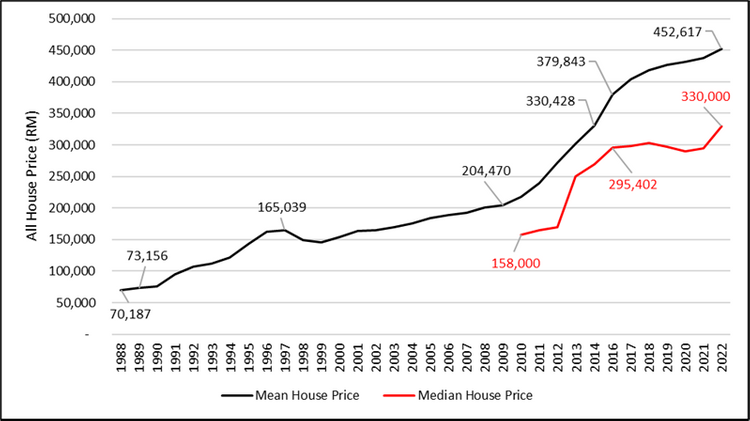

Unfortunately, this may not be the right yardstick for other nations due to different lifestyles, financial statuses, consumption patterns, etc., in different countries. Based on the median multiple approach, the median house price-to-income ratio in Malaysia was found to consistently exceed 4.0 since 2002, indicating that houses in Malaysia for the past 20 years were “seriously unaffordable.” Coupled with the fact that house prices in Malaysia started to rise sharply in 2009 (Figure 3), many believe that owning a house is much more difficult today than it was in the 1970s, 1980s, or even 1990s.

Besides, due to a lack of historical data, the median house prices recorded by NAPIC can only be traced back to 2010. Likewise, the median household incomes published by DOSM can only be traced back to 1995 (Figure 4). In this sense, many tend to perceive that the median multiple recorded before 2000 was probably 3.0 or below; hence, the “affordable” yardstick of 3.0 was also thought to be applicable to the Malaysian context.

Since then, housing policies that favour building affordable houses – as stipulated in the National Housing Policy (DRM) as well as the 5-year Malaysia Plan – were formulated and calls for the government to impose affordable/social housing quota in every housing development for the sake of the lower- and moderate-income group, are prevalent. This affordable/social housing is mainly capped at RM300k and below. For example, the Residensi MADANI – a newly introduced affordable/social housing program that aims to help low-income people own their comfortable and quality homes in the Federal Territory – is capped with a selling price range from RM150k to RM200k per unit.

Looking for New Homes? Click Here to Browse The Latest Launches in Malaysia!The mandatory in building affordable/social housing may be defended on the grounds of social justice, but its impact on the free-market houses is inequitable. This is because building affordable houses that are capped below the market price not only gives rise to the question of whether it is possible to build adequate houses that are cheap enough to meet the needs of the low-income group but also contributes towards an unsustainable price distortion in the market, as the development of affordable housing is only viable through cross-subsidization from free-market housing products targeted for other income groups.

The fact that cost subsidy is required in building affordable/social housing is evident in a statement made by the Ministry of Housing and Local Government (KPKT) when introducing the Program Residensi Rakyat (PRR), in which each of these PRR units has a construction cost of RM300k with the government subsidy of RM240k so that each of these units can be sold at RM60k, making them accessible to the low-income group.

Back to the measure of the price-to-income ratio in the 1980s and 1990s, although the required data for median house prices and household incomes in the 1980s and 1990s is incomplete, the average house prices and household incomes are recorded, which can be used as a proxy to assess the country’s housing affordability in 1980s and 1990s.

As shown in Figure 5, the mean housing affordability recorded in 1989 was 5.2, which was derived from the mean house price of RM73,156 (Figure 3) and the mean monthly household income of RM1,169 (Figure 4). After hitting its historical high at 5.9 in 1995, the ratio went down and hovered around 4.1 to 5.0 (seriously unaffordable) for more than two decades. Based on the median multiple 3.0 yardsticks, the housing market in Malaysia was generally considered “severely unaffordable” throughout the period of the 1990s.

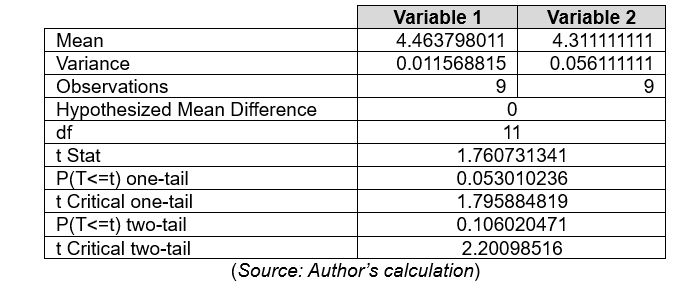

By running Welch’s t-test to determine if there is a significant difference between the mean and median housing affordability from 2002 to 2022 (Table 2), results show that mean housing affordability should not differ too much from median housing affordability. This, in turn, suggests that using averages to measure housing affordability is reliable in the absence of median data.

Table 2: Results of t-test where two samples assuming unequal variances

While house prices were lower in the past than they are now, household incomes were even lower in the past compared to the present, which further worsen people’s housing affordability. As far as one can observe, between 1989 and 2022, the country’s house price-to-income ratio never fell below 3.0. This not only raises the question of the appropriateness of using the median multiple of 3.0 as a yardstick to assess housing affordability in the Malaysian context, but also challenges the commonly accepted view that housing now is less affordable than in the past.

Housing unaffordability is likely to persist if we continue to benchmark our housing affordability with the median multiple of 3.0 and then call for more affordable houses within certain price range to be built. Doing so will not only give rise to the question on whether it is even possible to build housing cheap enough to make it affordable to the lower-income group, but may also contribute to the problem of cross-subsidization, thereby posing threats to the balance of the housing industry ecosystem, and even with the tendency of exacerbating the problem of oversupply in the affordable housing market segment.

To better gauge the country’s housing affordability so as to facilitate the development of a sustainable housing policy, measures of housing affordability that solely compare house prices to household income should be avoided. Instead, a method that is more reflective of a household’s ability to purchase a house by considering the household’s spending pattern, attributes, cost of living, and even housing construction costs should be adopted. In terms of the scale of measurement, a city level is highly recommended as the housing market is localized and segmented in nature.

One should also realize that there is always a “cost” to build affordable/social housing selling below market price. House prices will not return to more affordable levels until land becomes available at more reasonable prices, especially in highly urbanized areas where land values naturally increase closer to urban centres.

Given that unsustainable supply of affordable/social housing in urban areas is due mainly to the high land cost, which can only be made possible through cross-subsidization of free-market housing, the government should consider unlocking “pocket lands” or land reserves owned by government agencies or its corporatised bodies that have been left idle for future affordable/social housing development.

For example, the government’s recent decision to review the Bandar Malaysia development plan is a timely and wise move to ensure that future development in this largest remaining government-owned land in the heart of Kuala Lumpur adhere to the development principles that balance the ecosystem while providing affordable housing for the people.

By doing so, an effective public-private collaboration in providing affordable/social housing can be established, where private developers only need to bear the construction and compliance costs of affordable/social housing development. This will free them from paying substantial land costs and enable them to provide housing units below market price in a stand-alone project without even cross-subsidizing the profits made in free-market housing units.

Just like the recent announcement on joint development between SkyWorld Development Bhd and Penang Development Corporation (PDC) in building 35,000 affordable housing units – with a selling price ranging from RM225k to RM420k – in Penang. With an estimated gross development value (GDV) of RM13 billion and a total land cost of RM502.4 million for two lands totalling 195.54 acres, the respective land cost to GDV is as low as 3.9%, which has contributed significantly to improving the “buildability” of the project.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.