Here are 4 reasons why the RSKU homeownership rate is so low despite the affordable selling price.

What is Rumah Selangorku?

Rumah Selangorku (RSKU) is a housing scheme introduced by the Selangor state government in 2014, and led by the state’s own housing organisation – Lembaga Perumahan dan Hartanah Selangor (LPHS), with the aim of delivering affordable houses to qualified citizens within the state. Under this initiative, developers of qualifying developments are mandated to construct a certain amount of affordable housing units as part of their overall project, with a specified house type, size, and capped selling price, based on the location and size of development.

With the help from the private sector, the state government believes that this scheme can not only synchronise the housing supply and demand mismatch in the market, but also help resolve the home-ownership and affordability issues in Selangor.

To further ensure the private sector is on board with these measures, the state government has decided to withhold the necessary approvals for developers who do not meet its RSKU quotas or have delayed the construction of RSKU in their project.

This means that RSKU houses must be built in the first phase of the project’s development or concurrently with other residential units. Failure to comply could result in punitive action by the respective local government, including the suspension of the development order, building plan approval, as well as the issuance of the certificate of fitness.

However, one can observe that building more RSKU houses does not necessarily increase affordable homeownership. The official statistics show that the RSKU homeownership is still lower than expected. Among 189,892 applications for RSKU houses received in the past five years, only 24,243 or 12.8% of them received offer letters and ended up owning the homes offered.

Here we look at the arguments which have contributed to this situation:

1. Rumah Selangorku restrictions which limit the property value growth

Since RSKU is a housing scheme designed to support the low- and middle-income group, it comes with certain conditions attached to the sale that are limiting for homeowners. One of the conditions is that the owner of RSKU houses can neither sell nor rent out the property within the first 5 years of purchase. Such moratorium is to ensure that RSKU houses will not be abused for profit purposes. To note, the state government is drafting a new regulation for disciplinary action against RSKU owners who rent out their properties, following the public complaints on some RSKU owners found renting out their homes.

In case the owner insists on selling their RSKU unit before the end of the moratorium period, consent from the LPHS is required, and the respective unit can only be sold to qualified first homebuyers (B40 or M40). If the unit is a leasehold property, approval for sale is needed from the LPHS, even if the moratorium is up. This inevitably restricts the value of RSKU houses in the secondary market, as the unit cannot be treated as a free-market product.

Furthermore, if the unit is under the category of low-cost houses, consent is needed from the LPHS (regardless of the moratorium) before it can be sold to another party. This is because, in Selangor, there is a policy that once the unit is considered a low-cost house, it shall always remain as so. This is to protect the low-cost houses from falling into the hands of the wealthier income group. However, in terms of property investment, such price control movement has severely affected the value appreciation that the house can contribute to its owner.

The moratorium can be inflexible, especially to owners who are subject to job relocation. A location that was once preferable to the owners could become unsuitable in three-years time – after signing the SPA and until the unit is completed – due to changes in life. As a result, the unit could be left vacant while waiting for the end of the moratorium. The owner has to fork out extra cash not only to maintain the property (as it cannot be rented out), but also to pay for their current property’s rental.

CHECK OUT: 9 things you should know about RUMAWIP

2. Hidden costs of owning Rumah Selangorku houses

The cost of owning a house is not only determined by its selling price. There are hidden costs when purchasing the unit, as well as the ongoing cost of maintaining it over the term of ownership. Most often, first-time homebuyers do not know that buying and financing a house can cost more than just the deposit and the loan – it involves miscellaneous fees and charges such as:

- Stamp duty for the transfer of ownership title

- Sale & Purchase Agreement (SPA) legal fees

- Stamping for SPA & loan agreement

- SPA legal disbursement fee

- Loan agreement legal fees

- Fee for transfer of ownership title

- Government tax on legal agreements

- Bank processing fee for loan

READ: Latest stamp duty charges & 6 other costs to consider before buying a house in 2019

Purchasers of RSKU houses are of no different from those who buy the free-market products, as they need to pay a downpayment of 10% of the house price, in addition to bearing the above charges. Due to the selling price of below RM300k, RSKU purchasers cannot enjoy special property deals and purchase exemptions offered under the nation-wide Home Ownership Campaign (HOC) 2019, including the stamp duty exemption (on MOT) for homes costing RM300k – RM1 million.

This makes buying a free-market product more attractive than buying a RSKU unit in conjunction with the HOC. Most importantly, the lifestyle and quality of living offered by free-market product are perceived as better than what’s offered by RSKU units. Free-market units are also usually located in more strategic locations, with good connectivity to the city centre, good accessibility to infrastructure, and well-integrated with public transportation network. This is not only the key to future property value appreciation but also enhances housing affordability in the long-run, by taking into account the combined housing and transportation costs.

To note, the annual cost of owning a car in Malaysia can range from RM11k to RM23k, with an average annual cost of RM18k or equivalent to RM1,500 per month. The cost impact on car ownership is definitely greater for those owning a RSKU unit, as RSKU houses are usually located in less appealing areas that the owners are forced to rely heavily on private transportation. As such, true affordability is not only about being able to afford to buy a house, but also being able to afford to live in it. This goes beyond meeting expenses related to operations and maintenance; it also involves considerations of transport, infrastructure, and services.

3. Limited pool of eligible buyers

One of the critical challenges faced by the developers in RSKU development is the difficulty in getting eligible buyers. The current RSKU sales process is tedious, and developers are likely to face cash flow problems during the development progress. Since RSKU is only meant for qualified buyers, the developers have to get two rounds of pre-qualified buyers listing from LPHS. Most of the time, only 20% of these buyers are actually interested in the houses offered and are qualified for a bank loan.

It takes the developer 3 months to screen the first round of listing and once the list is exhausted, developers will apply for second round listing from LPHS, which is roughly a 3 month-long wait, and the process repeats itself again. Only after going through the whole process above can the developers can apply for “open day”, when they can officially sell the remaining RSKU units to the public.

All in all, the whole process may take about 12 months before the developers can finish selling their RSKU units. In some cases, RSKU units are still left empty even after years of being launched in the market. The state government often declares that new housing units are unaffordable and that the housing industry is not supplying the so-called affordable units in accordance with the mass-market demand.

However, it fails to acknowledge that most of these so-called “eligible buyers” do not actually earn enough to afford the “affordable houses” targeted at them.

To note, RSKU housing scheme is only applicable to a small segment of the market due to its restrictions. Even though statistics show that there are demands for affordable housing in the state, through the Household Income Survey (HIS), one must understand that these are not effective demands and cannot be treated as “eligible buyers”. Furthermore, amongst this pool of “eligible buyers”, only a small portion of them managed to get a bank loan application.

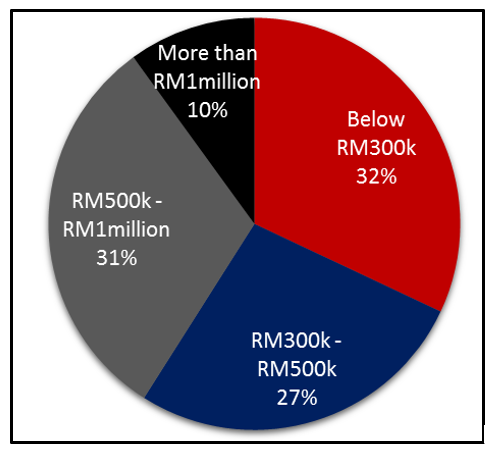

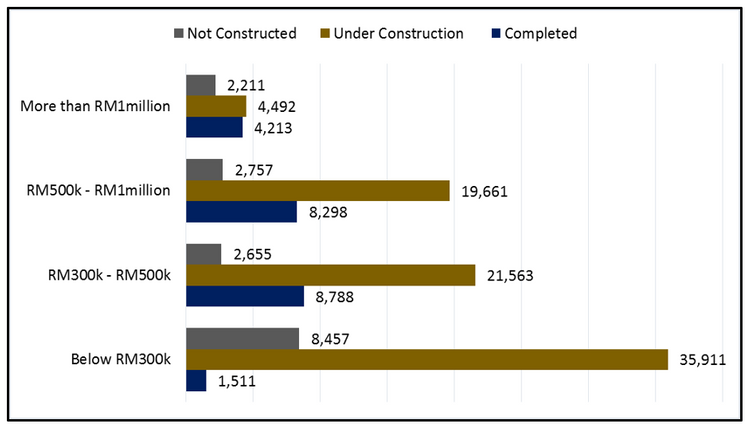

The fact that there’s a high loan application rejection rate (32%) (Figure 1), together with 45,879 unsold units for properties priced below RM300k (Figure 2), should tell the truth that low homeownership for affordable housing is essentially due to the escalating cost of living.

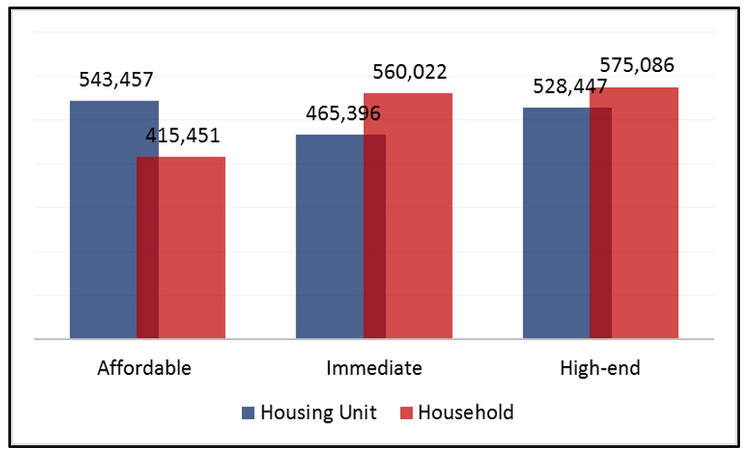

In that sense, what should be a bigger concern is not how many units of affordable houses being built or how fast these houses can be built; but rather, does the market even need these houses during the economic slowdown period. Most importantly, one must realise that there could be a potential threat of oversupply of affordable houses in Selangor (Figure 3)

It is a noble act to help citizens to own a roof over their heads. However, certain segments remain more vulnerable to shocks, particularly those earning below RM5,000 per month due to low take-home pay after deducting existing debt obligations and expenditures. It is dangerous to push these seemingly financially unqualified buyers into the market through affordable housing, because this category of buyers is, otherwise, not directly exposed to the danger of a property market crisis. When the market exhausts the number of buyers and there’s no one left to buy, the market will be at its highest risk ever.

MORE: How does DSR affect my home loan eligibility & how to calculate it?

4. Public’s perception of Rumah Selangorku houses

In general, the public still perceives that RSKU units are associated with low-cost housing – though it is not – due to its limited value growth due to the less-appealing housing quality. There are “eligible buyers” who decided not to buy RSKU houses because they assume the buyers of these houses are relatively of lower education level, bad attitude, lower social class, etc. Most importantly, their main concern is that the neighbourhoods that are defined as settlement of low-income groups may distract high valued investment or physical development, which eventually can contribute to class discrimination or local inequalities.

To note, urban residential house prices depend on two broad factors: (1) tangible factors – characteristics of the dwelling units; and (2) intangible factors – neighbourhood characteristics, services, and environment.

Households residing in a neighbourhood tend to have similarity in socioeconomic characteristics and preferences, such as household income, family size, anticipated services, and neighbourhood characteristics. The presence of low-income households in the neighbourhood is perceived to be associated with social nuisance (less demand for a better neighbourhood environment), whereas, high-income households have both the ability and the willingness to pay premium prices for higher quality neighbourhood services in a more sustainable manner.

Since the intra-neighbourhood similarities are crucial to the public’s perception, and the purchase of a house is the single greatest investment that most people will make in their lifetimes; failing to look at the house as a driver of value can limit the property’s overall performance in enhancing the owner’s income status; which then affects its marketability among potential buyers.

In this sense, LPHS needs to relook its affordable housing strategies by taking into account the concept of marketability, because the present selling price is not the sole factor that the buyer concerns the most, but the potential future value that a property can unlock.

Read this article next: Rethink current housing measures, let’s not send the wrong message to developers and speculators