The newly released HIS report by the Department of Statistics Malaysia sheds some light upon the overhang and oversupply issue that is currently plaguing the local property market.

Overhang and oversupply are two very different terms. Simply speaking, overhang (or unsold units) is a cyclical problem due mainly to the unmet housing demand in association with the varying economic performance, housing preferences, market sentiment, credit accessibility and so on. Property oversupply, on the other hand, is a structural problem where the number of houses is in excess of the number of households, as a result of a failure in complying with the housing planning policy, guidelines, and other determinations as contained in the development plans.

To illustrate this: Assuming there are 100 people living in an area, an oversupply happens when the number of houses provided – let say 200 units – which are more than the existing occupiers, leading to the surplus of houses that are not needed in the market. In contrast, the provision of 50 houses is definitely an undersupply but even so, not all these 50 houses can be fully sold out, simply due to the mismatch of price or product that is not in favour of the end-users’ preference. The unsold units, in this case, are termed as overhang.

What is the history of property overhang in Malaysia?

The definition of overhang has been changing over the years. Let’s look at a summary of the various definitions used over time:

- 1999: The total number of housing units remained unsold after it was launched for sale (irrespective of whether the unit is completed, under construction, or not constructed yet)

- 2000-2002: The total number of unsold units for more than 9 months after it was launched for sale (including completed units, under construction and not built)

- 2003 onwards: The total number of completed housing units with Certificate of Completion and Compliance (CCC) and remained unsold for more than 9 months after it was launched for sale.

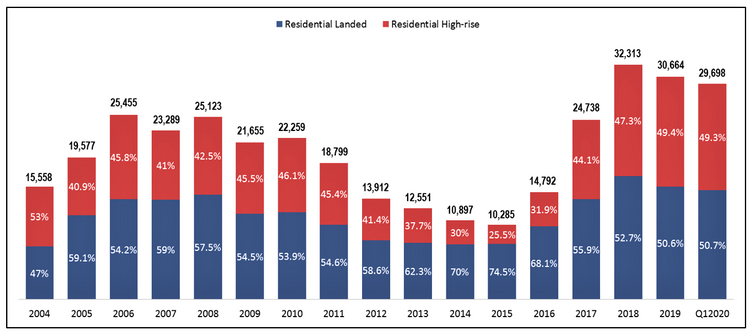

Past experience suggested that the severity of overhang varies with the country’s housing policy and economic performance. During the period of 2004 – 2008, overhangs peaked from 15,558 units to 26,029 units, which is in conjunction with the weak economic performance following the Oil Price Bubble (2003 – 2009) and Global Financial Crisis (2007 – 2009). Since then, overhangs had reduced substantially, from 22,592 units in 2009 to 11,816 units in 2014 (Figure 1), when the market was boosted by easy credit as well as the introduction of the Developer Interest Bearing Scheme (DIBS) to help lower down the buyers’ entry-level.

Again, due to the implementation of various macroprudential and fiscal measures that aimed to curb speculation, the property market had slowed down since 2014, leading to the increase of overhangs that peaked at 32,313 units in 2018.

One can see that overhang always remains there, and to a large extent, its impact to the housing industry relies on the local market condition, which is mainly driven by the favourable lending policy, market optimism from the buyers upon future capital appreciation from property investment, as well as the drumming-up market sentiment from the developers.

While people are unlikely to commit to big and long-term spending right now due to the uncertainties posed by COVID-19, one must recognise that once the vaccine is found or natural immunity is built up, the take-up rate of property will be sure to revive, leading to the reduction of overhang and unsold units in the market.

How did property oversupply contribute to the overhang issue?

While the problem of residential overhangs seems to lessen after its peak in 2018, the inclusion of commercial-titled residences, such as serviced apartments and SOHO units, has seen to the intensifying property glut in the country. In Q12020, the total number of overhangs, encompassing both residential- and commercial-titled residences, recorded at 48,619 units; where 34.8% of the overhangs were contributed by serviced apartment, followed by residential landed (30.9%), residential high-rise (30.1%), and SOHO (4.1%) (Figure 2).

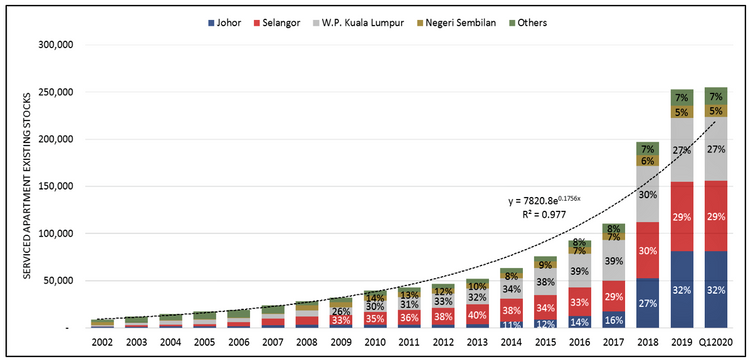

Residential landed and high-rise properties that used to contribute to the first and second-biggest share of overhangs have been replaced by serviced apartments in recent years. Particularly in states like Johor, Kuala Lumpur and Selangor, serviced apartments accounted for a significant portion of overhangs, which is as high as 67.1%, 45.2%, and 23.2%, respectively.

Correspondingly, 88% of the serviced apartment existing stocks in the country were concentrated in these three states – with 32% in Johor, 29% in Selangor, and 27% in Kuala Lumpur (Figure 3). In these areas, a drastic increase of serviced apartments was experienced in 2018, with extensive annual growth of 78.84%, as compared to 2.2% growth of residential landed and 4% growth of residential high-rise properties. This implies that the problem of overhangs we are facing today is neither solely caused by the weak economic performance and market sentiment, nor the desire of property developers to capitalise on high-end products; but to a large extent, the oversupplying of houses that exceed the local market absorptivity.

RELATED: What is the impact of COVID-19 on Malaysia’s property market?

How does the Household Income Survey tie in with property oversupply?

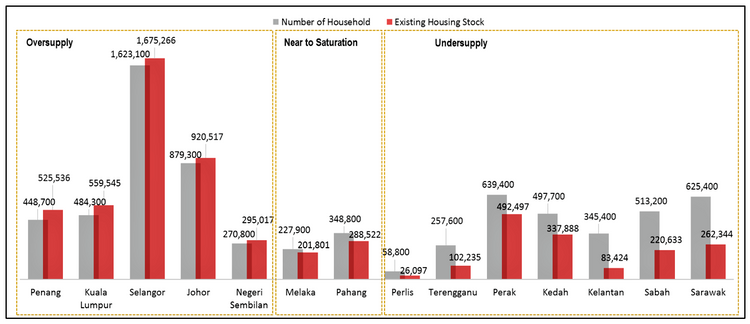

Based on the newly released Household Income Survey 2019 (HIS) by the Department of Statistics Malaysia (DOSM), the total number of households in Malaysia is 7.2 million as compared to 5.7 million residential- and 291,000 commercial-titled residences. This means that there are a total of 6 million existing stocks – which creates an undersupply condition for the property market in the country. This seems like good news as it gives way to a sustainable growth of the industry, as long as the supply of houses is kept under control. However, in terms of local scale, housing supply is outgrowing the housing demand.

As shown in Figure 4, the existing housing stocks – encompassing residential landed, residential high-rise, serviced apartment, and SOHO – exceed the number of households in areas like Penang, Kuala Lumpur, Selangor, Johor, and Negeri Sembilan. While in areas like Melaka and Pahang, housing supply is approaching a point of saturation, owing to the increase of housing provision rate which is much faster than the household growth rate. The remaining areas are in the undersupply condition, with the shortage of houses in Sarawak being the most critical, followed by Sabah, Kelantan, Kedah.

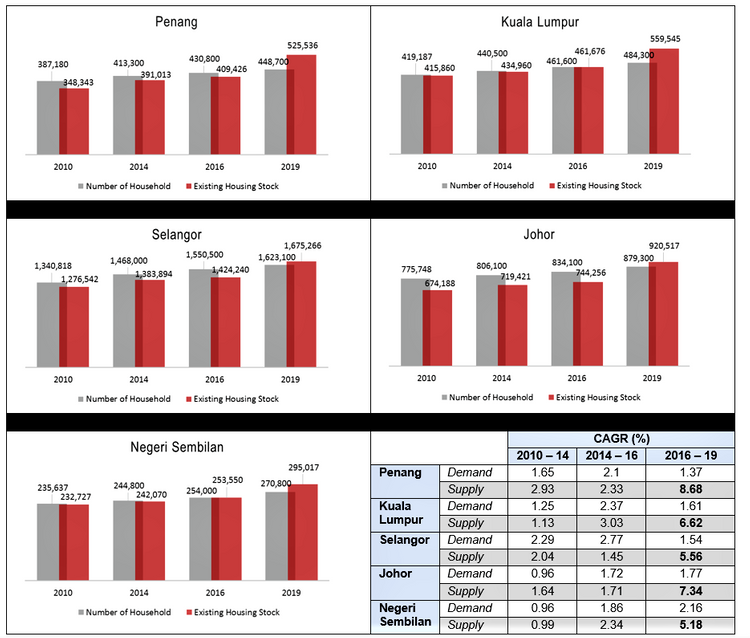

When and how did oversupply come into the picture? By comparing the number of households (demand) and compared against the number of housing stock (supply) within the period of 2010 – 2019 (Figure 5), we can observe that prior to 2014, no oversupply was found in states like Penang, Kuala Lumpur, Selangor, Johor, and Negeri Sembilan. Also, the housing supply rate (calculated in CAGR) is lower or almost in line with the rate of household growth.

This indicates a “healthy” sign to the property market as it offers opportunities for property developers to continuously launch new houses to the market without exceeding the local market absorptivity. Correspondingly, the property market also embarked on an explosive phase in the same period.

MORE: 7 areas in Klang Valley affordable for middle income earners

When did the housing supply in Malaysia begin to outstrip housing demand?

The number of housing stocks started to exceed the number of households in states like Kuala Lumpur and Negeri Sembilan since 2016 and became more apparent in 2019 as the housing supply rate became almost 2 to 4 fold more than the household growth rate. Meanwhile, in states like Penang, Selangor, and Johor, the housing supply rate also began to accelerate and went beyond the demand rate. In Penang, for example, the housing supply rate is 6 fold of the demand rate; while in the case of Selangor and Johor, the supply rate is 4 fold of the demand rate. Since the above mentioned 5 states are the major driver of the whole country’s property industry, any property market imbalances in these states will definitely affect the sustainability of the country’s housing delivery system.

In fact, the property market has been slowing down since 2016. While it is generally believed that the dampened performance is due to the mismatch of house prices and affordability, difficult access to property financing, and so on; the profound impact of housing oversupply should not be overlooked. Today’s overhang is likely the reflection of housing oversupply. This oversupply is likely to remain as a major challenge in the property market for the next couple of years as population growth is expected to decrease, but developers are likely to build more units in smaller sizes due to land scarcity.

What must the government do to tackle the property oversupply issue?

This problem points towards the issue of lack of coordination in planning, and the inability to tackle the effective demand in the market using existing data. It cannot be solved simply by freezing new developments, as such an attempt will tend to exacerbate the problem – when supply reduces, the demand will increase, leading to the shortage of houses that pushes up the house prices.

The solution that has to be developed, at this moment, is to increase the housing supply responsiveness through the establishment of an integrated housing database that consolidates data from multiple agencies at federal, state, and local levels. The current property industry is still relying on data that is biased, historical, and oriented towards approvals. The information obtained from the existing data tends to be on “what has been approved” instead of “what is being built”. Besides, such data is not supported by up-to-date statistics such as demographic and households’ expenditure, thereby hindering its usefulness in reflecting the effective demand of the current market.

A better quality information flow on property can help industry players to gauge market trends, especially in a specific local area. By having these data accessible to all the industry players, a better understanding on how new launches perform in matching the local affordability level is achieved; and hence, an adequate supply and diversity of housing opportunities can be made available in the country.

If you enjoyed this guide, read this next: Quit Rent, Parcel Rent & Assessment Rates in Malaysia