NAPIC recently released its Property Market Report 2019 which showcases the industry performance at a national and state level. Samuel Tan, Executive Director of KGV International Property Consultants highlights important observations in the Johor property market and what we can look forward to in 2020.

1. Johor’s property market performance increased at a slow pace, with residential at the forefront

Johor property market recorded a growth of 4.0% in terms of total transaction volume against 2018. There was a marginal drop of 0.9% in terms of total transaction value. Total transaction volume increased from 41,653 in 2018 to 43,314 in 2019. Transaction value-wise, it was RM19,325 billion in 2018 and RM19,148 billion in 2019. This is quite similar to the reported national figure.

The residential sub-sector in 2019 dominated the market share at 66.7% of the total market activity. At the national level, this sub-sector was at 63.7%. In terms of total transaction value, this sub-sector took 52.8% in Johor and 51.2% nationally.

Valuable Insights

2019 was a stable year for the Johor property market. It synced with the national performance and did not have much changes when compared with the preceding years.

We believe the HOC 2019 which saw a total sale of RM21 billion by last November helped to prop up the market. Under this campaign, the various incentives offered encouraged more buying activities.

Most of the sub-sectors performed within expectations without any surprises. Residential was resilient, although serviced residences /SOHO were grossly over-supplied. Retail saw a small uptick in the occupancy rate but will be challenged by the increased floor space – whereas purpose-built offices will continue with a downward trajectory in its occupancy rate. The industrial sector remains stable with a slight increase in transaction volume and thus, overhang moderated.

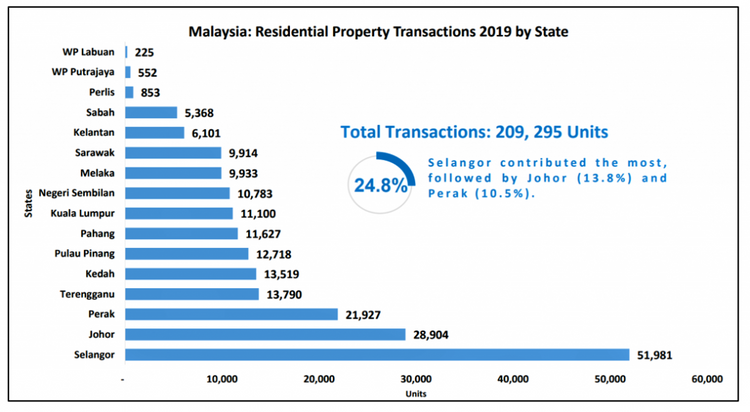

2. Johor contributed the second-highest residential transactions to Malaysia’s overall in 2019

Total property transaction volume increased from 26,885 units in 2018 to 28,904 units in 2019 reflecting a growth of 7.5%. In terms of total transaction value, it grew from RM8,771 billion to RM10,117 billion, an increase of 15.3%. The latter was the highest total transaction value recorded over the last 5 years.

Terraced houses dominated with 53.8% of the total residential volume (15,552 units). Of these, 6,235 units were single-storey terraced houses and 9,321 units were double-storey terraces. There was an increase of 4.5% of units launched in 2019, from 9,294 units to 9,711 units. The sales rate was recorded at 47.5% compared with 44.2% in 2017 and 45.5% in 2018. Two to three-storey terraced houses constituted 53.5% of the total launched units (5,193 units).

The overhang status dropped by 7.8% from 6,066 units to 5,627 units. This is about 37.6% of the total national residential overhang.

About 25.8% of the national overhang are those priced between RM200,000 – RM300,000. Another 23% are those pegged between RM300,000 – RM500,000 while 22% are those between RM500,000 – RM700,000. Approximately 32.2% are terraced houses, 12.8% are semi-detached and detached houses.

Units unsold and under-construction increased by 13.1% from 9,190 units to 10,392 units. Unsold stock and not under construction dropped significantly from 1,291 units to 104 units. Total residential stock by the end of 2019 stands at 838,528 units. Incoming supply amounts to another 59,836 units and planned supply at 79,771 units.

The Johor All House Price Index shows a slight increase of 1.8% with the index moving from 223.5 to 227.3. This shows the slowdown of price growth albeit at a nominal increase. In Johor, the Annual Percentage Change decreased from 6% in 2018 to 3.8% in 2019 whereas the r Average All House Price increased by 1.8% from RM348,420 to RM354,753 per unit.

Valuable Insights

This sub-sector remains resilient in 2019 with a good growth rate in terms of property transaction volume and value. This was reflected in all aspects including an increased number of units sold in new launches, sale rates, decreased overhang, Price Index and Average Price Index.

However, there was a sign of indigestion from the unsold under-construction units which saw an increase of 13.1%. However, this was mitigated by the fact that those unsold stock and not constructed saw a significant drop.

Residential remains to be the most desired sub-sector. A survey conducted by KGV International Property Consultants shows that 25.8% of our respondents expect this sector to recover within the next 2 years. Another 34.1% expect recovery within 3 years.

The property types expected to be popular are the two-storey terrace houses with prices tagged at RM300,000 – RM500,000 (33.1% ) followed by RM500,001 – RM750,000 (21.7%). Based on our survey, respondents also showed interest in serviced apartments. As seen, affordable houses will be the mainstay in 2020.

CHECK OUT: 9 Highlights from NAPIC’s Property Market Report 2019

3. Serviced apartments & SOHO sub-sector remained active in 2019

The total transaction volume for this sub-sector increased by a massive 73% from 298 units to 516 units. Volume-wise, it increased by 85.% from RM128.6 billion to RM238.6 billion. Serviced apartments/SOHO constitutes 13.9% and 7.5% of the total commercial property transaction volume and value respectively.

Johor recorded the highest serviced apartment overhang with 71.2% share in volume and 76.9% share in value of the national total.

There were 12,710 overhang units worth RM11.81 billion, increased substantially by 54.9% in volume and 80.7% in value compared with the previous year. (2018: 8,204 units worth RM6.53 billion). High-rise constitutes 48.8% of the total national overhang.

New planned supply increased by 5.8% from 12,023 units to 12,717 units. Starts for this property type decreased significantly by 52.7% from 7,875 units to 3,724 units reflecting the caution of housing developers. As at the end of 2019, there were 81,989 existing units of service apartments/SOHO units with another 24,695 units in the incoming supply and 61,915 units in the planned supply.

Valuable Insights

This is probably the most worrisome property type as it has a high overhang volume. The majority of these overhang units are located in Johor Bahru district, accounting for 99.2% of the state’s overhang (12,105 units worth RM11.5 billion). The state also holds a 34.0% share (11,490 units) of the country’s unsold under construction.

The 24,695 units in the incoming supply and 61,915 units in the planned supply will add to the pressure in this sub-sector. With the current economic condition, demand for such properties is expected to be soft, adding to the overhang situation when the buildings are completed.

It is imperative that the housing developers take the initiative to clear stocks in 2020. Various incentives including price reduction must be done to ensure that there will not be added overhang. The authorities should consider initiating another HOC to attract buyers with similar offerings to HOC 2019 and more.

2020’s outlook is not exactly rosy. The reduction of the foreigners’ price threshold from RM1 million to RM600,000 for overhang came a little too late. Moreover, the restriction to unsold stock after 9 months from the date of issuance of CCC should be relaxed. Foreign property buyers in Malaysia can refer to this.

The current COVID-19 pandemic will add to its woes as buyers are reluctant to commit to high ticket discretionary purchases during this time. They are likely to stall such purchases until the market begins to show signs of recovery.

The increased auctions of such property type is a dampener as investors will opt to buy from the cheaper auction market. However, units priced below RM500,000 is still expected to move due to its affordability.

4. Commercial property market – Increased in transactions, but dropped in value

The total transaction volume increased by 5.8% from 3,504 to 3,706 units. However, the total property transaction value slipped by 2.1% from RM3.23 billion to RM3.17 billion. At 3,706 units, it represents about 14.4% of the total national volume.

There was a slight increase in the shop overhang from 1,182 to1,288 units. Unsold and constructed units dropped from 58 to 50 units. Unsold stock and unconstructed units increased from 1,757 to 2,193 units.

At the end of 2019, the existing stock was 87,673 units with an incoming supply of 10,677 units and planned supply of 9,601 units. Completion drops from 1,470 to 1,390 units. Construction starts also decreased from 2,827 to 1,863 units. New Planned Supply witnessed a slip from 1,891 to 1,276 units.

Valuable Insights

This sub-sector was subdued after frantic construction activity since 2013/2014. Rental yield rates for commercial units have gone southwards as many sold units remain unoccupied, particularly those in lesser-known locations. However, shops in strategic places remain attractive to buyers and the prices in such locations have increased substantially. The geographical goodwill generated after years of business has fortified them from the economic downturn.

Moving forward, we will continue to see a decrease in new supply. It would still remain a well sought after asset for investors who are seeking recurring income.

FIND OUT: What happens if commercial & residential tenants are unable to pay rent due to COVID-19?

5. Shopping complex sub-sector strengthened as occupancy improved slightly

The performance of shopping complexes improved as the occupancy rate stood at 75.3% higher than the 71.7% recorded in 2018. This sub-sector witnessed an annual take-up of 246,670 sq m, slightly lower than 276,890 sq m charted in the previous year. Among major movements include Plaza Angsana, NSK Ulu Tiram and Pandan, Johor Premium Outlet, Komtar JBCC, Paradigm Mall, U Sentral in Segamat and Today’s Mall.

The new construction activity consists of 7 completions in 2019 which will inject a total of 279,563 sq m of retail space into the market. As of the end of 2019, there were 153 existing shopping complexes (2,392,121 sq m) with 5 complexes (115,784 sq m) in the incoming supply.

Valuable Insights

COVID-19 changes the entire landscape for our future shopping experience. The requirement for social distancing and other healthcare concerns will derail any immediate recovery of the retail market. Any improvements will be progressive and can only be measured over half to one year.

Mall owners will attempt to retain good tenants by offering rebates. Many will have to resort to profit-sharing with a base rental. This arrangement will mitigate fixed cost to the tenants but the advantage leans better in favour of the landlords.

The decreased footfalls will add pressure to this sub-sector. Therefore, shopping complexes must make themselves distinctive and different from others in the pack. Shoppers will become more demanding and would want to extract the best values for their dollars, both in terms of purchase and experience.

READ: What is the impact of COVID-19 on Malaysia’s property market?

6. Purpose-built offices portrayed a downward performance

This property type portrayed downward performance as the average occupancy rate contracted to 71.2% (2018: 75.9%). The annual take-up remained positive at 14,785 sq m lower than 31,786 sq m recorded in 2018.

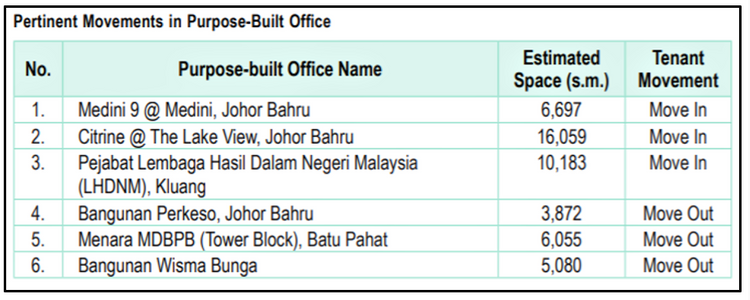

Pertinent movements were observed in this segment, where tenants moved into places like Medini9 @ Medini, Citrine @The Lake View and LHDM in Kluang. Meanwhile, for Bangunan Perkeso, Menara MDBPB (Tower Block) in Batu Pahat and Bangunan Wisma Bunga, tenants moved out.

Rental of office space remained stable. As of Q4/2019, the Purpose-Built Office Rental Index for Johor Bahru stood at 131.4 up by 0.4% from 130.8 points. The Purpose-Built Office Average Rental as at Q4/2019 stood at RM34.54 per sq m recorded in Q4/2018.

Valuable Insights

We opine that rentals will be under further pressure in 2020 due to the oversupply situation. Recalibrated rental rates and packages will likely be offered by landlords to existing tenants to retain them. Similarly, new tenants can be enticed with creative marketing such as rent free period, fit-out and relocation cost.

To revitalise this segment, new drivers must be found. The Singapore Rapid Transit System (RTS) and High-Speed rail Project (HSR) projects are potential game-changers in transforming Johor Bahru as a regional HQ for businesses.

Post MCO, tenants may plan for a less fixed operating cost. For example, some firms may opt for the Working From Homes (WFH) model and co-working spaces may become more popular, attracting an increasingly sizable market.

Purpose-built office spaces in Medini Iskandar should consider giving a tax rebate for the rental paid by their tenants. This is a possibility as Real Property Gains Tax is also waived for properties in this special economic zone. Certain criteria such as minimum CAPEX, minimum headcount or specific services can also be imposed.

7. Industrial property held on, new planned supply increased 6 fold in 2019

The industrial sub-sector recorded 1,016 transactions worth RM2.06 billion, an increase of 17.3% in volume whilst value contracted by 7.6% (2018: 866 transactions worth RM2.22 billion).

The overhang and unsold situation improved marginally. Overhang dropped from 579 units in 2018 to 554 units in 2019. Unsold under construction also decreased from 288 units to 276 units. There was no record of unsold not constructed for both 2018 and 2019.

Construction activity was moderated. However, the new planned supply increased significantly by more than 6 fold. As at the end 0f 2019, there were 17,681 existing industrial units with 1,305 units in the incoming supply and 940 units in the planned supply. Prices recorded mixed movements.

Valuable Insights

We believe that this segment will remain attractive. Post MCO, to avoid disruptions to the supply chain, factories will relocate their plants to various locations/countries instead of concentrating in just one particular location.

During this pandemic, we saw US and Japanese factories planning to relocate some of their plants from China. Malaysia should definitely capitalise on this trend.

Upon recovery of the economy, we believe some Singaporean factories will also relocate their plants to Johor. This is to mitigate the risks faced by them having a limited manpower pool and a higher cost of operation.

Existing factories with smaller floor plates and outdated specifications will find it difficult to attract tenants, however, managed industrial parks will continue to attract buyers. Mega distribution centres will be the new trend moving forth. This in part will be due to the growing demand for e-commerce.

For more insights into the current property market, click here.