In the recent Budget 2020, the government announced that the minimum purchase price for foreign property ownership will be lowered from RM1 million to RM600,000 in urban areas, beginning January 2020.

The latest Federal Government’s Budget which was tabled on 11 October 2019 did not present much allocation for the property sector as most of the initiatives announced – such as the Rent to Own (RTO) financing programme, RPGT amendment and Youth Housing Scheme – are already in place of they are an extension of existing programmes. Among these measures, the proposal for lowering the foreign property buying threshold could be considered as the most surprising one, as it sparked contradictory opinions among industry players.

This may push housing developers to focus on building properties priced above RM600k to target foreign buyers; and eventually, crowding out the M40 income group of local purchasers who are mainly aiming for properties priced at the range of RM400,000 to RM500,000.

Let’s take a closer look at the issue on hand:

Why was the proposal to encourage foreign property ownership introduced?

According to the government, the proposal of lowering the minimum purchase price from RM1 million to RM600,000 is only limited to the unsold existing condominium and apartment units in urban areas. The measure was introduced to help clear the country’s current property overhang dilemma. As of Q2 2019, the supply overhang of condominiums and apartments amounted to RM3 billion. In terms of volume, condos and apartments make up 43% or 14,021 units of the overall residential overhang in Malaysia.

For those who are not convinced by the measure, such a move will be sure to stimulate more foreigners to purchase residential properties in Malaysia – since the country’s house prices are relatively cheaper when compared to other high and middle-income countries in the region including Singapore, Thailand and Hong Kong.

However, there are also concerns that such a measure may further reduce the rakyat’s housing affordability level, as the existing property owners in the secondary market may capitalise on this situation by increasing the selling prices of their properties to target foreign purchasers. This will lead to a sudden rise in property prices across the board and might eventually contribute to a housing bubble in the near future.

READ: What to know about Base Rate (BR), Base Lending Rate (BLR) & Spread Rate when selecting a home loan?

Is it necessary to have such a measure in place?

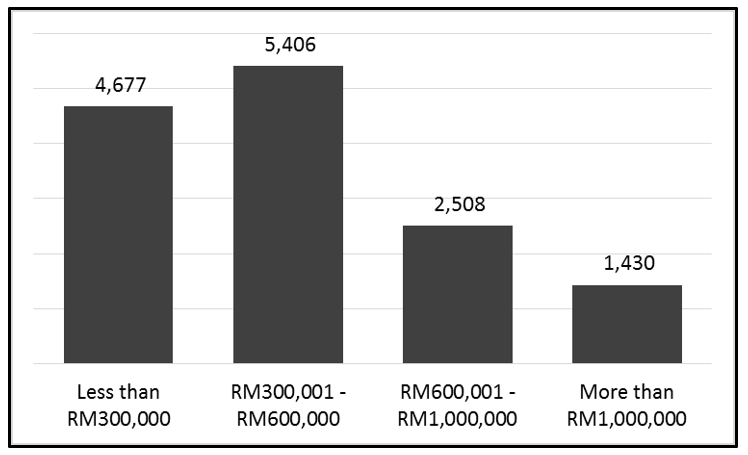

To answer this question, let’s dissect the existing residential property overhang landscape. By breaking down the current overhang for condominium and apartment units into different price categories (Figure 2), you can see that it is mainly contributed by housing products priced between RM300,000-RM600,000, followed closely by the RM300,000 category below.

This means that as high as 72% of the overhang condo/apartments units are targeted for domestic consumption; while the foreign buyers are only eligible to purchase from the remaining 28%.

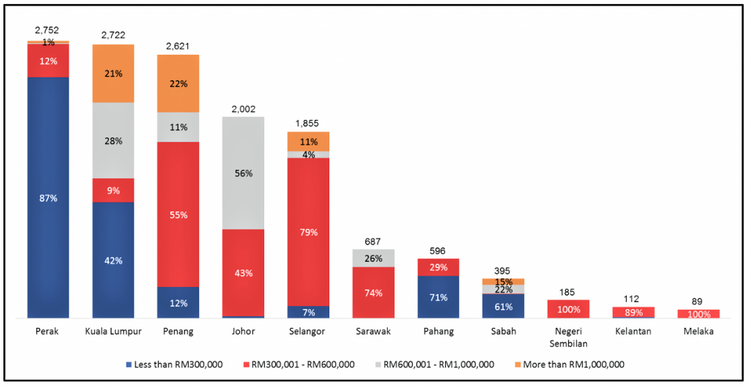

A further study on the condo/apartments overhang units reveals that the majority of them originate from the following five states: Perak (20%), Kuala Lumpur (19%), Penang (19%), Johor (14%), and Selangor (13%).

The property price differs quite a bit between states. It is obvious that products priced below RM300,000 are the major contributor to overhangs in Perak (87%), Pahang (71%), and Sabah (61%)

Meanwhile, in the case of Penang (55%), Selangor (79%), Sarawak (74%), Negeri Sembilan (100%), Kelantan (89%), and Melaka (100%), the main culprit is the RM300,000-RM600,000 price category. If RM600,000 is set as the threshold that separates high-end housing products from the mass-market housing product, one may find that these high-end products are not the main contributor to the property overhang stock.

Nevertheless, this is an exception for Johor and Kuala Lumpur, where high-end products account for 56% and 49% of the total overhang, respectively.

MORE: Why are there so few people buying Rumah Selangorku (RSKU) homes?

How effective is the measure in tackling the country’s overhang issue?

The significant property overhang in the >RM300,000 category is likely contributed by houses built under the various affordable housing schemes, PR1MA in particular, which have always been criticised for its unappealing locations and unfeasible pricing. Thus, it is unsurprising to hear that the Housing Ministry will be cancelling 56 PR1MA projects.

This is especially apparent for Perak, where 87% of the overhang condo/apartment units originates from this price category. Being a state with a relatively lower population density as compared to other more urbanised states, overhangs in Perak are mainly due to the mismatch of product, by launching high-rise housing projects which are not the local population’s preference.

Johor would be the state which will benefit the most from the proposal of reducing the foreign buying threshold since 56% of the state’s overhang are contributed by housing products priced between RM600,000-RM1 million.

Kuala Lumpur is likely to enjoy the benefit as well since 28% of the overhangs can now be opened to foreign buyers. In other words, the effectiveness of lowering the price threshold for foreigners will most likely be reflected in both Johor and Kuala Lumpur.

However, since land and housing is a state matter, the federal government can only enforce the minimum price threshold in Federal Territories like Kuala Lumpur. It is up to the respective state governments to respond to this positively and revise the ceiling price accordingly.

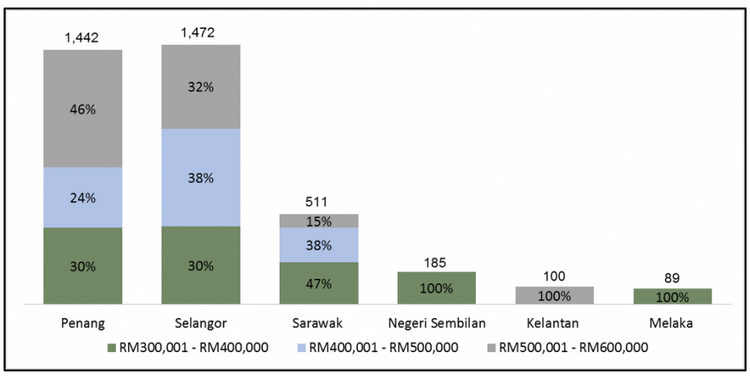

Another finding worth highlighting is the overhang of high-rise property priced between RM300,000-RM600,000 in states like Penang (55%), Selangor (79%), Sarawak (74%), Negeri Sembilan (100%), Kelantan (89%), and Melaka (100%). As one can observe, this housing product category is a major contributor to the high-rise property overhang in these states. A further breakdown on this housing product category can provide a better understanding of the nature of overhang in each state.

Since properties priced between RM300,000 – RM600,000 are considered as “immediate affordable housing” targeted for the for M40 income group, setting the right prices at the right locations is crucial for developers. It is obvious that the mismatch between supply and demand is the main cause for overhang for high-rise properties in Negeri Sembilan, Kelantan, and Melaka. The similar problem is applicable to Sarawak, especially for products priced at RM400,000-RM500,000 and RM500,000-RM600,000; but the overhang of products priced at RM300,000-RM400,000 is likely to be caused by houses built under the affordable housing schemes.

The overhang problem in Penang and Selangor is complicated as it is related to structural problems in the affordable housing delivery system.

Since Malaysia’s housing industry is applying the cross-subsidisation model, there is a tendency for developers to overbuild “overpriced” housing products to cross-subsidize the affordable and low-cost houses that they are mandated to build.

As one can observe, following the domination of housing products priced between RM400,000-RM600,000 in the market, a drastic increase of overhang units in this housing segment is also observed.

The answer is…..

Lowering the foreign buying threshold may help to reduce the property overhang, but the problem will largely remain, as the majority of the unsold units are targeted for domestic buyers. Since this move is just an interim measure to address the ongoing residential overhang in the country – coupled with the restrictions set to limit the eligibility of foreign buyers, as well as the availability of products priced from RM600,000 to RM1 million – the effectiveness of such a measure is less than expected. Likewise, its impact on the local housing market, especially in reducing the housing affordability level, is deemed less significant.

What should be done instead to help solve the overhang issue?

Instead, more concentration should be given on those overhang units marketed as “immediate affordable housing”. It is believed that the increase of unsold stocks in this housing product category is not merely the result of overbuilding, but is closely related to the increasing cost of living and the changing lifestyle trends. Since a large portion of monthly expenses is being spent on buying cars, eating out, entertainment, travelling, health care, and education; it is expected that lesser and lesser household income will be devoted to monthly mortgage repayments. Subsequently, leading to a decrease in the people’s purchasing power in properties.

All in all, a collaborative measure is needed to address the overhang problem. On one hand, developers need to slow down the pace and scale of their project launches, as well as to supply houses which comfortably meets the public’s affordability level. On the other hand, the government needs to increase the rakyat’s purchasing power by helping to improve the workforce’s skill set, job productivity, and national median wage, so as to manage the rising cost of living.

Also, check out How unaffordable are Malaysian homes? Your top 5 questions answered.

Edited by Reena Kaur Bhatt