The Coronavirus pandemic calls urgently for “Help-to-Buy” measures to assist home buyers and we discuss a recommendation on what housing incentives the government can incorporate in the immediate future.

The global economy has weakened significantly as COVID-19 continues its onslaught across countries. A majority of business activities were forced to cease due to the imposed measures to contain the spread of the pandemic. According to the UN Department of Economic and Social Affairs (UN-DESA), the global economy could shrink by up to 1% in 2020 and may contract even further if restrictions on economic activities are extended without adequate fiscal responses.

The Malaysian housing market is not an exception to facing a slowdown. This is reflected in the latest statement made by the Department of Statistics Malaysia (DOSM), where the construction sector contracted by 6.3% in 1Q2020; with the declines in each sub-sector like non-residential buildings, special trades activities, residential buildings, and civil engineering are 11%, 8.6%, 7.6%, and 2.3%, respectively.

Such dampened performance is expected to prolong unless there is a near-term catalyst from the government to revitalise the housing market. However, no provision has been allocated for the property sector so far. The government may be in the opinion that consumers will temporarily move away from buying luxury and big-ticket items in anticipation of a weaker income and employment outlook – but let’s not to forget that housing is both a basic human need and an important component of the country’s economy. The demand for housing is always there, just waiting to be fulfilled.

What is the impact of COVID-19 on Malaysian homebuyers’ sentiment?

As shown by NAPIC’s 2019 Property Market Report, the demand for residential housing has remained strong by recording a 5.3% growth in 2019, and by contributing the biggest weightage to the overall property transaction volume (63.7%). Most importantly, owing to the 2019 Home Ownership Campaign, 61.7% of the residential property transactions were contributed by houses that priced at RM300,000 and below, indicating the very high interest in housing purchase, especially if there is a government initiative to help lower down the buyers’ entry-level.

Unfortunately, such good performance has been clobbered by the pandemic, as people’s debt-servicing capacity is deemed to have deteriorated. There will be a higher number of potential buyers who will abort property purchases following their reduced repayment capacity or spending power. Besides, banks are likely to tighten their lending conditions in order to reduce their exposures to a higher risk of possible default from mortgage payments, making it even more difficult for the first-time homebuyers to enter the market.

What are the current challenges for homeownership among Malaysians?

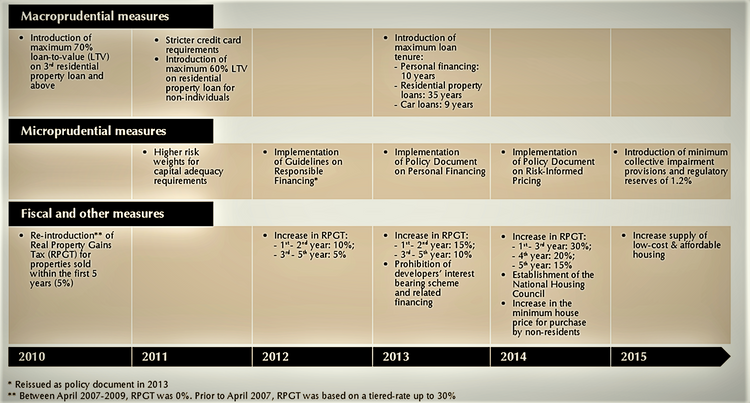

One should realise that the lending guidelines that banks currently pursue are originally formulated to curb speculation which was prevalent in 2010 (Figure 1). These guidelines are strict in approving loans. For instance, the existing lending guidelines require a borrower’s total debt servicing obligations to be below 60% of their income at the point of debt origination.

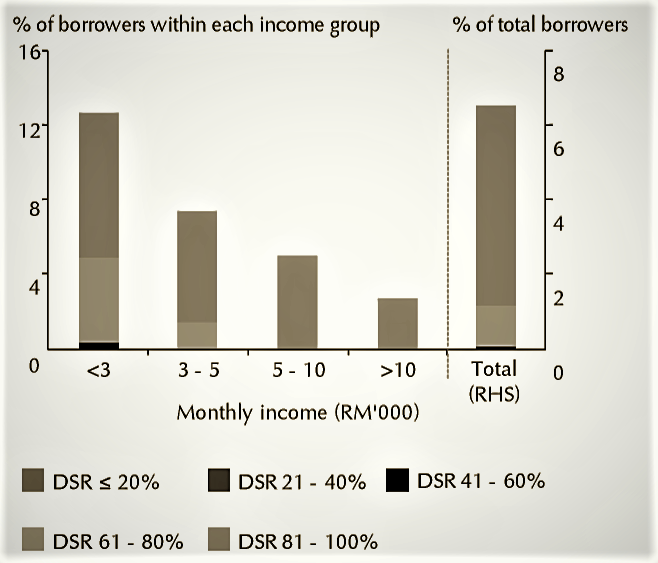

This is because, based on the Bank Negara Malaysia’s (BNM) study on households’ indebtedness, borrowers with a debt service ratio (DSR) of above 60% and with less than RM5,000 monthly earnings, tend to have negative financial margin (FM); and hence, have a greater likelihood to default (Figure 2).

However, the housing market is sure to behave differently post COVID-19. A contraction in both the volume and value of transactions, together with a slower pace of house price increment in the recent years (since 2015) indicates that the speculative herd instinct built up since 2010, has been diminished substantially (Figure 3).

Moreover, one can expect that thinner financial margins (FM) will be a norm for borrowers after COVID-19, as some may not have a steady income stream due to the impaired business activities, or their income just cannot be verified due to recovering repayment capacity. The rejection of home loan applications may trend higher among low to middle-income households, as they are likely to be presented as medium to high-risk borrowers after the economic shock.

MORE: What is Debt-to-service Ratio & how does it affect my home loan eligibility?

What can the government do to assist homeownership amidst a global recession?

In a bid to assist Malaysians with homeownership during the recession, the government should consider formulating a more “relaxed” affordable housing scheme – which is handled specially without following BNM’s rigid procedures and requirements – in order to ease up the home loan process. It can also be seen as a way to jumpstart the property market, as well as the economy, that has been ravaged over the past two months by the pandemic.

This scheme can be in the form of a housing subsidy that directly benefits genuine homebuyers who want to purchase for their housing needs but are temporarily stuck with financial incapability. Also, such scheme can take the form of a government credit guarantee for home loans, in which the government assumes part of the credit risk to act as a shield from risk averseness; and hence, making it possible for an unattractive candidate to obtain credit or improve the terms and conditions under which he/she can borrow.

Instead of solely focusing on low-income and lower-middle-income groups, the proposed scheme can be structured to include the entire spectrum of the middle-income group. The inclusion of the middle-income group should be seen as a kind of economic empowerment, in order to endow them with the ability to maintain or invest further for their own upward mobility, as well as to protect themselves from financial hazards during a recession.

In fact, the middle-income group is the most affected one by the current economic fallout. A large portion of the current M40 households may no longer demonstrate the characteristics of the “aspirational middle-income class” group during the recession. Their consumption pattern is expected to degrade and may exhibit trade-offs in their choice to consume more varieties of basic needs, which is similar to those at the top end of the B40 income group.

In this sense, the government policy and assistance on homeownership should be widened to assist the “middle-income group”. Once this group is able to recover from the shocks and achieve a higher living standard, its lingering effects on the country’s economy is appreciable. This is because it is the pillar to form the entrepreneurial group that brings about innovation and generates jobs in the market, and also exhibits aspirational consumption in the society.

Imagine, if the government is committed to set aside RM10 billion – which is equivalent to only 3.8% of the RM260 billion economic stimulus package or the same amount of allocation to the Rent-to-Own Scheme (RTO) in Budget 2020 – as a guarantee fee fund, there would be at least 100,000 buyers benefiting from it, with the assumption that the proposed scheme guarantees up to 20% of the financing of each property priced RM500,000. If the scheme is set to guarantee only 10% of the financing of each property priced RM500,000, as many as 200,000 buyers will be benefited.

CHECK OUT: How much does it cost to build a house in Malaysia? Here’s a step-by-step guide

What is the impact of having a housing subsidy/credit guarantee in place?

One should realise that such government allocation for a guaranteed fee fund should only be utilised if there is a default; otherwise, it is dormant throughout the period of credit guarantee. In fact, the application of government credit guarantee to ease home loans is not new in Malaysia. There already are two existing government-assisted schemes applying a similar concept, which are: (i) Skim Jaminan Kredit Perumahan (SJKP), and (ii) My First Home Scheme (MFHS). During the recession, the government can put these schemes into better usage by reviewing certain eligibility criteria in order to suit the current situation.

The impact of the proposed scheme on the property sector tends to be huge, as historical data shows us that the average volume of property transactions for the last 30 years (1990 – 2019) is 284,020 units per year (Figure 4). With such stimulus measures in place, the buying sentiment is sure to increase, thereby leading to the fast recovery of the entire housing industry, as well as the country’s economy.

Most importantly, the proposed scheme is not an investment tool that can cause house price escalation, like the Developer Interest Bearing Scheme (DIBS) introduced in 2009 as a stimulus measure to revitalise the housing market after the subprime mortgage crisis. Rather, it is considered as a kind of “housing subsidy” that directly benefits those genuine middle-class homebuyers who want to upgrade their financial profile, as well as quality of life.

If you enjoyed this guide, read this next: BNM’s 6-month loan moratorium: What is it and how can it help you?