| House Price (RM) | 90% Loan (RM) | Tenure (Year) | Monthly Installment (RM) | Required Minimum Household Income (RM) | Gross Household Income (RM) | Grouping |

| 100,000 | 90,000 | 30 | 490 | 2,000 | 3,000 |

Affordable (RM300k and below) |

| 200,000 | 180,000 | 30 | 935 | 3,000 | 4,300 | |

| 300,000 | 270,000 | 30 | 1,368 | 3,500 | 5,000 | |

| 400,000 | 360,000 | 30 | 1,824 | 5,000 | 7,000 | Immediate affordable

(RM300k – RM500k) |

| 500,000 | 450,000 | 30 | 2,280 | 6,000 | 8,600 | |

| 600,000 | 540,000 | 30 | 2,736 | 7,500 | 10,800 | High-end

(RM500k and above) |

| 700,000 | 630,000 | 30 | 3,192 | 8,500 | 12,200 |

With so many affordable home schemes being launched in recent years, there’s still an apparent lack in “immediate” affordable homes today.

The government’s role in the affordable housing market is well-reflected in the newly-launched National Affordable Housing Policy (DRMM), where it outlines the standards, key specification, selling prices, and guidelines for the development of affordable houses. Apart from that, its active involvement is also well-observed in the efforts to keep pushing for the plan of building one million affordable houses in the next 10 years, as well as to spearhead the Home Ownership Campaign (HOC) to combat the property overhang issue.

While the intention of building more affordable houses is good, one must consider if the market is able to absorb such big quantity of affordable houses. Are we really in lack of affordable options in the property market? This is what we found out.

1. What is the current market’s supply and demand status?

According to the DRMM, there is a lack of affordable houses in Malaysia. Only 35% of the Malaysian households can afford to own a home with a price of RM250,000 and only 24% of the newly launched houses are priced less than RM250,000. Hence, more affordable houses are needed to increase homeownership among the low to moderate-income groups. This is an appeal to the most basic economic principles: supply and demand. Add more supply than demand, and prices will drop in response.

One must question if the upcoming “one million affordable houses” is backed by any supply-demand analysis. This is because the existing affordable housing policy tends to give the impression of meeting the numbers, i.e it is a response from the government to the social pressure in providing acceptable housing standards at an affordable price for lower income groups. This could pose a threat to the property market by creating a demand-supply mismatch conundrum.

MORE: Serviced Residences is the “fastest-growing” residential property type in H1 2019

2. We are actually NOT lacking affordable houses. How so?

The real cause of today’s housing affordability issue is never the shortage of new builds. This is evidenced by comparing the existing housing stocks with the total number of households in a specific location. Assuming a family with the gross household income of RM5,000, the respective monthly installments for a house priced RM300,000 is RM1,368 – based on the rule of thumb that the monthly installment does not exceed 30% of the total income – with current market interest rate of 4.2% to 4.4% p.a. for a 90% mortgage loan over 30 years.

If the households are grouped into three income levels (i.e. RM5,000 and below; RM5,000 to RM9,000; RM9,000 and above) based on the eligibility of a household to serve the respective property’s monthly housing loan (Table 1), while the existing housing stocks are divided into three categories based on the average transaction value: Affordable (RM300k and below), immediate-affordable (RM300k – RM500k), and high-end (RM500k and above); one may find that Klang Valley region has sufficient affordable houses to cater for the low-income group.

Table 1: Property prices vs. income level

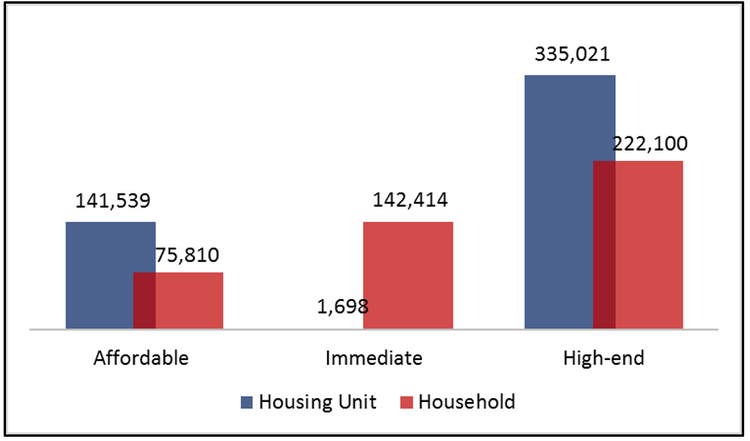

In the case of Kuala Lumpur, if the total number of households with gross household income up to RM5,000 is summed up (75,810 households) and to be compared with the existing housing stocks that are priced up to RM300,000 (141,539 houses); there is a surplus of 65,729 houses within the affordable price range (Figure 1).

In contrast, there is a serious lack of “immediate affordable houses” in Kuala Lumpur, where the eligible households are 142,414, as compared to the existing stock of 1,698.

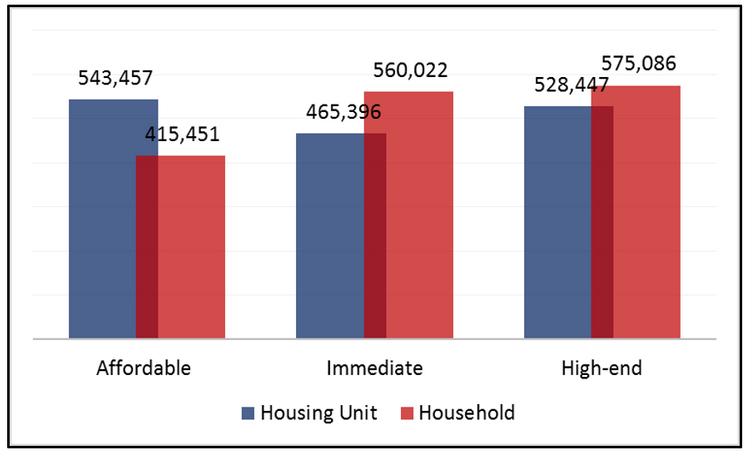

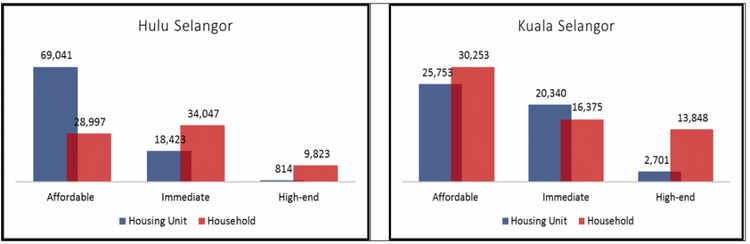

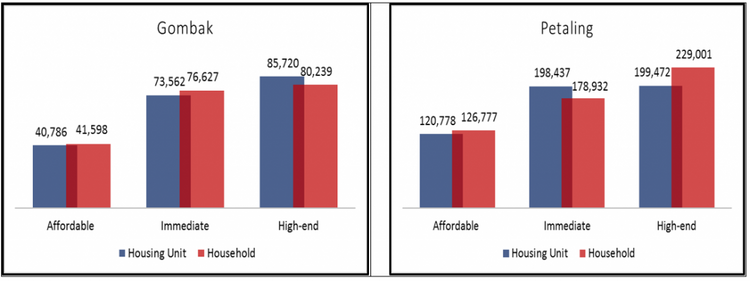

Figure 2 shows similar results for Selangor. In general, there are 543,457 affordable houses (RM300k and below) exist in Selangor, which is sufficient to cater for 415,451 households with a gross household income of RM5,000. On the other hand, there are only 465,396 “immediate affordable houses” (RM300k – RM500k) exist in Selangor as compared to 560,022 households with a gross household income of RM9,000.

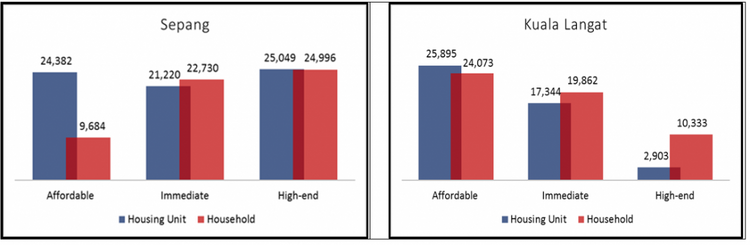

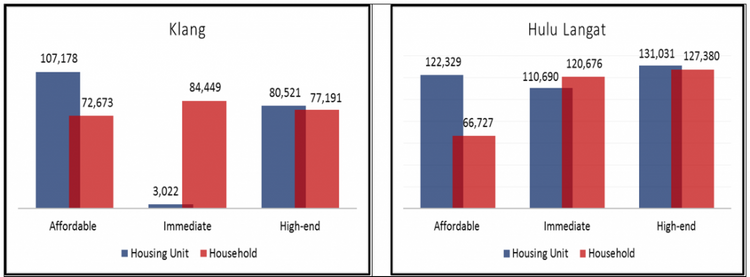

In terms of district level, Hulu Langat, Klang, Hulu Selangor, Kuala Langat, and Sepang are districts that have sufficient stock of affordable houses.

Only the district of Kuala Selangor is apparently lacking affordable houses.

Meanwhile, Gombak and Petaling are districts that have a small deficit of affordable houses.

All these results point to the fact that Selangor, too, is not short of affordable houses (RM300k and below), but are lacking “immediate affordable houses” with prices at RM300k – RM500k.

3. Why are there so little “immediate affordable houses” available on the market?

One must realise that the lack of “immediate affordable houses” is the direct consequence of cross-subsidisation, which can be attributed to the housing policy that merely focuses on quantities in affordable housing provision. Malaysia is the only country in the world where the private sector is imposed with compulsory affordable housing quota across the board nationwide. For example, in Selangor, developers are mandated to deliver a certain percentage of their housing products as a combination of affordable units, regardless of land suitability and the selling price of free-market housing.

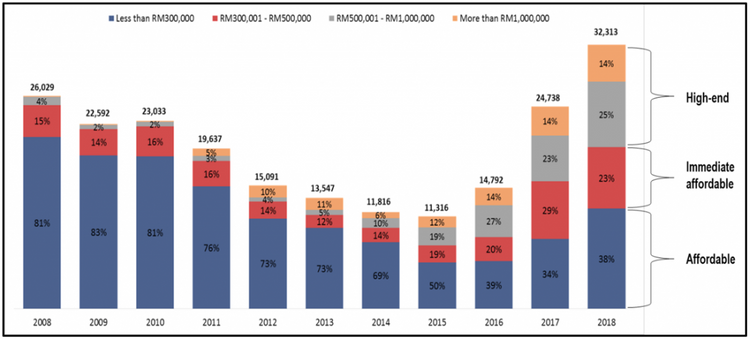

Since the construction of affordable houses is not always viable nor the best option for all projects, coupled with the fact that building affordable houses requires cross-subsidisation by taxing on free-market houses (as the development cost is higher than the capped selling price); the commercially rational response by developers, is to build high-end houses (RM500k and above) rather than “immediate affordable houses”. As a result, overpriced houses dominate the free-market housing segment and eventually leads to the situation of overhang during the market downturn (Figure 4).

Through the experiences of PR1MA, it has been proven that when a KPI is set based on the number of houses to be built within a certain period of time, developers (PR1MA) tend to start chasing for figures and eventually overlook on issues of location, connectivity, infrastructure, amenities, and facilities, which are all key to property sales performance.

At the end of the day, this not only causes the depletion of land, but also worsen the government’s financial burden.

CHECK OUT: 10 things you should know about the MyHome affordable housing scheme

4. Are there any viable solutions?

The government should instead, focus on the delivery of public/social housing or affordable rental housing as a national agenda. Focusing on rental housing and thus channelling more public funds towards its provision, is more advantageous for the country in the long-run as it ensures that the rental units remain as affordable housing stock that can benefit multiple cycles of renters instead of one individual purchaser.

Housing affordability is not an issue that’s caused by a discrete category of housing, but influenced by the wage scheme mainly due to the inefficiency of the government to generate alternative sources of growth, such as productive, skilled, and better-paid employment. It is likely to happen when household income is not increasing in tandem with the overall cost of living, which has greatly reduced the discretionary income and along with it, the people’s ability to afford a house.

In conclusion, it is clear that building more affordable houses cannot solve the housing affordability crisis. This instead, tends to transfer the housing problem from the lower-income group (B40) to middle-income group (M40).

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.