Knight Frank Malaysia recently ran a survey among industry stakeholders in which most respondents expects the logistics / industrial & healthcare / institutional sub-sectors to outperform the overall commercial real estate market in 2019. It is also worth noting that respondents from Sabah are bullish towards the hotel sub-sector, in line with the region’s booming tourism industry.

The survey respondents comprised of representatives in the senior management levels across the property industry. Developers made up half of the respondents (54%), followed by Commercial Lenders (30%) and Fund / REIT Managers (16%).

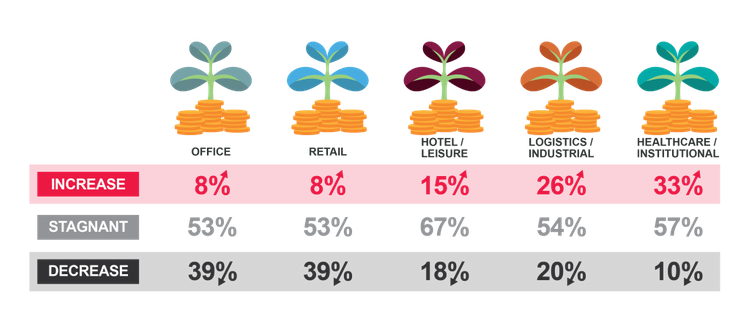

Where will stakeholders invest in 2019?

Developers will be building less office, retail and hotel properties in 2019. Those specialising in logistics / industrial and healthcare / institutional segments will, however, continue to remain active.

Lenders are targeting lesser investment activities in the office and retail sub-sectors in 2019. Instead, they have expressed stronger interests in the hotel/leisure, logistics / industrial and healthcare / institutional sub-sectors.

Fund / REIT Managers will remain active but selective in 2019, gravitating toward the logistics / industrial and healthcare /

institutional sub-sectors where there are lesser concerns of oversupply and are supported by demand and fundamentals.

What are 2019’s most attractive commercial sub-sectors by region?

© Page 2, The Malaysia Commercial Real Estate Investment Sentiment Survey (CREISS) 2019.

In Klang Valley, the logistics / industrial sub-sector is favoured, likely attributed to the strong inflow of FDI in the manufacturing sector. More than a third of respondents anticipate capital growth in this market segment. Despite challenges in the Klang Valley retail market, this sub-sector continues to be favoured, particularly among selected developers. Besides undertaking retail developments, key players are hopeful that their retail assets can become

more competitive upon completion of asset enhancement initiatives (AEIs).

Penang – The Pearl of The Orient continues to be favoured for its hotel / leisure and healthcare / institutional sub-sectors, supported by its UNESCO World Heritage Site of George Town and its many attractions as well as its position as

a leading medical tourism destination in the country. The southern region of Johor remains attractive for the logistics / industrial sub-sector as the state maintains its position as the leading investment destination in the country for the manufacturing sector.

Last but not least, Sabah – The Land Below the Wind, continues to experience a tourism boom with tourist arrivals recorded at 3.8 million in 2018. Supported by its rich natural environment and cultural diversity, the potential for its hotel / leisure sub-sector remains positive.

Healthcare & Institutional (Education) leads the way in 2019

By 2040, roughly 14.5% of Malaysians will be aged 65 and older, as compared to only 5.0% in 2010. The perfect storm caused by an increase in the ageing population has created tremendous opportunities for healthcare and its related sub-sectors.

In tandem with Malaysia’s demographic shift, this presents multiple avenues for key players to capitalise on this macro trend. In fact, several notable developers have started to incorporate healthcare/wellness elements into some of their township developments.

Besides the development of hospitals, key players are also exploring the potential of age care and senior living facilities in established neighbourhoods to cater to this growing segment of the urban ageing population who are independent, financially stable and have travelled the world. However, the feasibility of the various business models must be carefully evaluated by key players before making inroads in this niche market segment.Malaysia’s demographic shift, coupled with the nation’s booming medical tourism industry, has made the healthcare sub-sector a diamond in the rough, due to its sustainable growth potential.

The survey results revealed that 33% of the respondents anticipate an increase in the yield of healthcare / institutional assets in 2019.

Keith Ooi, Executive Director of Valuation & Advisory in Knight Frank Malaysia, says, “Unlike the conventional assets, healthcare and institutional real estate are alternative specialised asset class that is less reliant on the economy. From the investors’ point of view, this specialised asset class is attractive as it provides certainty, by offering long-term leases with a step-up rental.”

On the other hand, along with the growing importance of education, parents in Malaysia are increasingly willing to pay a premium to enrol their children in schools offering quality and holistic education.

Private and international schools have become a key driver to the success of a few townships, both existing and new / upcoming, such as Desa Parkcity, Kota Damansara, Setia Alam, Bandar Rimbayu, Tropicana Aman and Taman Equine.

Alpha REIT, Malaysia’s first full-fledged education REIT, currently owns Sri KDU School and The International School @ ParkCity. Both assets cater mainly to the middle and upper-income population segments. The fund is still actively seeking to acquire well performing institutional assets, capitalising on Malaysian parents’ willingness to invest in their children’s education.

James Buckley, Executive Director of Capital Markets in Knight Frank Malaysia, says, “Investing in the healthcare and institutional assets, such as education, is still a fairly new trend in Malaysia. However, it is possible that more deals will come to fruition from this sub-sector, with investors being attracted by its defensive qualities as it is less reliant on the general state of the economy, offers long leases and often comes with fixed increases in rent throughout the duration of the lease.”

In addition to investing merely in schools, investment opportunities are also aplenty in related assets, such as the likes of purpose-built student accommodation to cater to the changing needs of Gen Z and also co-living facilities catering to the mobile millennial workforce. As a matter of fact, purpose-built student accommodation has already become an asset class of its own in developed markets such as the United Kingdom and Australia.

In conclusion, the complementary benefits brought by institutional assets, coupled with insatiable demand for quality education, especially among elite families are strong reasons why key players shall start paying more emphasis towards the institutional sub-sector.

You can download the full report here.

Edited by Reena Kaur Bhatt