A journey of a thousand miles starts with a single step – don’t dream of purchasing a house if your finances aren’t in order. Here’s how you can plan a personal budget that you will actually stick to.

What can you buy with RM76? A nice dinner for two in a moderately upmarket restaurant? A presentable outfit for an important work meeting? Well, if you can afford these, kudos to you!

A recent study by Khazanah Research Institute found that RM76 is all that an average B40 Malaysian household (household income not exceeding RM3,000) has left, after deducting their household expenses!

But let’s be honest here, it’s not just the B40 group who struggle financially, most middle-income earners also live from paycheck to paycheck each month. You may be earning RM4,000, RM5,000 or even RM6,000 – but you may still find yourself broke at the end of the month, so let’s not even talk about having a proper savings account.

However, if you are ready to turn over a new leaf, read on!

Say hello to the 50/20/30 Budget

Developing a budget that suits your current lifestyle and long-term plans can help you avoid falling into the “RM76 trap”.

One of the most popular budgeting rules out there is the 50/20/30 rule. It was created by the mother-daughter tag team, US Senator Elizabeth Warren and offspring, Amelia Warren Tyagi. In fact, they wrote a whole book about it: “All Your Worth: The Ultimate Lifetime Money Plan”.

The 50/20/30 rule has been recommended by the likes of Forbes magazine, Investopedia, and NBC. It’s so popular because it is easy to understand, simple to use, and leaves room in the budget for some fun. Yup, you read that right – FUN! Allow us to explain.

READ: Should I buy a house now or wait?

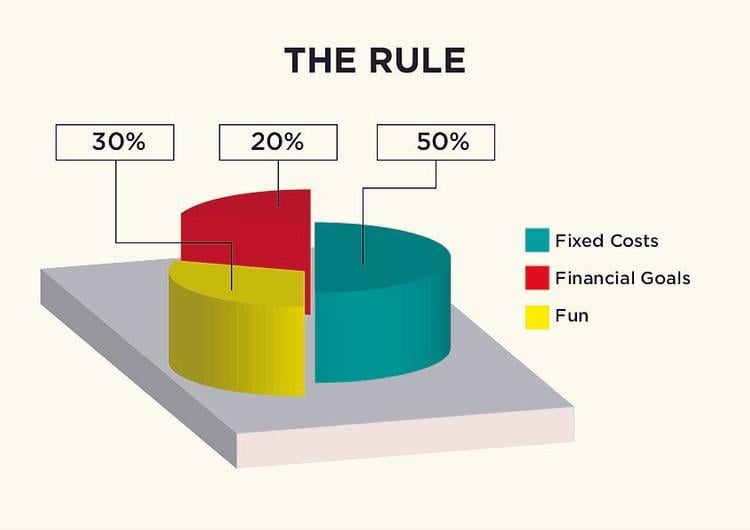

The underlying rule: The three “F”s

This rule is a percentage-based rule which, according to its creators, is suitable for all income brackets. You simply have to divide your total after-tax income into three F’s, and voilà – you’re all sorted.

The first F, which should make up 50% of your income, is for your Fixed costs. The second, at 20%, is for Financial Goals. And here’s the FUN part: the last F, a whole 30% of your monthly income, is for whatever your heart desires!

Here’s how you can do it in 4 simple steps

Step 1: Calculate your after-tax income. If you have a regular income, just look at your payslip. If you are self-employed or a freelancer, calculate your average monthly earnings after taxes.

Step 2: Calculate your fixed costs. This should ideally be within 50% of your after-tax income. If it’s more than that, take a hard (and yes, we know, painful) look at your expenses in this category. Can you downgrade your internet plan? Find an additional housemate to reduce your home rent? Try to do whatever it takes to bring the percentage down to 50%.

Step 3: Calculate the amount that you normally set aside for items under the financial goals category. If it does not already reach 20%, assign more of your income into savings or investment and this also includes savings for the downpayment on your first home.

Step 4: Go crazy with the remaining 30%!

Is the 50/20/30 Budget to good to be true?

Easy to understand? Check. Simple to use? Check. Fun? Most definitely check!

Nevertheless, many people have pooh-poohed the 50/20/30 rule, saying that it is not as universal as it claims to be.

First of all, living standards may not be the same everywhere. For example, the cost of rental and groceries in KL or Penang would be considerably more than, say, in Kuala Terengganu. Hence, allocating 50% for fixed costs may be too much or too little depending on where you’re based.

Secondly, some might disagree over the fun portion as fun should not be prioritised over settling any outstanding debts and savings. They argue that by keeping only 20% aside for financial goals, this drags out debts longer (which is never a good idea) and diminishes your long-term financial security. Well, they may have a point there.

And finally, the 50/20/30 budget may not make sense for every income bracket. While it may be quite suited for most of us middle-income earners, low-income households may have no choice but to spend more on fixed cost essentials (as seen in the Khazanah study above). Likewise, if you are a high-income earner, you may have a hard time finishing your very large 30% fun quota every month.

Ultimately, customise accordingly to make it work for you

Don’t tell the Warrens, but we think it’s perfectly okay to tweak the 50/20/30 rule to suit your own financial status and priorities. For example, those in high cost-of-living areas may decide that a 60/20/20 budget makes more sense. Those with higher debt may want to swap around the percentages for financial goals and (maybe less) fun.

And for those who have a really hard time trying to save anything, there’s a rule for you too. The 80/20 rule gets you to put aside 20% of your income in a more inaccessible savings account like Amanah Saham as soon as you are paid, leaving 80% for absolutely everything else.

Whichever budgeting rule you choose, the golden rule for making it work for you is to stick to it! Get a Buku 555, a budgeting app, or a very strict spouse to be in charge of finances – and remember, No Cheating!

*This article was repurposed from “Did You Know You Can Budget but Still Have FUN – No Cheating Involved!“, first published on Loanstreet.com.my | Edited by Reena Kaur Bhatt