| Similarities | HouzKEY Homebuyers & Direct-Buy Homebuyers |

| Ownership | The homebuyers immediately becomes the legal owners of the property upon completing the transaction. The buyer gains full ownership rights and responsibilities from the start and can sell the property for gains if appreciation |

| Responsibilities | The homebuyers are responsible for all costs associated with the property from the moment of purchase. This includes property taxes, maintenance, repairs, and any other ownership-related expenses. |

Always wanted to own a home but struggle to save enough for the down payment. Well, Rent-to-own (RTO) schemes might just be your ticket to home ownership. This guide outlines what you need to know about current RTO schemes in Malaysia and the pros and cons to help you decide whether it’s right for you.

With Rent-to-Own (RTO) schemes, aspiring homeowners have a more affordable and flexible option to climb the property ladder. Its accessibility, and equity-building aspects make them appealing options. Let’s take a look at what the RTO is all about and how you can benefit from it.

What is Rent-to-Own (RTO) and how does it work?

Rent-to-own (RTO) is a homeownership scheme that allows you to rent a property for a fixed period, which could be 12 months to five years or even longer, with the option to buy it in the future. It’s akin to the Buy Now, Pay Later (BNPL) schemes in Malaysia.

For BNPL, you buy items first and pay later. So, you settle the purchase price in full the next month or across a set number of monthly instalments. In the context of RTO, the same concept applies, where you rent first and own later.

In an RTO scheme, a portion of the rent is set aside as your down payment, and at the end of the lease, you have the option to purchase the property using the accumulated down payment and taking out a mortgage for the balance. Thus, RTO can be a good option for first-time homebuyers who may not be able to afford a down payment or qualify for a property mortgage.

Although a down payment is not required, the potential homebuyer will still need to pay a refundable security deposit, which could be roughly 5% of the property price.

READ: Should You Take a Personal Loan for Property Down Payment or Renovation?

What is the process of the RTO scheme?

Here’s a quick look at the process of taking up a Rent-To-Own (RTO) scheme.

- You select a property that offers an RTO Scheme.

- Developers/parties who provide funding for schemes, such as banks, require you to sign lease documents.

- Security deposits are usually refundable, which are around 5% of the property price, as opposed to 10% down payment for a regular property purchase

- Once all formalities and legalities are completed, you can move in.

- Rent is paid according to the lease terms during the rental period.

- Once the lease term has matured, you have two choices:

- Exercise your right to purchase the leased property at the locked-in rate when you signed the lease; or

- Waive your right and not purchase the property

What are the benefits of RTO?

- You need less to start your property ownership journey.

- You can move in and get to know the neighbourhood first-hand, to uncover any potential issues with the property and/or surroundings.

- Payments are often lower than renting.

- You get to lock in the purchase price of the property based on current market value; the sale price doesn’t change even if the property’s market value goes up in the near future.

- If the property value increases over time, you benefit from this capital appreciation.

- If your credit score is low, you get some time to fix your credit score.

- If you decide not to purchase upon expiry of the lease agreement, you can use the refundable deposit for other investment purposes.

What are the risks of RTO?

- If you default on your rent payments, you could lose the property.

- You are likely to end up paying more overall compared to a traditional mortgage, as you have to go through the entire lease period and then the bank loan’s period.

- Requirements such as having a stable income, and a good credit score are still needed to qualify for most RTO schemes. Not everyone will qualify.

- You may not qualify for a mortgage at the end of the lease period.

- During the RTO period, you’re not the owner until a sale has taken place.

- Depending on the terms of the lease, you might not be allowed to renovate or make any changes during the RTO period without the owner’s approval.

- If the property’s market value drops, you aren’t able to purchase the property at the lower/dropped value. You’ll have to buy the property at the price that was agreed upon during the signing for the RTO scheme.

What are the available Rent to Own (RTO) schemes in Malaysia?

1. Maybank Islamic HouzKEY

Maybank Islamic’s HouzKEY is a homeownership financing solution that helps first and second home Malaysian buyers towards owning a property. It is based on the Shariah contract of Ijarah Muntahiyah Bi Tamlik, where a lease contract ends with ownership via sale.

Maybank Islamic HouzKEY is available for properties offered by their partner developers which include new launches, under-construction and completed properties.

Key features of Maybank Islamic HouzKEY

- Tenure: Starts with a 5-year tenure (initial tenure), with the flexibility to continue for up to an additional 30 years. Maximum tenure is 35 years, or up to 70 years old, whichever earlier. Monthly payment is low in the first 5 years.

- Financing: 100% financing, and no down payment is required.

- Deposit: Three months upon signing the HouzKEY Agreements with the bank and the Sale and Purchase Agreement (SPA) with the developer. Deposit is refundable if there’s no outstanding sum due and payable to the bank including any cost of repairs, replacements or damage to the property.

- First payment: Only starts upon Vacant Possession (VP) as the payment during construction is financed and deferred.

- Expenses & charges: The applicant is responsible for the maintenance fees, utility charges, quit rent, insurance/takaful and so on, throughout the HouzKEY tenure.

During the initial tenure, the financing rate is referred to as the Campaign Rate, while the subsequent tenure is referred to as the Profit Rate.

Eligibility requirements

- Malaysian citizen

- 18 to 17 years old

- Must not have more than 1 home financing, including HouzKEY, at point of application

- Only one main applicant

- May provide up to 3 guarantors; must be members from immediate family such as parents, siblings, spouse, or children

How to apply Maybank HouzKEY?

- Select the project that you are interested in.

- Click ‘Register Interest’ and fill in your details.

- The developers/agents will get in touch with the applicant.

- Alternatively, interested purchasers may make a booking with the participating developer directly and apply for HouzKEY.

What documents required to apply HouzKEY?

- NRIC

- Employed (salary earner)

- Latest 3 months’ consecutive salary slip

- Latest EPF statement

- Latest 3 months’ bank statements (if non-Maybank crediting salary)

OR

- Self-employed

- Latest 6 months’ bank statements

- Latest consecutive 2 years’ B/BE Form (with tax receipt)

- Latest 2 years’ Financial Account Statement/Management Account

- Latest SSM search

AND

- Other supporting documents to strengthen the application

- Latest BE form with tax receipt

- 2 years’ EA form for non-contractual bonus

- Employment confirmation letter on fixed bonus

- 6 months or up to 1 year’s bank statement or commission/variable allowance/overtime/service points vouchers

- 3 months’ pension statement

- Copy of ASB book or Tabung Haji reflecting customer’s name and latest balance

- Copy of Fixed Deposit certificate

- Valid tenancy agreement not less than 6 months from expiry date, or 6 months bank statement showing rental income and property ownership evidence.

Is Insurance / Takaful coverage required?

There are three types of insurance / Takaful coverage that are relevant for properties under HouzKEY:

- Fire Insurance / Takaful

- It is mandatory for homebuyers to take Fire Takaful to cover the property. The annual contribution will be charged to homebuyers as part of their monthly billing.

- Life Insurance / Family Takaful

- This is optional, but recommended for homebuyers to take up; based on the property settlement price to ease their appointed nominee in the event of homebuyer’s demise.

- Takaful on Death / Total Permanent Disability

- This is optional, but recommended as it covers the monthly payment in the event of death or Total Permanent Disability.

- Latest projects/developments: Here

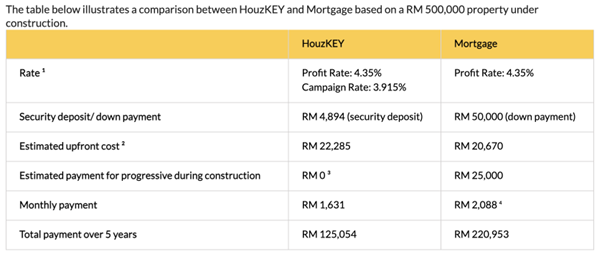

According to Jonathan Ng, mortgage specialist from Smart Choice Solution Sdn Bhd, these are the similarities and differences between HouzKEY and direct-buy.

Similarities between HouzKEY and direct-buy

Differences between HouzKEY and direct-buy

| Differences | HouzKEY Homebuyers | Direct-Buy Homebuyers |

| Criteria | Must not have more than 1 home financing at the point of application | No limitation |

| Financial commitment | Lower upfront cost (no down payment, no progressive interest during construction), and lower monthly payment for first 5 years (initial tenure) | Pay 10% down payment and serve normal monthly payment after vacant possession (VP) |

| Extra cost | Pay extra cost (estimated 1.5% of purchase price) after 5 years (initial tenure) to continue the loan, and serve higher monthly payment for the rest of loan tenure | No extra cost & serve normal monthly payment as usual |

2. Smart Sewa Scheme

This is an initiative by the Selangor government. The Smart Sewa scheme provides an opportunity for low and middle income groups to own a home (Rumah SelangorKu Harapan and Rumah Idaman).

Key features of Smart Sewa Scheme

- Rental: 2 to 5 years

- Return: A 30% return of the total rental is paid and used as a deposit if the tenant can buy the property within the stipulated 5 years.

- Right to purchase: Available by the end of the lease term. If the offer is not taken up at the end of the contract, the tenants will have to move out. However, the tenants will be entitled to a 30% refund of rental paid during the lease term.

Eligibility requirements

- Malaysian citizen, including spouses.

- Aged 18 and above, with discernible financial or family commitments. Monthly family income:

- i. Not more than RM5,000 a month for Type A or low-cost housing

- ii. Not more than RM15,000 a month for Type B, C, and D properties, including affordable and low-cost housing (priority to those with family income below RM10,000/month).

- Applicants and/or spouses must live or work in Selangor.

- Applicants must not own any property in Selangor. If they do own a property, it must be located more than 50km away from the applied location and within a 25km radius of their workplace.

- Applicants must be registered voters in Selangor.

How to apply

- Apply online at the SSIPR website:https://ssipr-daftar.selangor.gov.my/register

- Register for an account.

- Log in to your account.

- Provide all required details and submit your application.

- Download the form at this website: http://phssb.com/syarat-syarat-kelayakan-skim-smart-sewa/

- Print the application form

- Fill in the application form.

- Mail the completed form, along with necessary documents to:

- Pejabat Pengurusan Perumahan Dan Hartanah Selangor Sdn Bhd

- Tingkat Bawah, Blok A,

- PPR Kg. Baru Hicom, Jalan Bukit Belimbing 26/38,

- 40400, Shah Alam, Selangor Darul Ehsan.

- You may also scan and email to: [email protected]

- The applicant will be notified of the interview date upon receipt of the form and complete documents.

- Latest projects/developments: Here

3. RTO scheme under the Melaka Housing Board (LPM)

The Melaka government aims to increase the number of homes under the rent-to-own (RTO) scheme for low-income B40 housing projects. Through the RTO scheme under the Melaka Housing Board (LPM), there are up to 1,150 houses involving 1,100 People’s Housing Project (PPR) homes in Tehel and 50 Rumah Sejahtera units in Lipat Kajang, as at May 2023.

Rental: A monthly rental fee of RM200 to RM300, subject to the price of the premises.

Click here for more info: https://lpnm.gov.my/en/

4. RTO scheme by the Penang government

The rent-to-own scheme was introduced in Budget 2020, and Penang is targeting to build 180,000 affordable housing units by 2030, of which 10% will be placed under the RTO scheme.

State Housing, Local Government, Town, And Country Planning Committee Jagdeep Singh Deo notes that 2,474 units are currently on the list, and welcomes the participation of other developers, especially government-linked companies (GLC) to offer RTO schemes in their housing projects.

In July 2022, it was reported that the State Government intends to expand homeownership in Penang through RTO, which only involves Type A and Type B Affordable Housing (RMM).

Previously, the RTO scheme was only for RMM Type A (low cost house at RM42,000) and RMM Type B (low medium cost house, RM72,500). They intend to expand to RMM Type C (starting from RM150,000 to RM300,000), and two projects that have been identified to offer 44 units by RTO. The priority for this category is for civil servants.

Eligibility requirements

- Malaysian

- Aged 21 years and above on the date of application

- Born in Penang or a resident in Penang

- Registered voters in Penang

- Working in Penang

- Husband and wife’s income does not exceed RM2,500: For Affordable House A maximum price of RM42,000

- Husband and wife’s income does not exceed RM3,500: For Affordable House B, maximum price of RM72,500.00

- Husband and wife’s income does not exceed RM8,000: For Affordable Housing C1, maximum price of RM150,000

- Husband and wife’s income does not exceed RM10,000: For Affordable Housing C2, maximum price of RM200,000

- Husband and wife’s income does not exceed RM12,000: For C3 Affordable Housing, maximum price of RM300,000

- For the Type A / Type B Affordable Housing application, the applicant and spouse must not own a house in any state in Malaysia; or

- For the Affordable Housing Type C1, C2 and C3 application, applicants and spouses who own a house priced below the price of the Affordable Housing applied for (provided the previous home ownership is after 2008) are eligible to apply.

- For the civil servant category, applicants must submit a letter of support from the respective Head of Department.

- For the Talent and Skill Group category, applicants must submit a letter of support from Invest Penang.

- Latest projects/developments: : Here

5. Jauhar Prihatin RTO scheme in Johor

Kumpulan Prasarana Rakyat Johor Sdn. Bhd. (KPRJ) is a private limited company wholly owned by the Johor government. Juahar Prihatin targets the M40 and B40 groups as the main target of this initiative. This scheme also provides a platform for this group to own their own home in less than 5 years.

Eligibility requirements

- Preference given to residents of Johor or Malaysian citizens who have resided in Johor for more than 10 years.

- Aged between 18 and 45 years old, and married or have dependents.

- Gross household income of RM1,500 to 10,000 per month (according to the category of house applied for).

- Applicant or spouse does not own a home / first home.

- Not a bankrupt.

- Registered voters in Johor.

- Details here: https://kprj.com.my/jauhar-prihatin/

Does PR1MA have a Rent-to-Own Scheme?

Previously, the PR1MA RTO scheme was tabled during Budget 2021 and effective until 2022. To date, there aren’t any updates on a PR1MA RTO scheme. However, if you’re interested in PR1MA homes, click here.

Is RTO right for me?

RTO may be a good option for you if you’re looking to buy a property, but don’t have enough for a down payment just yet. It is also a good option if you want to try out a new neighbourhood before committing to buying a property there.

It’s important to weigh the pros and cons of RTO before deciding if it’s right for you. You should also do your research to find a good RTO scheme. And of course, calculate all fees and interest charges to determine if the RTO scheme suits your budget before signing the agreement.

You’ve got this! Stay focused on your goal, and soon enough, you’ll be able to call that place your own!

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.