This article showcases how Malaysian property developers have performed over the past decade. It is intended to serve as a guide for assessing property development companies that are listed on Bursa Malaysia.

Property development involves many stages. It starts from acquiring the land, getting planning approval from the local authorities, and handing over the completed property aka delivery of vacant possession. Depending on the type of project, it can take 4 to 6 years to complete one cycle.

Because of this long cycle, the impact of a particular government policy or company action may only be seen a few years down the road. It takes time for changes to flow through the pipeline. Thus, the real estate sector can be said to be alike to a big ship. A big tanker with full gears in reverse may require as much as 5 km before it can come to a complete standstill. A 500 ft, 8,000-tonne ship needs over a third of a mile to turnaround.

If a property developer stops launching new housing projects for a year or two, you would not see the impact of this until 2 to 3 years down the road. Investors who are looking to get into the real estate sector, have to appreciate this “big ship” analogy. You need to think long-term rather than just looking at current results.

2020 has been a very challenging year for the Malaysian property market because of Covid-19 and the measures taken to control it. Keeping the “big ship” approach in mind, you cannot just look at the past year’s performance, instead, investors need to look at the past decade.

The past decade had been very challenging for the property development industry. The industry started the decade in 2010 on a very positive note. However, the government soon instituted a number of cooling measures to reduce real estate speculation. These included:

The Developer Interest Bearing Scheme (DIBS) was banned.

The minimum property purchase price for foreigners was raised from RM 500,000 to RM 1 million.

There was a cap on the loan-to-value ratio for third house purchases.

Many of these real estate measures were implemented in the first half of the decade. But the big ship effect meant that the impact was felt years down the road. Join me as I explore how the industry fared during the past decade.

How did the Malaysian property industry fare from 2010-2020?

To answer this question, I tracked the performance of all the real estate companies under the Malaysian stock exchange or KLSE from 2010 to 2020. There are 99 companies in the property sector in 2021. However, there were only 85 publicly available financial statements from 2010 to 2020. The rest did not have 10 years of listing history.

I divided the property development companies into 3 groups based on their 2021 shareholders’ funds:

Large – With shareholders’ funds greater than RM 1 billion. There were 27 sample companies in this group.

Medium – With shareholders’ funds between RM 300 million and RM 1 billion. There were 32 property developers here.

Small – There were 26 companies with shareholders’ funds of less than RM 300 million.

NOTE: Refer to Appendix 1 for the list of property development companies for each of the 3 groups above.

To cater to the different sample sizes in each group, I have used the average value (RM per company) when comparing the metrics for the various groups.

The key findings based on the 85 listed property development companies are:

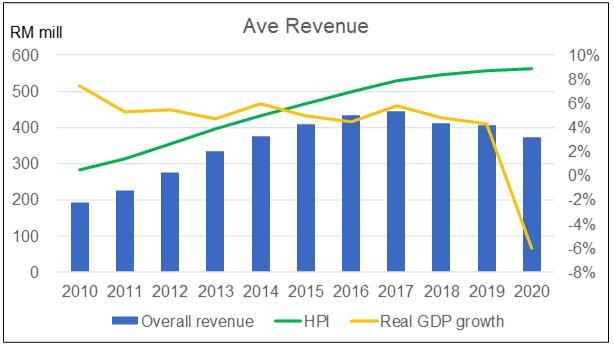

The property development industry revenue has been declining since 2017. Nevertheless, the industry revenue has grown at a CAGR of 6.8 % from 2010 to 2020.

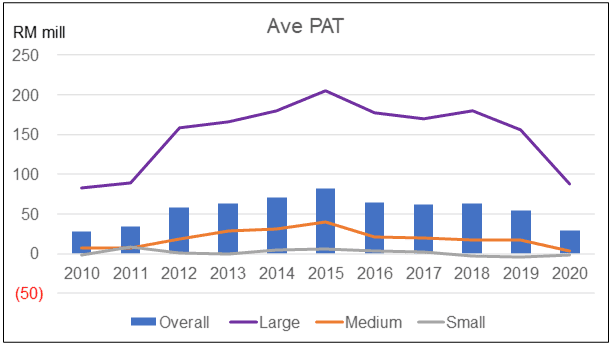

The industry earnings were at a standstill. The industry average PAT in 2020 is about the same as that in 2010.

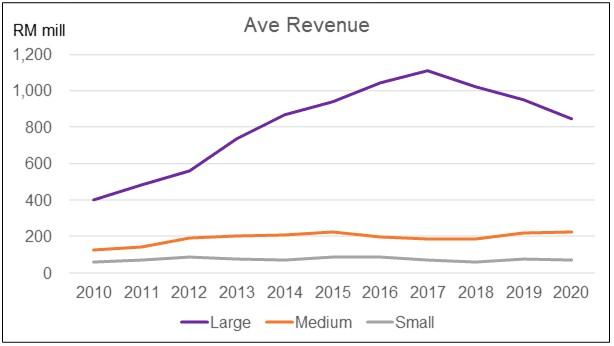

The growth in revenue and earnings was driven by the large company group.

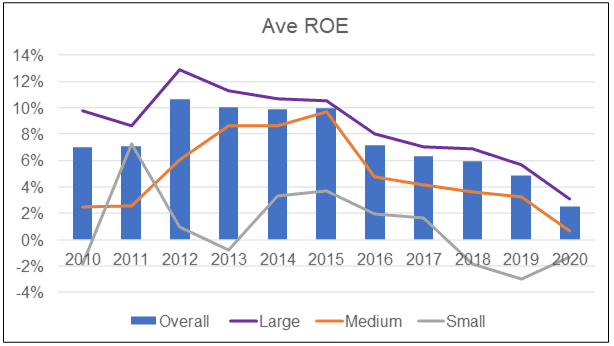

The industry performance in terms of Return on Equity peaked in 2012 and it has gone downhill since then. The 2020 Return on Equity is about 1/3 that of 2010.

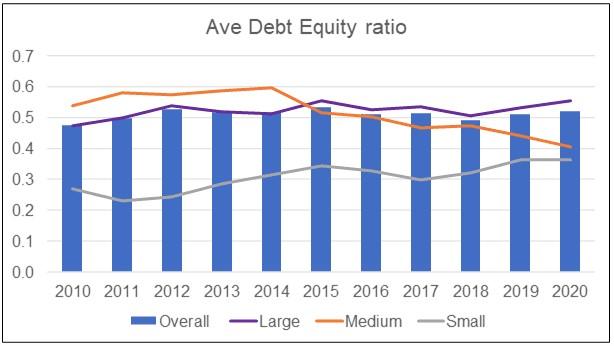

The industry funding in terms of equity and debt appeared to have increased despite the decline in earnings. This has resulted in a decline in the Return on Equity. On the positive side, the industry Debt-Equity ratio for the sector appears to be quite stable.

I do not see the real estate industry performance turning around until another 2 to 3 years’ time. If we are lucky, we may see the start of a property market uptrend in 2024. This is based on the declining revenue, declining gross profitability, and the big ship effect.

The rationale for the above is presented in the following sections.

Revenue of property companies on Bursa Malaysia

Based on the results of these 85 companies, the property development industry revenue in 2020 was 8% lower compared to that in 2019. In fact, as shown in Chart 1, you can see that the industry revenue had grown since 2010 to peak in 2017. Thereafter it experienced a decline so that the revenue in 2020 is 16 % lower than in 2017. On the positive side, the 2020 revenue is still about double that in 2010.

The cooling measures were introduced in the first half of the decade – most of them in 2013/2014. But the property development industry revenue continued to grow during this introduction period. In fact, house prices as represented by the Housing Price Index continued to rise.

As can be seen from Chart 2, the bulk of the revenue growth was driven by large property developers.

Profitability of property companies on Bursa Malaysia

When it comes to earnings, the industry average Profitability After Tax (PAT) in 2020 is about the same as that in 2010. Effectively earnings were at a standstill, as shown below. The biggest contribution was by the large property developers. In fact, the small group actually incurred losses for the past 3 years.

However, when you looked at Return on Equity (ROE), the industry performance peaked in 2012 and it has gone downhill since then. The 2020 ROE is about 1/3 that of 2010. A sobering thought if you have invested in property development companies in Malaysia. The trend is the same when you look at returns from a Return on Asset (ROA) basis.

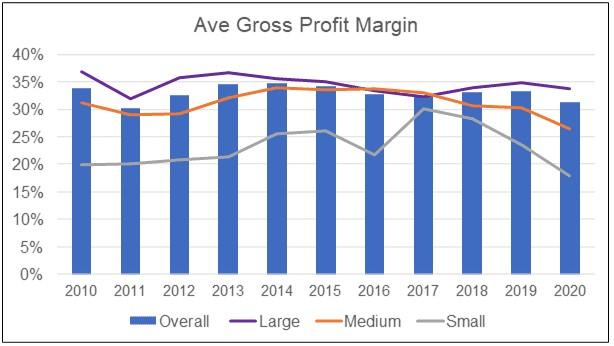

Gross profit margins of property companies on Bursa Malaysia

However, the gross profit margins (gross profit/revenue) for the sector appear to be less volatile than the earnings or revenue. I interpret the results to mean that as the revenue declined, the gross profit declined almost proportionately. However, despite the declining revenue and earnings, the funds to finance the business grew larger. This has resulted in a decline in the ROE and ROA.

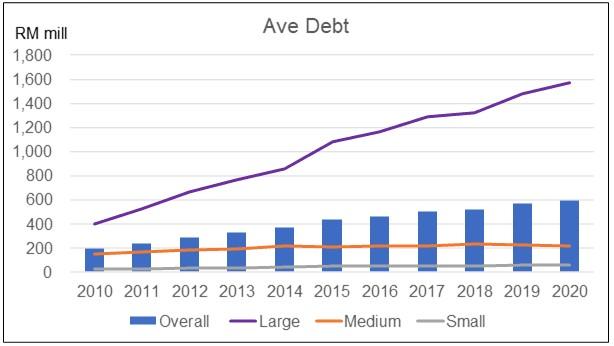

This is supported by trendlines showing how the equity and debt of the property development industry have grown over the decade.

2021 would also be another year where business operations are going to be disrupted by the Covid-19 pandemic measures.

Many property developers have reported a slow down or postponement of property launches in 2020. We may experience the same scenario in 2021.

As shown in the revenue chart, the industry has seen a declining revenue since 2017. With 2020 and 2021 as periods with lower property launches, the development pipeline is being depleted. So even if 2022 reverts back to the pre-pandemic “normal”, the big ship effect means that we are not likely to see any improvement in the sector profits or returns until a few years down the road.

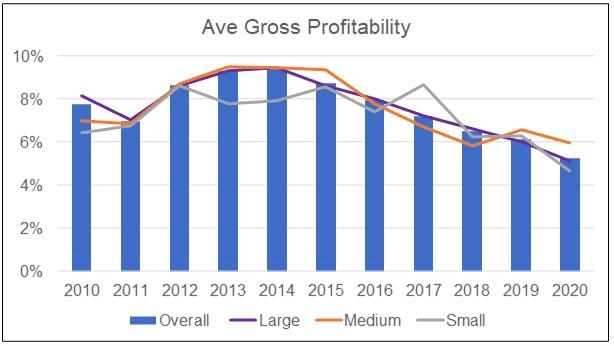

The other basis for my view is based on the gross profitability trend. Gross profitability is defined as gross profit divided by total assets. Professor Robert Novy-Max, University of Rochester, has done considerable research into this metric. According to him, it has roughly the same power as book-to-market in predicting the cross-section of average returns. Profitable firms generate significantly higher returns than unprofitable firms. This is despite having significantly higher valuation ratios.

I used this as one of the indicators to gauge the prospects of companies. As can be seen from the chart below, the gross profitability of the industry has been declining for the past 6 years.

The frightening thing is that the performance of all the 3 groups looked very similar. This is very unlike all the other metrics that I have presented. Given the reduced launches last year and possibly for 2021, I do not expect any improvement in this metric. I do not have a crystal ball to see the future. Gross profitability peaked in 2013/204. But:

The industry revenue peak in 2017.

The industry’s Profit After Tax peaked in 2015.

Industry gross profit margins were quite stable.

For the gross profitability to turn around, revenue must turn around first. And this has to occur without any substantial increase in the total assets used for the gross profitability to turn around. Based on Professor Robert Novy-Max’s theory, I don’t expect any turnaround in the property sector profits or returns till 2024. But it is not all doom and gloom. The industry debt to equity ratio is less than 1 and it does not seem to be increasing.

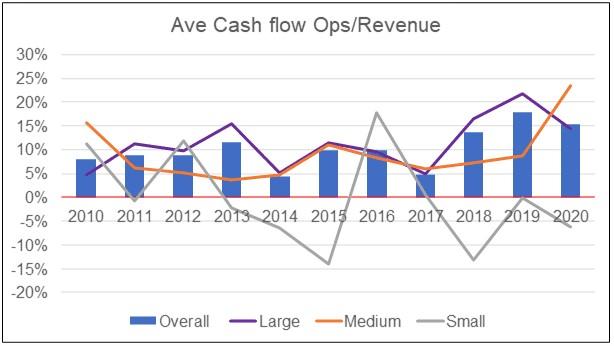

Secondly, cash flow which is key in the property sector has positive trends. As you can see from the chart below, the overall Cash flow from Operations as a % of the Revenue has been growing and this is despite the declining revenue. However, this Cash flow from Operations graph does not look too good for the small companies.

I have not attempted to relate the industry performance with the various measures taken by the government to manage the property sector. There have been several articles about the efficacy of the cooling measures and what needs to be done next so I won’t go into this.

But for those investing in the property sector, the results show that the performances of the small companies were the most volatile. I would focus on investing in large property development companies as they were the main drivers of the industry.

I invest in property companies and I undertook the study to provide base rates for my analysis. However, in looking at the results, do keep the following in mind.

The companies under the Bursa Malaysia property sector do not represent all the property companies in the country. There are also private developers. Then there also developers under Bursa Malaysia construction or industrial products and services sectors. Examples are WCT for the former and Sunway for the latter. But I doubt that these developers have different business trends than what I have presented.

Many of the sample companies have other property-related businesses in addition to property development. These could be investment properties and hotels. Others have non-property activities such as education and palm oil plantation. This meant that part of the revenue and earnings will come from non-property sources. These can help to cushion any negative impact due to property development.

Furthermore, many of the developers are also involved in the non-residential sectors. This may provide some diversification.

The data for the analysis were extracted from the financial statements from an online platform/app known as TIKR.com. Unfortunately, it does not cover the following property development KPI – new launches, property sales, and unbilled sales. We would be able to get a better picture of the current pipeline if such data were available.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.

Share

Share on Facebook

Share on Whatsapp

Share on LinkedIn

Share on Twitter

Copy link

Sign up and stay updated

Get the latest property insights from industry experts and real estate guides in Malaysia.

By subscribing, you consent to receive direct marketing from iProperty.com Malaysia Sdn Bhd (iProperty), its group of companies and partners. You also accept iProperty’s Terms of Use and Privacy Policy including its collection, use, disclosure, processing, storage and handling of your personal information.