| PROS | CONS |

| Passive Income | More work than buying stocks |

| Hedge against Inflation | Illiquid |

| Able to leverage | High transaction costs & longer transaction time |

| Less volatile price movements | Difficult to diversify |

| More difficult to be defrauded | Continued costs eg home insurance |

| Higher tax |

In this article, we compare the returns between investing in residential properties and investing in the stock exchange in Malaysia over the long term.

Investors are always looking for better assets to invest in. The million-dollar question asked by inspiring investors is which is a better investment – property or the stock market? Online responses to this query generally fall into two categories:

– Those that outline the pros and cons of each type of investment

– Those that focus on the comparative investment returns between stocks and property

The sentiments also differ from one investor type to another. A layman might compare residential properties with the Malaysian stock market while an institutional investor is more likely to compare the stock market with commercial properties.

For the purpose of this article, we take the position of a layman and compare the investment returns from Bursa Malaysia with those from residential properties. For Malaysia, the return analyses suggest that if you don’t have a 30-year time frame, you are better off investing in the stock market. The exceptions here are semi-detached and detached houses in the capital city of Kuala Lumpur.

Let’s dive into the details:

What are the pros and cons of investment property?

Do note that this is a qualitative assessment and the answers are independent of your location.

SEE WHAT OTHERS ARE READING:

💰 Flipping a house for profit in Malaysia: How to do it?

💡 Investing in auction properties: Tips and tricks.

What are the comparative (net) investment returns?

There aren’t many online resources available that detail the returns on property investment. Those that cover property gains tend to be about the US or European markets. Thus, for the purpose of this article, I compare investing in Bursa Malaysia with investing in residential properties in Malaysia.

- Kuala Lumpur Composite Index (KLCI) is used to represent Malaysian stocks. The KLCI is a capitalisation-weighted stock market index. It is composed of the 30 largest companies in Bursa Malaysia (refer to Notes 1)

- The Malaysian Housing Price Index (HPI) is used to represent residential properties. The HPI measures the changes in prices of an average house and is updated by the Malaysian Valuation and Property Services Department (JPPH) (refer to Notes 2)

We then look at the comparative returns of buying properties in 1990 against the stock market in 1990. The properties are held for 10 years, 20 years and 30 years before selling. In practice, the gains from properties would differ by location and residential property types in Malaysia. As such, we compare the investment returns for:

- four regions in the country – Kuala Lumpur (KL), Selangor, Johor and Penang

- four residential property types – terrace homes, semi-detached, detached and high-rise

The transaction costs of buying and selling the various assets are also factored in, where the investment returns presented in this article are the capital gains net of the various transaction costs. You may argue that the transaction costs especially the Real Property Gains Tax (RPGT) can be a large portion of the gain and may want to compare just the HPI with the KLCI. But, it is not realistic to compare the returns based on the indices only. In real life, there are transaction costs. Transaction costs include:

- Properties – property agent’s commission, stamp duty, legal fees and RPGT

- Stocks – brokerage fees and stamp duty

Other assumptions:

- Transaction rates are the same throughout the comparison period. The exception is RPGT as this applies only to properties sold in 2019

- Both the property and equity transactions are in cash. There are no borrowings

Investment property vs Stocks – Which one is better in the long term?

What can we conclude from the analysis?

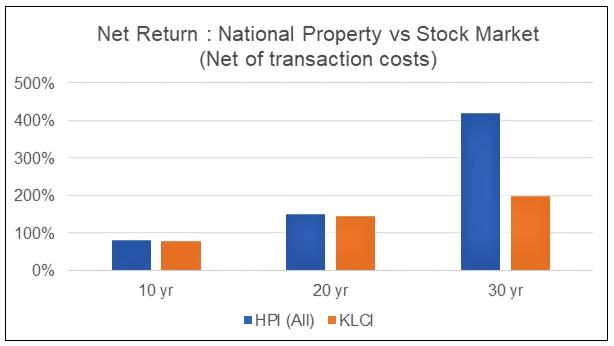

At the end of the 30 years, the returns from investing in properties are better than from the stock market. But for 20 years or less, the returns from investing in properties are only marginally better.

However, the stock market requires a lot of nerve as it has a larger peak to trough drawdown. You will also need a much longer time to recoup losses

| Duration (years) | Items | National HPI (All) | KLCI |

| 30 | Net Return (1) | 421% | 198% |

| Maximum drawdown (2) | (12)% | (53)% | |

| Time to recover from drawdown (3) | 6 yr | 11 yrs | |

| 20 | Net Return | 150% | 145% |

| Maximum drawdown | (12)% | (53)% | |

| Time to recover from drawdown | 6 yrs | 11 yrs | |

| 10 | Net Return | 81% | 79% |

| Maximum drawdown | (12)% | (53)% | |

| Time to recover from drawdown | Out of time | Out of time |

Notes

1) Net Return = Capital gain minus Transaction Costs + Purchase Price

2) Max drawdown = Difference between the peak and lowest trough (before any upturn)

3) Time to recover = Time required to return to the same level i.e. to the peak just before the start of the drawdown

Investment property vs stocks – Which housing type is better vs the KLCI?

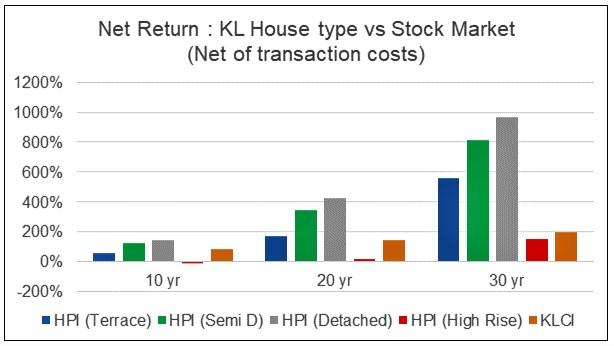

Property prices differ by house types. Rather than looking at all property prices, it might be prudent to compare between the different housing types in Malaysia. The chart and table below show the comparisons for four types of houses at national level.

As can be seen:

- After 30 years, the investment returns from terrace, semi-detached and detached houses outperform the KLCI. The best return is from investing in terrace homes.

- At the end of 10 or 20 years, the investment returns from the stock market are generally better compared to the four different types of residential properties

| Duration (years) | Net Return for different category of HPI | KLCI Net return | |||

| Terrace | Semi-D | Detached | High rise | ||

| 30 | 432% | 281% | 352% | 167% | 198% |

| 20 | 140% | 101% | 143% | 28% | 145% |

| 10 | 67% | 31% | 55% | (6)% | 79% |

CHECK OUT: How to invest in REITs in Malaysia and why is it an alternative to property investment?

Net investment performance of residential properties across Malaysia

Would the findings at the national level be different if we look at specific regions or states? Yes, very much so.

Below are charts and tables comparing between the regional property types. To provide different perspectives, the charts are by states and tables are by holding periods.

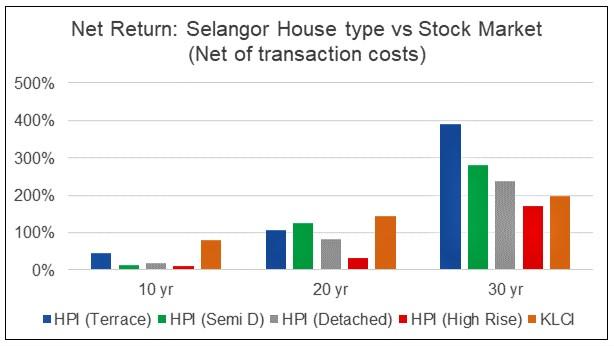

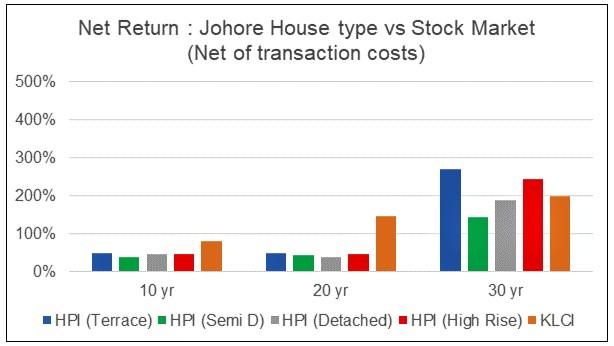

- For the KL region, you get better investment returns from detached and semi-detached homes in KL compared to the stock market regardless of the holding period

- If you hold for only 10 years, except for semi-detached and detached houses in KL, you are better off investing in the stock market

- If you are in Selangor, Johor and Penang and you want to hold for 20 years or less, you get better returns from the stock market. The only exception is holding terrace homes in Penang for 20 years

- The best returns come from investing in a detached house in KL and holding it for 30 years

- The worst investment returns come from buying a high-rise unit in KL and holding it for 10 years only. You actually make a loss.

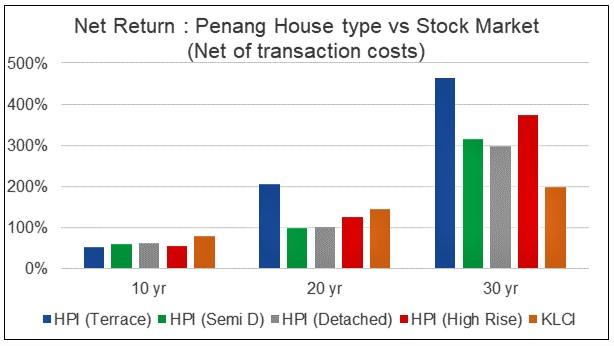

Holding an investment property for 30 years

| STATE | Net Return for different types of properties | KLCI Net Return | |||

| Terrace | Semi-D | Detached | High rise | ||

| KL | 560% | 811% | 967% | 147% | 198% |

| Selangor | 391% | 281% | 238% | 171% | 198% |

| Johor | 269% | 143% | 188% | 243% | 198% |

| Penang | 464% | 315% | 299% | 373% | 198% |

Holding an investment property for 20 years

| STATE | Net Return for different types of properties | KLCI Net Return | |||

| Terrace | Semi-D | Detached | High rise | ||

| KL | 169% | 344% | 427% | 16% | 145% |

| Selangor | 107% | 126% | 83% | 32% | 145% |

| Johor | 48% | 42% | 36% | 46% | 145% |

| Penang | 205% | 97% | 101% | 125% | 145% |

Holding an investment property for 10 years

| STATE | Net Return for different types of properties | KLCI Net Return | |||

| Terrace | Semi-D | Detached | High rise | ||

| KL | 58% | 125% | 143% | (11)% | 79% |

| Selangor | 45% | 14% | 19% | 10% | 79% |

| Johor | 47% | 36% | 46% | 45% | 79% |

| Penang | 52% | 59% | 63% | 54% | 79% |

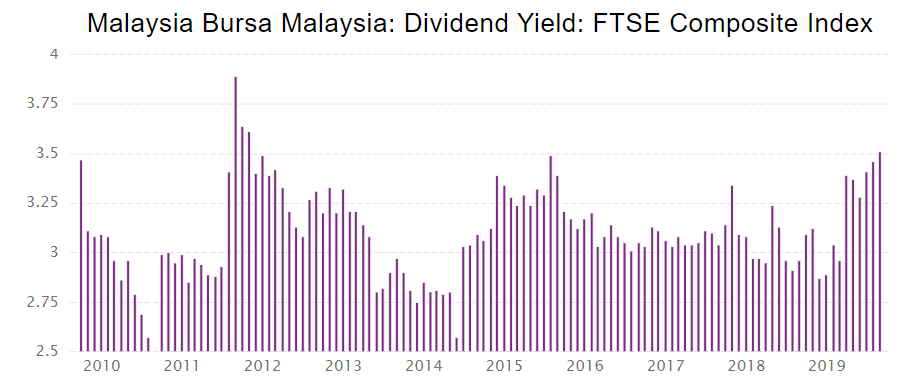

Several sources suggest rental yields for properties are better than the dividend yield for stocks. According to the Globalpropertyguide.com, the average rental yield for properties in Malaysia stood at 3.72% as of June 2020. Comparatively, the dividend yield for the KLCI companies for the past 10 years appears to be about 3% as shown in the chart below.

Conclusion

- There are both qualitative and return factors to be considered when deciding whether to invest in the stock market or in properties. But I don’t think the pros of investing in properties can offset the lower returns associated with a short holding period

- The returns are affected not only by the changes in the value of the assets but also by transaction costs and taxes. They vary not only by location and house type but also by the tax structure. So returns comparison has to be specific for each country

- For Malaysia, the return analyses suggest that if you don’t have a 30-year time frame, you are better off investing in the stock market. The exceptions here are for semi-detached and detached houses in KL

- For Malaysia, if you can hold for 30 years, then property is a better investment than the stock market. The exceptions are high-rise properties in Selangor

and semi-detached and detached homes in Johor

FOOTNOTES

1. This comparative investment return analysis takes into consideration cash investment. Returns might be different if you take a loan to buy a property

2. Returns might be different if the timing of the purchases were different. For example, instead of starting in 1990, the results would be different if the start was in 2010

3. This analysis does not include the impact of recurring annual operating income and expenses such as:

- Rental income and other operating costs such as insurance for properties

- Dividends from the companies making up the KLCI

Unfortunately, we do not have historical rental income records for the various types of properties in Malaysia. Similarly, we do not have the records of the dividends paid by the KLCI companies from 1990.

If you enjoyed this guide, read this next: Malaysia’s Top 7 High-Rise Properties with the Highest Rental Yield in 2019

*This article was repurposed from “In Malaysia, which has better returns; Stock market or Property?“, first published on i4value.asia

TOP ARTICLES JUST FOR YOU:

🏗️ Property market lessons Malaysians can learn from Covid-19.

🤔 5 things you should know before investing in a property.

🔑 Buying a property to live in vs. renting it out.

Disclaimer: The information is provided for general information only. iProperty.com Malaysia Sdn Bhd makes no representations or warranties in relation to the information, including but not limited to any representation or warranty as to the fitness for any particular purpose of the information to the fullest extent permitted by law. While every effort has been made to ensure that the information provided in this article is accurate, reliable, and complete as of the time of writing, the information provided in this article should not be relied upon to make any financial, investment, real estate or legal decisions. Additionally, the information should not substitute advice from a trained professional who can take into account your personal facts and circumstances, and we accept no liability if you use the information to form decisions.