An analysis of latest transactions, top neighbourhoods and preferred residential products.

Highlights

• Terrace homes in Skudai, Kulai and Pasir Gudang showed impressive capital appreciation, recording above average figures of 9.4%, 13.1% and 21.5%, respectively.

• Asking rental yield for apartments appears promising amid a sluggish property market – the top 5 transacted areas provided monthly returns above 5%.

• Properties within the RM260,000-RM340,000 price range were most popular among purchasers – Which begs the question, is this the standard for affordable properties in IM?

For analytical purposes, we will focus on these two products, of which key figures were extracted for the top 5 performing areas within the IM region, for terrace homes and apartments, respectively.

- The period of evaluation is from April 2016 – March 2017.

- Terrace homes comprise of single, double and triple storey houses.

- The price of apartments vary across Johor, in most areas they consist of mid-priced units, ranging between RM150,000-RM300,000. However, apartments in newer areas such as Iskandar Puteri have higher than average selling prices.

- The data used to calculate asking median rent are obtained from iProperty.com.my listings. Only monthly rents within the evaluation period are used to determine the median – this final figure is then used to calculate asking rental yields in each area.

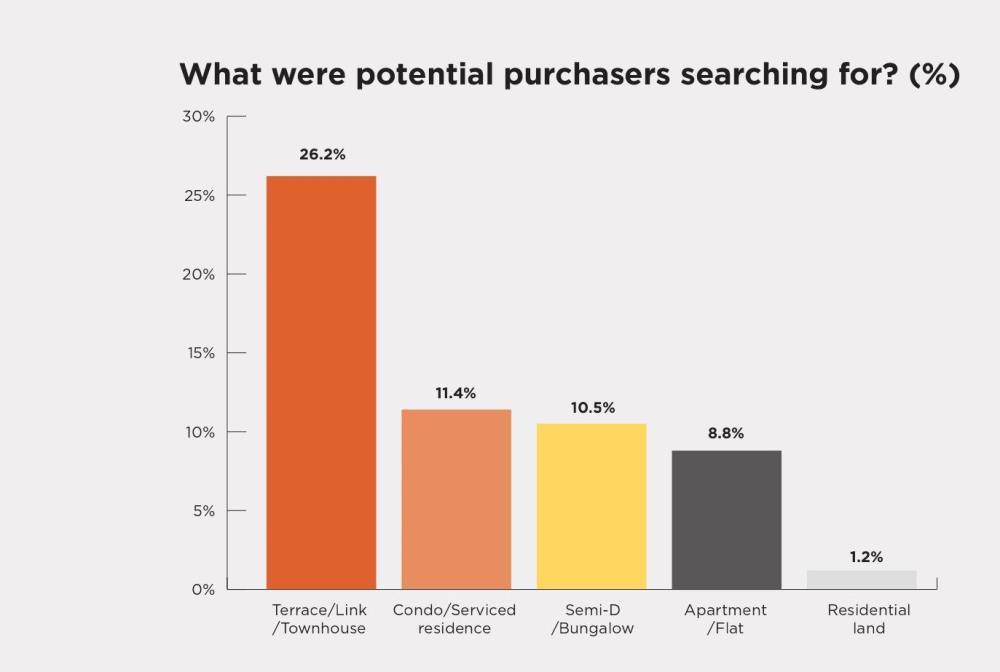

- The type of properties displayed in the “What were potential purchasers searching for” infographic is based on the search tab category in iProperty.com.my.

Terrace Homes

Key figures for top 5 areas

Source: iPropertyiQ.com

Source: iPropertyiQ.com

Save for Iskandar Puteri which suffered a slight drop of 0.7%, the other areas performed remarkably well in terms of year on year (y-o-y) capital growth. This positive trend is contrary to the public’s perception that property prices are devaluing, says Samuel Tan.

Skudai and Kulai are secondary towns within Greater Johor Bahru and have always been very popular among the locals. Price growths of 9.4% and 13.1% are not unreasonable and could be explained by the suburb effect – where locals and city centre folk are drawn to the cheaper housing alternatives available in these areas.

Meanwhile, the substantial appreciation of 21.5% seen in Pasir Gudang is mainly attributed to the mushrooming of new developments in the area, particularly the Eco Tropics project by EcoWorld and Mah Sing’s Meridin East township. These developers are offering housing concepts and products that are fresh and new to the region, at higher-than average price points – a lake garden community with Meridin East and Eco Tropics will be the first gated and guarded development in the Kota Masai area. These ‘new kids on the block’ will inevitably influence the secondary market and pull up its prices as well.

Tebrau is a very mature area – property prices there have been increasing steadily since 2014. It’s boom period kicked in earlier compared to other areas – hence, the smaller growth rate of 4.8% in the recent year. On the other hand, being a greenfield or new development, Iskandar Puteri is still in its ‘teething stages’ – with newly completed units coming onstream property prices are still adapting to market movements. Hence, the slight drop in property values is not alarming.

The rental yields ranging between 3.9% to 5.5% are commendable and appear attractive to investors as the returns are similar or higher than the current fixed deposit rates. In light of economic hiccups and market fluctuations, these healthy yield rates testify that real estate remains as a good investment vehicle.

Apparently, more people in IM are purchasing pricier properties. And yes, we have the data to show.

Top 3 projects in each area

Source: iPropertyiQ.com

Source: iPropertyiQ.com

Samuel notes one common thread that runs across all these schemes – they are self-contained townships or something similar. Zooming into Iskandar Puteri, the top 3 neighbourhoods – Bukit Indah, Nusa Bestari 2 and Nusa Bayu are commanding robust median prices in the range of RM376-RM460 per sq ft. This is attributed to their proximity to the Woodlands Causeway and the Tuas Second Link, a boon for those who commute daily to Singapore for work. In addition, these residential enclaves are complemented by various supporting infrastructure and amenities – from banks to clinic and grocery stores. Despite their higher than average median prices, convenience is the main driver for the huge demand for properties there. Meanwhile, housing units in the other 4 suburbs offer good value for money deals. Good connectivity links to the JB city centre is a main selling point too.

What were people buying?

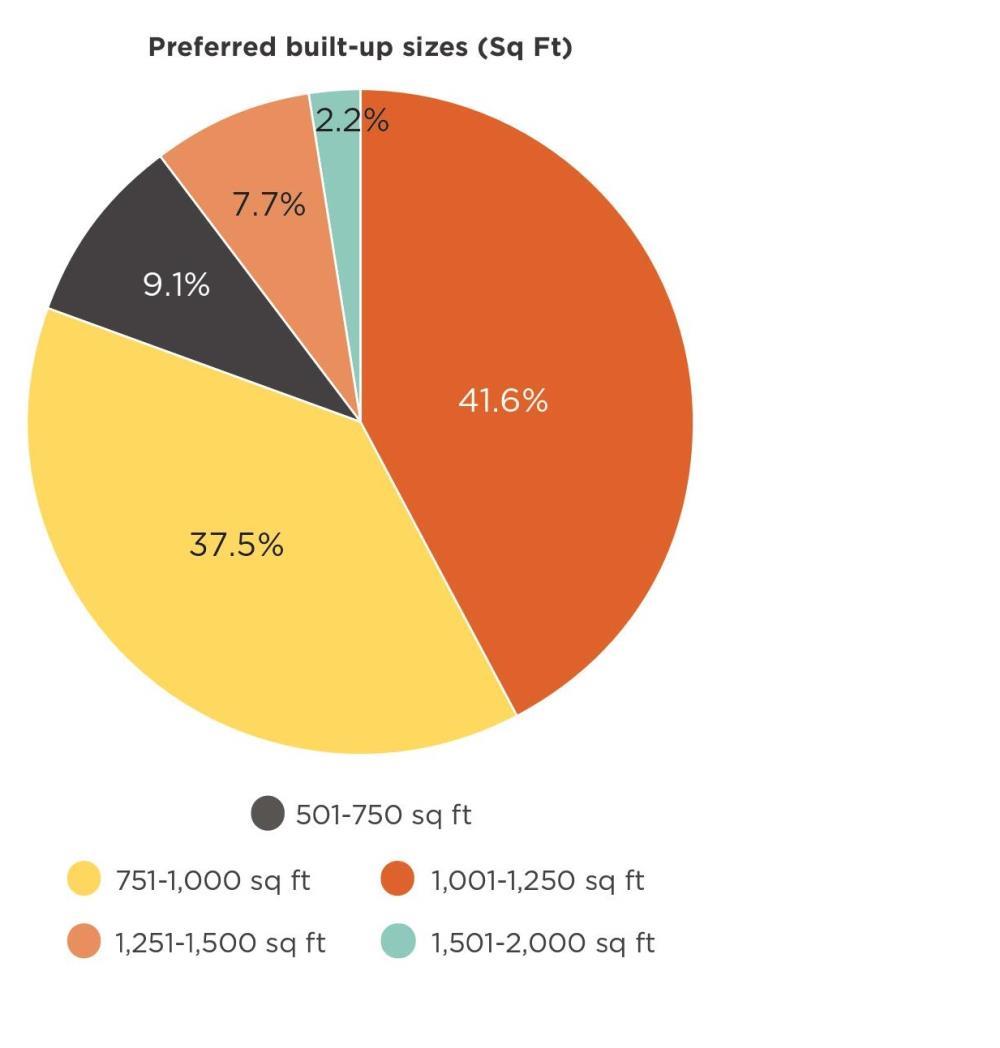

The three most popular sizes for terrace homes were:

1) 750-1,000 sq ft

Traditionally, these are single-storey terrace homes which can accommodate at least 2 bedrooms and possibly an en-suite room cum study room. Units at the end of the spectrum, i.e measuring 1,000 sq ft should be able to house 3 comfortably sized bedrooms. Homes of these sizes are popular among small families and first-time home owners due to the affordable entry point. Some of the government-driven schemes such as PRIMA fall within this size range too.

2) 1,501 – 2,000 sq ft

These are typically double-storey terrace homes and can comfortably accommodate 3 to 4 bedrooms with at least 2 bathrooms, making it very suitable for the average Johorean household, consisting of 6-8 people. Newly completed units of this size will cost roughly RM400,000 in an average area whereas those more strategically located will bear higher price tags.

3) 1,251 to 1,500 sq ft

Properties in this category are basically large single-storey terrace homes or more compact double storey terrace units. Again, their popularity is due to the affordable factor. Nevertheless, developers are no longer constructing homes within this price range, hence transacted sales moving forwards will only occur in the secondary market.

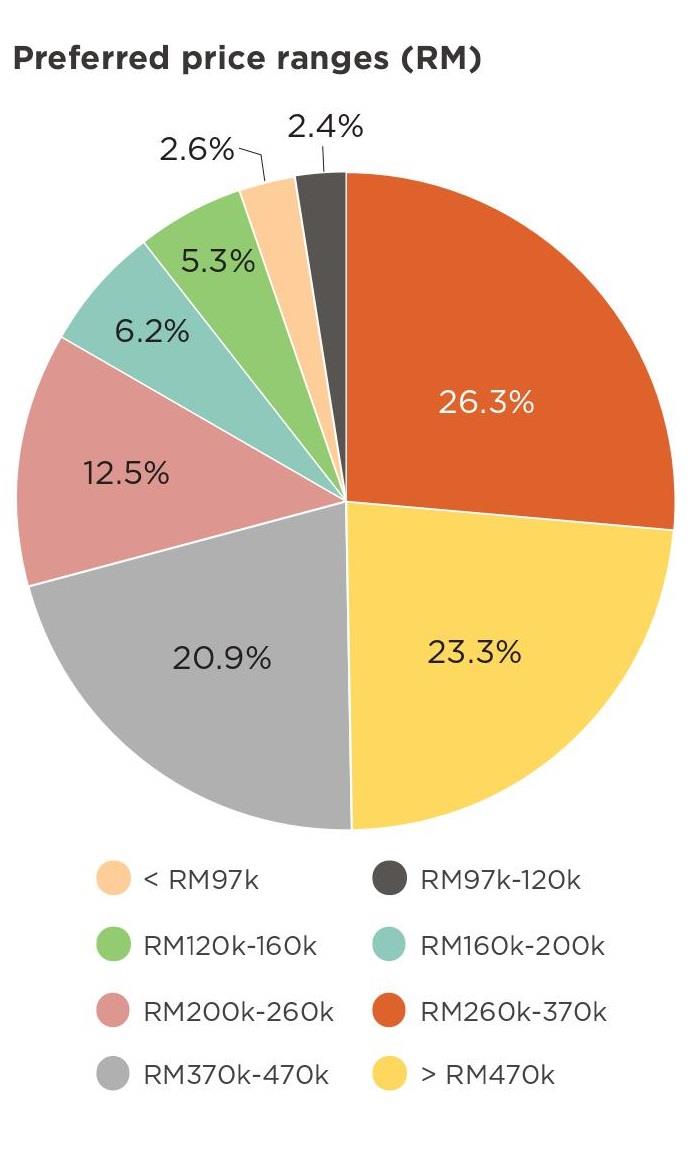

More than a quarter or 26.3% of the transactions occurred in the RM260,000 and RM370,000 category. As defined by Bank Negara Malaysia (BNM) these are considered as affordable housing. When compared against the median household income of Johoreans, most can afford to purchase homes up to this price point. Coming in a close second at 23.3% are homes priced above RM470,000. According to Samuel, these purchases would have occurred in the larger, more populous areas like JB. Most double-storey terrace home in the suburbs are already going for RM450,000 and above, with deluxe offerings priced beyond RM1 million.

You get what you pay for – which is why these homes are desirable to those who could afford them as they offer quality, comfortable sizes, strategic location and quality finishes. Another quarter or 29% trended in the price categories not exceeding RM260,000 – one can only deduce that these are for the low and low-medium cost houses.

Future Trends

Within JB, the immediate purchasing trend will be for properties ranging from RM450,000 to RM800,000, shared Samuel. With the stringent loan requirements, however, home buyers must be prepared to cough up more cash for a down payment. This consumer challenge will put a constraint on developers’ selling prices. A similar trend of dampened prices can also be expected for the secondary market. The current emphasis on assisting first-time-house-buyers will see the launching of more properties costing below RM400,000. As can be seen in the few recent government budgets, various schemes have been introduced to assist millennials and civil servants in achieving their home ownership dream.

Apartments

Key figures for top 5 areas

Source: iPropertyiQ.com

Samuel points out that capital growth values for apartments in Iskandar Malaysia are relatively lower than their landed counterparts. This could be attributed to the current oversupply of such products in the local market. Notwithstanding that, it is a pleasant surprise indeed to witness a positive growth rate.

Masai showed the highest y-o-y capital appreciation of 8.6%. The most plausible explanation for this growth trend is the emergence of new apartments in an area which never had many modern residential strata buildings before. Iskandar Puteri showed a marginal growth of 2.6% as this area is still new and property prices there require time to stabilise.

In terms of rental yield, all 5 areas showed commendable rates ranging from 5.6% to 8.0% per annum. Except for Iskandar Puteri and JB, the other regions recorded figures exceeding the market’s standard of a profitable figure, i.e 6%. The above average percentages were probably due to the lower market value of sub-sale units vis-à-vis the monthly rental. Meanwhile, Iskandar Puteri and JB have many higher-priced, new apartments/service apartments and in the current buyers/tenants’ market, it is only normal for the rental yields to be lower.

Top 3 projects in each area

Source: iPropertyiQ.com

Advice for Homebuyers & Investors

1. Due diligence must-dos include product details, accessibility to convenience, cost of repairs, security concerns as well as the quality and cost of management and maintenance.

2. Find out the ratio of local and foreign purchasers – having more locals within a project/neighbourhood holds more appeal as house prices there tend to be more stable.

3. Considering the current oversupply of high-rise units in IM, investors should be more discerning than usual when making a purchase.

4. Only purchase in popular areas – where tenant demand is high and sustainable.

5. Look for projects with a good concept and a strong management team.

What were people buying?

1) 750-1,000 sq ft

The lion share of purchases or 41.6% were transacted in this category. Samuel shares that this floor area can comfortably accommodate 3 bedrooms and 2 bathrooms. Also, the living and dining/kitchen areas will be pretty spacious, thus very appealing to families with several children. Prices for new apartments in the JB city centre will range between RM800,000 and RM1.2 million whilst those in the suburbs fall within RM550,000 to RM1.2 million. The higher end ones are usually luxury units with high-quality finishes.

2) 751-1,000 sq ft

These typically feature 2 bedrooms and 2 baths. Larger units might even have an extra bedroom. First time home buyers and young couples especially are the main fans of such ‘starter’ units.

3) 501-750 sq ft

Such units are likely studios or one bedroom apartments. During the property boom in the 2013- 2015 period, numerous developers launched smaller- sized units, which received good response as the price points were very affordable. It is no surprise why these units are popular among those looking to get a foothold on the property ladder as well as investors looking for healthy rental yields. Current prices range from RM250,000 to RM900,000.

As enumerated earlier, the RM260,000-RM340,000 price range takes the crown for most purchases. Typically older apartments of over 10 years old with a floor area of roughly 1,000 sq ft are sought after by small families as they feature 3 bedrooms and 2 bathrooms. 19.7% of transactions were garnered for properties priced between RM340,000 and RM420,000. Again

these would be apartments nearer to the city with a floor area of roughly 1,000 sq ft. Given the constant variables with the previous category, these pricier units offer a better location and/or higher quality finishes and more attractive facilities.

There aren’t many property options within the RM220,000-RM260,000 category except for basic apartments in lesser-known suburbs. These cheaper units would appeal to the masses, especially to households with a monthly disposable income of less than RM5,000.

Future trends

Given the current residential overhang, particularly for high-rise units in Johor, the state government had frozen all new applications for service apartments since 2014. Projects being constructed are expected to see completion in the next 2 years. This incoming supply means that it will take some time for the market to digest the excesses, explained Samuel.

Several scenarios are expected to play out in the next few years – developers with unsold stock will be prompted to offer more freebies including cheaper selling prices and special packages to entice purchasers.

As more units flood the market, investors will be competing over a limited pool of tenants, giving rise to a tenant’s market. With the exception for some premium apartments, owners of most schemes will find yield accretion a challenge. Securing a tenant in the first place will not be an easy task, given the supply-demand mismatch.

However, with the serviced apartments freeze as mentioned, there may be a new pent-up demand for apartments from 2020 onwards. Considering the developments in technology and innovations such as Industrialised Building System, the new breed of apartments will be quite different from their predecessors.

In line with consumers’ demand, we can expect to see more uniquely designed homes with carbon-free and environment-friendly features as well as the utilization of artificial intelligence and Internet of Things (IoT).