With every tragedy comes an opportunity or two, which is especially useful when it comes to life-changing decisions like buying a property. What are they and how can it help you?

At this point of writing, we are already very close to 60% recovery rate from the COVID-19 pandemic in Malaysia, and the total number of recoveries has been higher than new cases for 9 days in total.

→ Navigate Covid-19: Property knowledge, stay at home articles and tools. Get started now.

So, with all these positive turnarounds, are we expecting a booming property market very soon? As someone who owns a couple of properties, of course I would hope so. However, as a person who has spoken to many prominent property owners and investors, the answer is as follows:

The property market has not changed, instead sentiment has declined

The implementation of the Movement Control Order (MCO) was not the start of a slowing Malaysian property market. In fact, it is because of the extremely successful Home Ownership Campaign (HOC) in 2019, which has resulted in our number of property transactions in 2019 to be much slightly higher in 2018. What has happened from 2013-2018 was a mismatch in the demand and supply of properties. Despite many Malaysians wanting to buy, their requirements and affordability were not being met in terms of the properties being built and introduced into the market.

The situation is evolving now with more “on-point” new property launches. Whether it is a landed property with a slightly smaller land size to make the price more attractive, or the additional number of units in high-rise developments to make the price more affordable – housing developers are changing their development plans to cater to the market demand, who were asking for more affordable homes. Then, COVID-19 arrived. However, I believe that the property market mismatch was improving, even if the overhang number may linger around for a while more.

MORE: What caused Malaysia’s residential property overhang and when will it get better?

Housing demand is still and will be there

With the MCO in effect, this is delayed further, but it does not mean that there is no demand for properties. From the 300,000 over graduates we have every year to the new household formation and the fact that the median age in Malaysia is still 30 – all these points to strong demands for properties in the long term. It is always a consideration between size, distance and connectivity – although it’s prudent to note that demands for property types will continue to evolve over time.

Would property prices drop then?

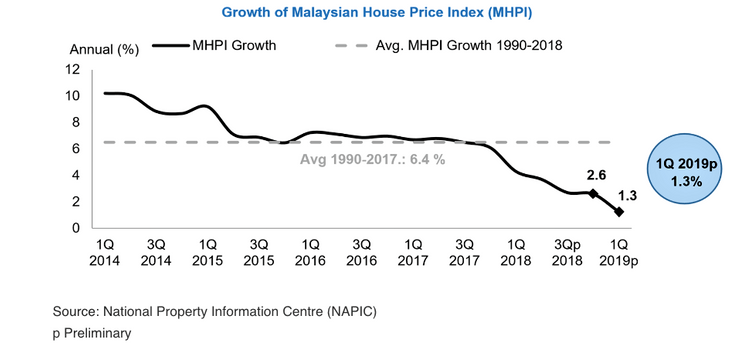

This is a question everyone has in their mind and it has been the same question even before the arrival of COVID-19. The term buyer’s market has been around for a couple of years – it did not appear because of the Covid pandemic. Residential property prices have been growing at a much slower rate these past few years but, if we look at the Malaysia House Price Index (MHPI), we would be able to clearly see that property prices did not drop into the negative territory. What has happened however is that the percentage increase in property price continued to drop every quarter.

This shows that property price increase is already below the typical salary increments in Malaysia since 2018 and I think with the COVID-19 situation, we may even see prices drop into the negative territory for a while. There are definitely motivated sellers who may need the cash and would prefer to sell their property instead of holding on to it. In order to sell faster, they would have to sell below the market price.

As for the question of whether the property prices would drop, we have to look at the employment market. In order to understand the employment market, we would need to look at the direction of the economy. If the economy does not start growing fast enough, more businesses may fail and more people will be likely out of jobs. If this happens, then yes, we may see property prices weakening.

What is the current consumer sentiment?

At the moment, the 6-month loan moratorium for all consumers till end of September 2020 seeks to provide some breathing space to businesses. I would want to think that this is enough and that the Malaysian economy would already start growing again by then to kick off an economic rebound. Anything above negative is already a plus. At this moment, it does seem that the situation is getting better, even for the badly affected countries like China, whose economy is slowly recovering and the pandemic is under control. Consumers will definitely be extra careful with spending from hereon, so businesses will need to look into new ways to give value to them.

The U.S. has just announced steps for the states to start reopening businesses versus the current lockdown. Even Italy and Spain have seen the number of new infections stabilising versus an increasing trend. Some drugs have shown promise in COVID-19 treatments while a few vaccines have already reached the human trial stage.

So, when will the property market recover?

Well, if we were to ask economists, they will tell you that we need to look at the economy which will then require us to push up job numbers first. If we were to ask real estate agents, now is the best time to buy because it is a buyer’s market. If we were to ask the vaccine researchers, they will tell you that the fastest that vaccines could ever reach the manufacturing stage would be 12-18 months from now. So, the answer is a mixed bag as all of them are right from their own respective views, and only time will tell.

When is the right time to buy a property?

If you ask me, I think it’s imperative to understand the reason for buying. Do not focus on the “when”. When you realise that it’s time to buy, the prices would have already moved up for a while. If you made a purchase and the prices drop within the next couple of months, you may not sleep well at night.

Stay focused on WHY. The ‘why’ should be based on necessity and practicality. Prices are definitely not on the high side today. Interest rates are also on the low side – even when compared to rates from the 1998 Asian Financial Crisis – making it an opportune time for you to apply for a home loan.

Therefore, if you have the right reason to buy, then go ahead as both price and interest rates are on our side, currently.

To gauge your readiness to purchase a property, some of the questions you should ask yourself beforehand are:

- Am I ready to purchase a property now?

- Do I have the financial capability to buy a property?

- Do I have the time to research and carry out the necessary due diligence required for property purchasing/investment?

MORE HERE: Are you ready to purchase or is it a case of missing out?

By the way, there’s nothing wrong with renting a property forever. Just be sure to set aside enough money because when it comes to paying rent, it doesn’t stop for rain nor shine. On the other hand, a mortgage lasts only 35 years but there are other extra costs involved from the get-go. Either way, it’s always best to spend based on your current needs and capability – but don’t forget to use any and every advantage possible.