The following tips could score you substantial tax savings.

1. Look at the calendar

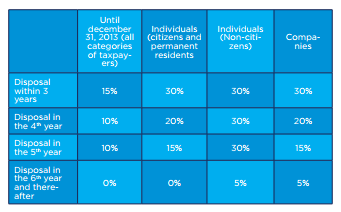

Real Property Gains Tax (RPGT) is imposed on the chargeable gain you make from a property sale. The rate charged will depend on the duration that you have held the property for, as shown below:

One tip for when determining how long you have held your property for is to take note of the ‘disposal in the Xth year’ part. For instance, a Malaysian who disposes of his property after holding it for 5 years and 1 day will attract 0% RPGT as the sale qualifies as a disposal in the sixth year.

Whereas, if the same investor sold off the property after 4 years and 364 days, it will be considered as a disposal in the fifth year, which results in a 15% RPGT rate.

The moral of this story: be mindful of when you bought your property in the first place. Take a quick look at your Sale and Purchase Agreement to determine when it will be safe for you to make a sale. A matter of a few months or even a week could save you from unnecessary tax expenditure.

READ: What is Real Property Gains Tax (RPGT) in Malaysia & How to calculate it?

2. Know your allowable deductions

There are several expenses incurred which one can claim as an allowable deduction against the gain obtained from a property sale.

(a) Enhancement costs’, ie. expenditure incurred for the enhancement of the property, which includes renovation costs and the cost of construction of a building on the land.

(b) Fees, commission or remuneration paid for the professional services of any surveyor, valuer, accountant, agent or legal adviser.

(c) Transfer costs (including stamp duty).

(d) Advertising costs.

(e) Valuation report to ascertain market value.

(f) Goods & Services Tax (GST) incurred by a seller who is not registered under the GST Act 2014, or who is registered but is not entitled to an input tax credit on the GST incurred.

Any other expenditure than the ones listed above does not qualify as deductions. For example, expenses incurred on loan interest of a property or penalty on early settlement of loans are not deductible expenditures when computing your RPGT.

MORE: What is property valuation & the 4 factors which influence a home’s value?

3. You can file the relevant returns to the tax authorities yourself

Property sellers can save a few hundred Ringgit by opting to file the necessary forms (most importantly, the CKHT 1A Form) with the Inland Revenue Board (IRB) on their own, without solicitor assistance.

Check out the IRB website where a comprehensive guide is provided on how to do so. At the moment, the guidelines are only available in Bahasa Malaysia. Alternatively, visit your local bookstore to get a copy of my book, ‘Every Property Investors Guide To How To Pay Less Tax Legally’ for the guide in English, plus other tax-savings tips!

4. The sale of your property may be subject to income tax!

As of late, the IRB has been actively scrutinising property transactions to determine whether such sale of property(ies) is based on the circumstances of each sale, subject to RPGT or in reality, subject to Income Tax instead.

This means the IRB may surprise you a few years down the road after the sale of your property that they have reason to believe that the sale was in their opinion, subject to Income Tax. This will result in the property sale being subjected to Income Tax of up to 28% of the gains obtained on top of penalties as well!

The most effective way to mitigate this kind of exposure with the IRB is to understand this one concept – ‘the badges of trade tests’. These tests, which are established by the courts are used by the IRB to determine if a property seller is ‘trading’ in properties (i.e. Income Tax) instead of ‘investing’ in properties (i.e. RPGT).

The badges of trade include:

NATURE OF THE ASSET

A property which yields rental income typically gives the impression that the property is held for investment while a property which is not rented out is taken to be held as a trading asset.

SOURCES OF FINANCE

The purchase of investment properties is normally financed by long-term borrowings (eg. term loan) where the repayment of the borrowings can be financed from the rentals received from those properties. Meanwhile, speculative properties are normally financed using short-term funds such as bank overdraft.

FREQUENCY OF TRANSACTIONS

Repetitive and systematic undertaking of property transactions may indicate trading in properties.

CHANGES TO THE PROPERTY

Improvements or modifications made to an asset prior to sale to make it more marketable such as carrying out renovation works and giving the property that you bought a fresh coat of paint may be viewed as efforts to enhance the value of the property prior to resale and may attract Income Tax.

CHECK OUT: 3 Critical things property investors often overlook

5. Be mindful about the Goods and Services Tax (Gst)

Commercial property investors, take note!

Depending on certain conditions being met as determined by the Director-General of Customs (DGC), a sale of a commercial property may be subject to GST.

Property sellers will have to pay a 6% GST, which is calculated from the gross selling price to the Royal Malaysian Customs (RMC).

According to the DGC, if you own

a. more than 2 commercial properties;

b. more than one acre of commercial land; or

c. commercial property or commercial land worth more than RM2 million at market price;

AND if you have the intention to sell any of your commercial properties, then you are considered to be running a business and have to comply with the relevant GST laws (ie. collect and pay GST to the RMC).

Do watch out for this relatively new tax because if you do not account for the GST element when negotiating the sale of your commercial property, the RMC can deem the selling price of that property to be inclusive of the 6% GST.

You will then have to pay the GST portion (plus penalties) from the sales proceeds which you have collected.

This article is written by Richard Oon, National Tax Director of ShineWing TY Teoh.